The term "quanto" is the abbreviation of quantity adjusting option. The payoff of quanto derivatives is determined by an asset denominated in one currency, but is paid in another currency.

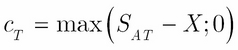

The best way to understand a quanto product (or any kind of derivative) is to examine its payoff function. It is well known that assuming the underlying asset is a stock that pays no dividend, the payoff of a European call option is as follows:

Here, SA is the price of the stock and X is the strike price. Here, c, SAT, and X are denominated in the same currency; let's call it domestic currency.

The payoff of a European call quanto is as follows:

Here, S is a foreign exchange rate. Thus, a call quanto pays the same "quantity" of money as a simple call option, but in another currency—let's call it foreign currency. So, this quantity paid has to be multiplied by an FX rate so that we get the payoff's value in domestic currency. Of course, S has to be the price of the foreign currency in terms of domestic currency. In other words, in the quotation of S, the base currency is the foreign one.

Pricing a call quanto means determining the value of the earlier payoff. As usual, we will assume that the price of the underlying asset under the risk neutral measure (Q) follows geometric Brownian motion with drift equal to the risk-free domestic rate (r), that is:

Furthermore, we assume that the FX rate follows a similar process:

In these equations, W1 and W2 are standard Wiener processes under Q, with correlation ρ. Let q denote the risk-free foreign rate. This means that the value of one unit of foreign bank deposit at time t is exp(qt). In terms of the domestic currency, this value is as follows:

Supposing that this is a traded product in the domestic market, its discounted value has to be a martingale under Q. Let's calculate this discounted value:

This process is martingale only if ![]() , which is under Q.

, which is under Q.

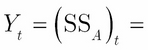

Now, we will calculate the SSA product, which we will denote by Y.

Here, ![]() and

and  .

.

The correlation ![]() between W2 and W3 is

between W2 and W3 is  .

.

Consequently, ![]() .

.

Now, it is important to notice that the call quanto is a special exchange option, and hence, might be priced with Margrabe's formula. We only have to identify the two risky assets to be exchanged upon exercising the option, and the related parameters. From the payoff function of the quanto, it is easy to see that the first risky asset is SSA = Y, while the second one is XS (both expressed in domestic currency). Since the drift components of these processes under Q are not simply the risk-free domestic rate, we have to use the Margrabe formula with dividend yields. From the earlier calculations, we can see that the Y process should be handled as if the dividend yield was ![]() , while in case of XS, it is simply q. The only remaining parameter to be determined is σ. With straightforward substitutions, we have the following calculation:

, while in case of XS, it is simply q. The only remaining parameter to be determined is σ. With straightforward substitutions, we have the following calculation:

Summarizing all these results, we have to use the Margrabe formula (given in Equation (4)) with the substitutions ![]() ,

, ![]() ,

, ![]() ,

, ![]() , and

, and ![]() .

.

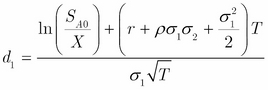

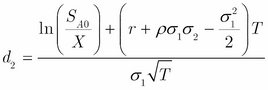

Hence, the price of the call quanto is as follows:

In the earlier equation, d1 and d2 were as follows:

and

and  .

.

Let's see an example to price a call quanto in R. Our favorite stock is priced at 100 USD and 20 percent volatility. We need a call option with 90 USD, which is paid in EURs in three years. The USD risk-free rate is r = 2% and the EUR risk-free rate is q = 3%. Currently, 1 USD is equal to 0.7467 EUR. The EUR volatility is 15%, and the correlation between the stock price and the USDEUR exchange rate is 10%.

If in three years the price of the stock is higher than 90 USD, the difference is paid in EUR. If, for instance, the price is 110 USD in 3 years, we will get 20 EURs. On the current FX rate, it is 20*0.7467 = 26.78093 USD, but if the EURUSD exchange rate is different in three years, for example, USDEUR is equal to 0.7, this equals 28.57143 USD. So the payoff can be different in USD, but we eliminated the FX rate risk if we want to be paid in EUR.

This seems complicated, but fortunately, we can use the Margrabe formula and our Margrabe function to calculate the price of the option.

Margrabe = function(S1, S2, sigma1, sigma2, Time, rho, delta1 = 0, delta2 = 0)

We need these substitutions ![]() ,

, ![]() ,

, ![]() ,

, ![]() , and

, and ![]() .

.

S1 is the stock price in EUR, and S2 is the strike price in EUR. delta1 and delta2 can be calculated easily: delta1 = 0.03-0.02-0.2*0.15*0.1 and delta2 = 0.03. The only problem is that we need to set sigma = sigma1, but sigma is not a parameter of the Margrabe function; it is calculated inside the function body. Consider the following command:

sigma = sqrt(sigma1^2 + sigma2^2 - 2 * sigma1 * sigma2 * rho)

To get the sigma = sigma1 result, we need to set sigma2 = rho = 0.

Now, we can call the Margrabe function with the given parameters.

Margrabe(74.67, 90*0.7467, 0.2, 0,3, 0, 0.007 , 0.03) [1] 16.23238

The result is 16.23. This is the price of the quanto.