When using the interest rate models for pricing or simulation purposes, it is important to calibrate their parameters to real data properly. Here, we present a possible method to estimate the parameters. This method was developed by Chan et al, 1992, and is often referred to as the CKLS method. The procedure was elaborated to estimate the parameters of the following interest rate model with the help of the econometric procedure called Generalized Method of Moments (GMM; see Hansen, 1982, for more details):

It is easy to see that this process gives the Vasicek model when γ=0, and the CIR model when γ =0.5. As the first step of the parameter estimation, we discretize this equation with the Euler approximation (see Atkinson, 1989):

Here, δt is the time interval between two observations of the interest rate and et is independent, standard normal random variables. The parameters are estimated with the following null hypothesis:

Let Θ be the vector of the parameters to be estimated, that is, ![]() .

.

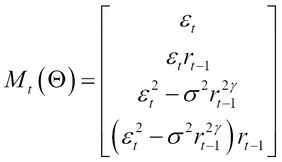

We consider the following function of the parameter vector:

It is easy to see that under the null hypothesis, ![]() =0.

=0.

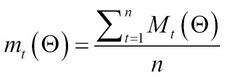

The first step of GMM is that we consider the sample corresponding to ![]() , which is

, which is ![]() :

:

Here, n is the number of observations.

Finally, GMM determines the parameters by minimizing the following quadratic form:

Here, ![]() is a symmetric, positive definite weight matrix.

is a symmetric, positive definite weight matrix.

There is a quadprog package in R for these kinds of problems, or we can use general methods for optimization with the optim function.