Until this point, we considered the entire sample as one. It could be a logical decision to focus only on some industries. Note that choosing the right industry to invest should not be based on past performance pattern; we rather have to analyze comovements with global economic trends over a number of years, and then, based on our prediction for the coming periods, we should pick the one with the best outlook. This method helps you to determine the right weights of the industries in your portfolio, but then, you still need to select individual shares that may overperform the others.

Of course, once one given industry is selected, we may end up with different investment rules than those on the whole sample. So, we may further improve our investment performance by performing the previously shown steps for each industry separately.

At the same time, recall that the more specific you are in data selection (time period, industry, and firm size), the less likely will the strategy created show good performance on other samples or in the future. By increasing the degree of freedom of your strategy building (rerunning all statistical tests for subsamples), you make recommendations fit nearly perfectly to the given sample that may reflect the effects of a number of random events. As these random effects never occur again, adding more and more flexibility after a certain limit will actually worsen the end result.

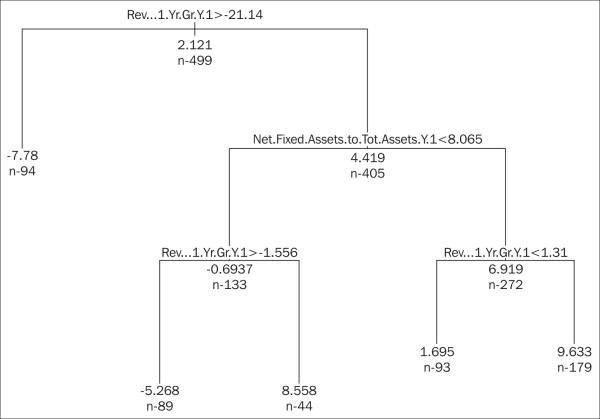

For the sake of the example, we picked Communications. If we apply the decision-tree technique here, we would end up with the following figure. After that, we have to invest into firms that have seen their revenue growing by less than 21 percent but more than 1.31 percent during the last year, while the net fixed assets ratio was at least 8.06 percent:

d_comm <- d[d[,18] == "Communications",c(3:17,19)] vars <- colnames(d_comm) m <- length(vars) tree_formula <- paste(vars[m], paste(vars[-m], collapse = " + "), sep = " ~ ") library(rpart) tree <- rpart(formula = tree_formula, data = d_comm, maxdepth = 5 ,cp = 0.01, control = rpart.control(minsplit = 100)) tree <- prune(tree, cp = 0.006) par(xpd = T) plot(tree) text(tree, cex = .5, use.n = T, all = T) print(tree)

At the same time, building a strategy based on a general sample of a given period may end up overweighting certain industries that show great performance during the given year(s), while, of course, there is no guarantee that the coming years will also prefer the same sectors. So, after building our strategy, we should crosscheck whether there is a serious industry dependency behind that strategy.

A cross-table controlling for the connection of the industry and decision-tree-based investment strategy reveals that we heavily overweighted the Energy and Utilities sectors. The cluster-based strategy, at the same time, gives an extra weight to materials. The code for the latter is shown here:

cross <- table(d[,18], d$selected) colnames(cross) <- c("not selected", "selected") cross not selected selected Communications 488 11 Consumer Discretionary 1476 44 Consumer Staples 675 36 Energy 449 32 Financials 116 1 Health Care 535 37 Industrials 1179 53 Materials 762 99 Technology 894 7 Utilities 287 17 prop.table(cross) not selected selected Communications 0.0677966102 0.0015282023 Consumer Discretionary 0.2050569603 0.0061128091 Consumer Staples 0.0937760489 0.0050013893 Energy 0.0623784385 0.0044456794 Financials 0.0161155877 0.0001389275 Health Care 0.0743262017 0.0051403168 Industrials 0.1637954987 0.0073631564 Materials 0.1058627396 0.0137538205 Technology 0.1242011670 0.0009724924 Utilities 0.0398721867 0.0023617672

We may also be interested in how good our strategy performs across industries. For this, we should see the average TRS of firms chosen and not chosen for all the individual sectors. To create a table like this, we need to use the following command. The output illustrates how the decision-tree-based strategy performs (0 not selected, 1 selected):

t1 <- aggregate(d[ d$tree,19], list(d[ d$tree,18]), function(x) c(mean(x), median(x))) t2 <- aggregate(d[!d$tree,19], list(d[!d$tree,18]), function(x) c(mean(x), median(x))) industry_crosstab <- round(cbind(t1$x, t2$x),4) colnames(industry_crosstab) <- c("mean-1","median-1","mean-0","median-0") rownames(industry_crosstab) <- t1[,1] industry_crosstab mean-1 median-1 mean-0 median-0 Communications 10.4402 11.5531 1.8810 2.8154 Consumer Discretionary 15.9422 10.7034 2.7963 1.3154 Consumer Staples 14.2748 6.5512 4.5523 3.1839 Energy 17.8265 16.7273 5.6107 5.0800 Financials 33.3632 33.9155 5.4558 3.5193 Health Care 26.6268 21.8815 7.5387 4.6022 Industrials 29.2173 17.6756 6.5487 3.7119 Materials 22.9989 21.3155 8.4270 5.6327 Technology 43.9722 46.8772 7.4596 5.3433 Utilities 11.6620 11.1069 8.6993 7.7672

As shown in the preceding output, our strategy performs pretty well in all sectors; though in Consumer Staples, the median of the selected firms is somewhat near to that of not selected. In other cases, we may end up seeing that in some sectors, we do not get very good results, and the TRS of the chosen firms may even be lower than that of the other group. In this case, we would build a separate stock-selection model for those sectors where our model performed weaker.