As we learned in the previous chapter, banking is a specifically risky industry and the safety of the clients' money is a top priority. In order to ensure that banks meet this primary objective, the industry is under strict regulation. It has always been a very important task for supervisors to build rules to avoid the collapsing of banks and to protect clients' wealth. Capital adequacy or capital requirement is one of, if not, the most, important regulatory tool to serve this goal. Given the high leverage in the financial sector, banks and other financial institutions are not allowed to freely use all their assets. These firms need to hold enough capital to ensure safe operation and solvency even if things turn bad.

Different countries have different banking supervisory bodies (financial watchdog, central bank, and so on) and regulation standards. However, as the banking system became more and more globalized, a common worldwide standard became necessary. In 1974, the Basel Committee on Banking Supervision (BCBS) was set up by the G-10 central banks to provide banking regulatory standards that can be applied to different countries around the globe.

This area of economics has developed quite fast since then, and more and more complex mathematical methods are used in risk management and capital adequacy calculation. R is such a powerful tool that it is perfectly capable of solving these complex mathematical and analytical problems. Therefore, it is not surprising that many banks use this as an important tool for risk management.

In 1988, the BCBS published a regulatory framework in Basel, Switzerland, to set the minimum capital that a bank needs to hold to minimize the risk of insolvency. The so-called First Basel Accord, which is now referred to as Basel I, was enforced by the law in all of the G-10 countries by 1992. By 2009, 27 jurisdictions were involved in the Basel Regulatory Framework (the history of the Basel Committee can be read at http://www.bis.org/bcbs/history.htm).

The first Basel Accord mainly focuses on credit risk, and formalizes the appropriate risk weighting considering different asset classes. Based on the Accord, the assets of banks should be classified into categories regarding credit risk, and the exposure of each category should be weighted with the defined measures (0 percent, 20 percent, 50 percent, and 100 percent). The resulted value of risk-weighted assets (RWA) is used for the determination of capital adequacy. According to the Basel I legislation, banks that are present on international markets are required to hold capital of at least 8 percent of their RWA. This is called the minimum capital ratio (refer to Basel Committee on Banking Supervision (Charter) http://www.bis.org/bcbs/charter.htm).

The so-called off-balance sheet items such as derivatives, unused commitments, and credit letters are included in RWA, and should be reported as well.

The Accord was intended to amend and refine over time in order to address risks other than credit risk as well. Furthermore, it was revised to give more appropriate definitions to certain asset classes included in the capital adequacy calculation and to recognize subsequently identified effects.

Basel I defines other capital ratios as well, in order to quantify the banks' capital adequacy. The capital ratios are considered as certain so-called tier-capital elements relative to all RWA. Tier-capital elements include types of capital grouped based on the definition of Basel I. However, each country's banking regulator might revise the classification of the financial instruments considered in capital calculation due to the different legal frameworks of the countries.

The tier 1 capital includes core capital, which is composed of common stock, retained earnings, and certain preferred stocks, which meet the defined requirements. Tier 2 is considered supplementary capital, which involves supplementary debts, undisclosed reserves, revaluation reserves, general loan-loss reserves, and hybrid capital instruments, while tier 3 is deemed as the short-term additional capital. (Committee on Banking Regulations and Supervisory Practices (1987): Proposals for international convergence of capital measurement and capital standards, Consultative paper, December 1987, http://www.bis.org/publ/bcbs03a.pdf.)

Basel II was issued in 1999 as a new capital adequacy framework proposed to succeed Basel I, and was published in 2004 in order to ensure resolutions to certain issues, which was slightly regulated by the former Basel Accord.

The main objectives of Basel II were to:

- Provide more risk-sensitive capital allocation

- Implement appropriate calculation methods for not only credit risk but market risk and operational risk as well

- Improve the disclosure requirement in order to make capital adequacy more perceptible for market participants

- Avoid regulatory arbitrage

The framework of Basel II is based on the three following pillars:

- The minimum capital requirements by which the Committee intended to develop and expand the standardized capital adequacy calculations

- A supervisory review of a financial institute's capital adequacy and internal assessment process

- Effective disclosure to enhance market discipline

The required capital on credit risk can be calculated according to the standardized approach. Based on this method, credit exposures should be weighted by measures considering primarily the related ratings by External Credit Assessment Institutions (ECAI). Claims on sovereigns, corporates, and banks or securities companies can be weighted by 0 percent, 20 percent, 50 percent, 100 percent, or 150 percent according to their ratings; however, based on the claims by international associations such as IMF, BIS, or EC, the risk weight should consistently be 0 percent.

Regarding secured claims, cash, and other assets, there are constant weights defined by the Committee and implemented by local regulators who are considering risk mitigation techniques. Eligibility can be considered on different levels regarding the different asset classes, and is regulated in local acts and decrees of the countries. Furthermore, real estate is not deemed as cover but as exposure according to the standard approach; therefore, it is included in the regulation on asset classes as well.

Minimum capital requirement is defined as 8 percent of the RWA, considering conversion factors in case of off-balance sheet items. Capital requirement determined by this method should be appropriate to cover credit risk, market risk, and operational risk as well.

Other methods for the calculation of credit risk are the so-called Internal Ratings-Based (IRB) approaches, including Foundation IRB and Advanced IRB. IRB approaches are allowed to use only the approved banks by their local regulator.

IRB approaches apply a capital function to determine the required capital. There are key parameters that influence the capital function, such as probability of default (PD), loss given default (LGD), exposure at default (EAD), and maturity (M).

Probability of default is considered the likelihood that the client will not (entirely) meet its debt obligation over a particular time horizon. By IRB methods, the bank is allowed to estimate the PD of its clients based on either own developed models or by applying the ratings of ECAI.

Loss given default is the percentage of a relating asset when the client defaults. LGD is related tightly to EAD. Exposure at default is the value of the outstanding liability towards the client at the time of the event of its default. Applying Foundation IRB, the calculation method of EAD is determined by the local regulator; however, by Advanced IRB, the banks are allowed to develop their own methodology.

Maturity is a duration type parameter, which indicates the average remaining part of the credit period.

Advanced IRB enables another classification of exposures and assets, which may reflect more on the characteristics of the bank's portfolio. Furthermore, the range of the possibly applied credit risk mitigation actions expands as well.

Although RWA can be determined by various methods by applying either Foundation IRB or Advanced IRB, according to Basel II, the minimum capital requirement is the 8 percent of RWA in both cases.

Determination of the operational risk can be executed by different methods. The simplest way of the calculation is the so-called Basic Indicator Approach (BIA). Based on this approach, the capital requirement is defined as the average of gross incomes (GI) of the previous 3 years of the bank multiplied by a given measure, Alpha, which is determined as 15 percent by the legislation.

The Standardized Approach (STA) is a little bit more complex. This approach adopts certain methods of BIA; however, using STA, it is required to determine the gross income regarding the lines of business (LoB). The GI of each LoB should be multiplied by a fixed measure, Beta (12 percent, 15 percent, or 18 percent, depending on the LoB). The capital requirement is the sum of the products of GIs and betas that refer to the LoBs.

The aim of the Alternative Standard Approach (ASTA) is to avoid double imposition due to credit risk. ASTA adopts the methodology of STA; however, in the case of two LoBs (Retail and Commercial banking), the calculation differs from the standardized approach. Regarding these LoBs, GI is replaced by the product of the value of loans and advances (LA) and a fixed factor (m is equal to 0,035).

The most complex methodology of the determination of operational risk is the Advanced Measurement Approach (AMA). This approach has both quantitative and qualitative requirements, which should be met. The internal model developed for the estimation of the operational risk has to correspond to the standards of safe operation, such as risk measurement on 99.9 percent possibility regarding the period of 1 year. Furthermore, banks that apply the AMA have to provide data of the past 5 years in relation to their losses.

Risk-mitigation techniques can be applied for up to 20 percent of the capital requirement only by banks that use the advanced measurement approach. The banks also have to meet certain strict requirements to be allowed to adopt the risk-mitigation effects.

Regarding the calculation of capital requirement for market risk, the standardized approach is based on the measures and techniques defined by regulators. For more advanced approaches, determination of Value at Risk (VaR) is considered the preferred methodology.

Basel II defines the supervisory and interventional responsibilities of local regulators. It enables them to prescribe a higher capital requirement than what is determined in Pillar I. Furthermore, it allows regulating and managing the remaining risks that are not described in Pillar I, such as liquidity, concentration, strategic, and systemic risks.

The International Capital Adequacy Assessment Process (ICAAP) is meant to ensure that the bank operates an appropriately sophisticated risk management system, which measures, quantifies, summarizes, and monitors all the potentially occurring risks. Furthermore, it should oversee whether the banks have enough capital determined, based on internal methods, to cover all the mentioned risks.

The Supervisory Review Evaluation Process (SREP) is defined as the procedure for the examination of risk and capital adequacy of the institutes executed by the local regulator. Moreover, considering Pillar II, the regulator has to regularly monitor the capital adequacy according to Pillar I, and intervene in order to ensure the sustainable level of capital.

Pillar III of Basel II focuses on the disclosure requirements of banks. It refers mainly to the listed institutes, which are required to share information regarding the scope of application of Pillar I-II, risk assessment processes, risk exposure, and capital adequacy. (Basel Committee on Banking Supervisions (1999): A New Capital Adequacy Framework; Consultative paper; June 1999; http://www.bis.org/publ/bcbs50.pdf.)

Even before the financial crisis, the need for review and the fundamental strengthening of Basel II framework became evident. During the crisis, it was apparent that the banks had inadequate liquidity position and too much leverage. Risk management should have been more significant, while credit and liquidity risks have usually been mispriced.

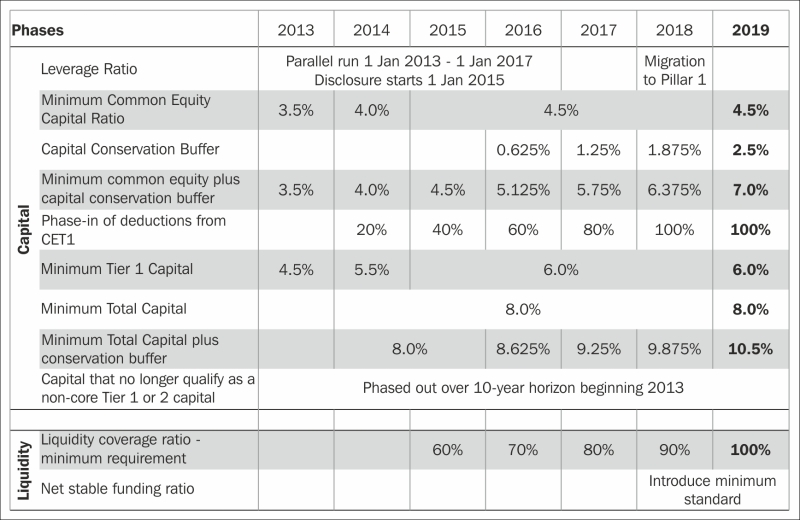

The third installment of Basel Accords was developed in 2010 with the aim of providing a more stable and safe operation framework for the financial sector. Basel III and the relating Capital Requirements Directive (CRD IV) are supposed to be implemented into the local legislation by 2019.

Although the implementation will be executed in several steps, the financial institutions are required to commence the preparation for the application of new capital standards even years before the deadline.

The areas concerned in the regulation of Basel III are the following:

- The elements of the required capital—implementing a capital conservation buffer and a counter-cyclical buffer

- Introduction of leverage ratio

- Implementation of liquidity indicators

- Measurement of the counterparty risk

- Capital requirement of credit institutions and investment companies

- Implementation of global prudential standards

In order to improve the quality of capital, Basel III regulates the composite of required capital. Core Tier 1 is defined within Tier 1 capital, and a so-called capital conservation buffer is implemented with the constant measure of 2.5 percent. A discretionary counter-cyclical buffer is introduced as well, which is considered an additional 2.5 percent of capital during periods of high-credit growth.

A leverage ratio was also defined by Basel III, as a minimum amount of loss-absorbing capital compared to all assets and off-balance sheet items regardless of risk weighting.

The most significant provision of Basel III is the introduction of two liquidity indicators. The first one, considered on a short-term horizon, is the liquidity coverage ratio (LCR), which should be implemented in 2015. LCR is the value of liquid assets relative to the cumulated net cash flow within a 30-day period. At the beginning, the minimum value of LCR should be 60 percent; however, it is intended to be raised to 100 percent by 2019. The formula for the LCR is as follows:

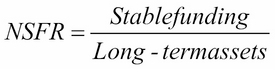

The Net stable funding ratio (NSFR) is going to be implemented in 2018. The aim of this indicator is to avoid maturity gaps between the assets and liabilities of financial institutions. The objective is to provide financing of long-term assets that concern the stability of liabilities. Consequently, NSFR is defined as the stable liabilities on stable assets to be financed. The measure of NSFR should be a minimum 100 percent in 2019 as well.

To avoid systemic risks, capital requirement is implemented also with regard to counterparty risk. Expectations regarding the capital adequacy and liquidity position of counterparties are framed according to the Basel III regulation. Regarding the capital adequacy, institutes that mainly apply internal calculation methods are involved in the new regulation, since the regulation takes into consideration the more detailed examination of potential risks that occur and the exposures towards Systematically Important Financial Institutions (SIFI). Based on the third installment of Basel Accords, the institutions should identify the SIFI based on an indicator than apply the requirements determined by the regulator regarding them (refer to History of the Basel Committee).

The main measures and phase-in arrangements of Basel III are included in the following table: