CHAPTER 12

FASB Value Worlds

The Financial Accounting Standards Board (FASB) is a private, not-for-profit organization whose primary purpose is to develop generally accepted accounting principles (GAAP) within the United States in the public's interest. The FASB, acting as an authority, has created a number of value worlds in the past few years, several of which are described in this chapter.

Specifically, this chapter discusses fair value, which gives guidance for post-transaction financial reporting compliance. The goal of the FASB's framework is to eliminate the inconsistencies between balance sheet (historical cost) numbers and income statement (fair value) numbers. Further, the fair value of the target company's identifiable assets and goodwill is reflected on the acquiring company's balance sheet. The fair value ultimately impacts the company's reported earnings in subsequent periods due to amortization of certain identifiable intangible assets.

FASB FAIR VALUE (ASC 820, FORMERLY FAS 157)

During the last decade, the use of fair value measurements in financial reporting has increased. In 2006, the FASB issued Financial Accounting Standard (FAS) 157 to provide a framework for how companies should measure fair value and sets out the required disclosures when GAAP requires the use of fair value. Note that the FASB is using the term “fair value” here, even though “fair value,” the subject of Chapter 9, has been used to describe minority dissent and oppression cases for decades. Companies began using FASB's framework for nonfinancial assets and nonfinancial liabilities for the first time in 2009. Also in 2009, the FASB proposed, and in some cases finalized, additional guidance and disclosures relating to fair value measurements. This guidance was codified as Accounting Standards Codification (ASC) 820.

In accounting, fair value is used as an estimate of the market value of an asset (or liability) for which a market price cannot be determined (usually because there is no established market for the asset). Under GAAP (FAS 157), fair value is the amount at which the asset could be sold or the liability could be transferred in a hypothetical transaction between willing parties, or transferred to an equivalent party, other than in a liquidation sale. Note that the definition focuses on the exit price rather than the entry price. This is used for assets whose carrying value is based on mark-to-market valuations; for assets carried at historical cost, the fair value of the asset is not used. One example of where fair value is an issue is a restaurant with a cost of $2 million that was built five years ago. If the owners wanted to put a fair value measurement on the restaurant, it would be a subjective estimate because there is no active market for such items or items similar to this one. In another example, if ABC Corporation purchased a two-acre tract of land in 1980 for $1 million, then a historical-cost financial statement would still record the land at $1 million on ABC's balance sheet. If XYZ purchased a similar two-acre tract of land in 2005 for $2 million, then XYZ would report an asset of $2 million on its balance sheet. Even if the two pieces of land were virtually identical, ABC would report an asset with one-half the value of XYZ's land; historical cost is unable to identify that the two items are similar. This problem is compounded when numerous assets and liabilities are reported at historical cost, leading to a balance sheet that may be greatly undervalued. If, however, ABC and XYZ reported financial information using fair value accounting, then both would report an asset of $2 million. The fair value balance sheet provides information for investors who are interested in the current value of assets and liabilities, not the historical cost.

Exhibit 12.1 provides a snapshot of the key tenets of FASB fair value.

EXHIBIT 12.1 Longitude and Latitude: FASB Fair Value

| Definition | The price received to sell an asset or the price paid to transfer a liability in a transaction taking place in an active market. |

| Purpose of appraisal | To determine the fair value of a company's assets or liabilities, as described by FAS 157. |

| Function of appraisal | To determine the price that would be received to sell the asset or transfer the liability at the measurement date (an exit price). |

| Quadrant | Notional regulated. |

| Authority | FASB. |

| Benefit stream | Determined on a case-by-case basis. |

| Private return expectation | Determined on a case-by-case basis. |

| Valuation process summary | Valuation technique follows three broad levels of inputs (Level 1 being the highest priority).

Level 1: Observable inputs that reflect quoted prices (unadjusted) for identical assets or liabilities in active markets (e.g., price × quantity). Level 2: Inputs other than quoted prices included in Level 1 that are observable for the asset or liability, whether directly or indirectly. Level 3: Unobservable inputs (i.e., a reporting entity's own data, financial projections, or when a financial model is relied on). |

FAS 157 provides a framework for measuring fair value. This structure is described in five steps:

1. Determine unit of account.

2. Determine potential markets based on the highest and best use.

3. Determine markets for basis of valuation.

4. Apply the appropriate valuation technique(s).

5. Determine fair value.

Step 1: Determine Unit of Account

The reporting entity must first determine the unit of account (i.e., what is being measured). Fair value is measured for a particular asset or liability and, thus, should incorporate its specific characteristics, such as condition, location, and restrictions, if any, on sale or use as of the measurement date.

Step 2: Determine Potential Markets Based on the Highest and Best Use

After determining the unit of account, the reporting entity must assess the highest and best use for the asset, based on the perspective of market participants. In accordance with FAS 157, paragraph 12, the fair value of an asset is based on the use of the asset by market participants that would maximize its value. The highest and best use for an asset must be determined based on the perspective of market participants, even if the reporting entity intends a different use.

Consideration of the highest and best use for an asset is an integral part of the identification of potential markets where the asset can be sold and establishes the valuation premise. The valuation premise may be either in use or in exchange.

Liabilities are valued based on the transfer of the liability to a market participant on the measurement date. However, reporting entities must still consider potential markets for the transfer of the liability.

Step 3: Determine Markets for Basis of Valuation

Once a reporting entity has considered potential markets, market participants, and the valuation premise, it must assess whether it has access to any potential markets. If access is available, a reporting entity must consider these points:

- Is there a principal market for the asset or liability? In accordance with FAS 157, paragraph 8, the principal market is the market in which the reporting entity would sell the asset or transfer the liability with the greatest volume and level of activity for the asset or liability. If there is a principal market, the fair value measurement represents the price in that market, even if the price in another market is potentially more advantageous.

Furthermore, based on this guidance, if the reporting entity does have a principal market, it will be able to expedite steps 2 and 3. The reporting entity cannot incorporate potentially more advantageous markets in its fair value measurements when it has a principal market. - What is the most advantageous market? If the reporting entity does not have a principal market, it should determine the most advantageous market for sale of the asset or transfer of the liability. As part of this determination, a reporting entity may need to consider more than one potential market. In each potential market, the entity should evaluate whether the appropriate valuation premise is in use or in exchange. In some cases, a reporting entity will need to determine the value in multiple markets and may need to consider both valuation premises in one or more markets, in order to determine the highest fair value.

The market determination should incorporate the appropriate valuation technique(s), as further described in step 4. The reporting entity will determine the most advantageous market using valuation technique(s) consistent with market participant assumptions in each of the potential markets. The market that results in the highest value for the asset or the lowest amount that would be paid to transfer the liability (after transaction costs) will represent the most advantageous market.

In the application of the framework, it is important to note that the determination of highest and best use and development of the fair value measurement are based on market participant assumptions. However, the determination of the principal or most advantageous market is determined from the perspective of the reporting entity itself based on its business model and market access.

If there are no potential markets for the asset or liability, the reporting entity must develop a hypothetical market based on the assumptions of potential market participants.

Step 4: Apply the Appropriate Valuation Technique(s)

FAS 157 emphasizes the use of market inputs in estimating the fair value for an asset or liability. Quoted prices, credit data, yield curve, and so forth are examples of market inputs described by FAS 157. Quoted prices are the most accurate measurement of fair value; however, many times an active market does not exist so other methods have to be used to estimate the fair value on an asset or liability. FAS 157 emphasizes that assumptions used to estimate fair value should be from the perspective of an unrelated market participant. This necessitates identification of the market in which the asset or liability trades. If more than one market is available, FAS 157 requires the use of the “most advantageous market.” Both the price and costs to transact must be considered in determining which market is the most advantageous market.

The framework uses a fair value hierarchy to reflect the level of judgment involved in estimating fair values. The hierarchy is broken down into three levels:

Level 1 Inputs. The preferred inputs to valuation efforts are quoted prices in active markets for identical assets or liabilities, with the caveat that the reporting entity must have access to that market. An example would be a stock trade on the New York Stock Exchange. Information at this level is based on direct observations of transactions involving the identical assets or liabilities being valued, not assumptions, and thus offers superior reliability. However, relatively few items, especially physical assets, actually trade in active markets. If available, a quoted market price in an active market for identical assets or liabilities should be used. To use this level, the entity must have access to an active market for the item being valued. In many circumstances, quoted market prices are unavailable. If a quoted market price is not available, preparers should make an estimate of fair value using the best information available in the circumstances. The resulting fair value estimate would then be classified in Level Two or Level Three.

Example inputs for Level 1 include: New York Stock Exchange prices for securities and New York Mercantile Exchange futures contract prices.

Level 2 Inputs. This is valuation based on market observables. The FASB acknowledged that active markets for identical assets and liabilities are relatively uncommon and that, even when they do exist, they may be too thin to provide reliable information. To deal with this shortage of direct data, the board provided a second level of inputs that can be applied in three situations. The first involves less active markets for identical assets and liabilities; this category is ranked lower because the market consensus about value may not be strong. The second arises when the owned assets and owed liabilities are similar to, but not the same as, those traded in a market. In this case, the reporting company has to make some assumptions about what the fair value of the reported items might be in a market. The third situation exists when no active or less active markets exist for similar assets and liabilities but some observable market data is sufficiently applicable to the reported items to allow the fair values to be estimated.

Example Level 2 inputs are posted or published clearing prices (if corroborated) and a dealer quote for a nonliquid security, provided the dealer is standing ready and able to transact.

Level 3 Inputs. The FASB describes Level 3 inputs as “unobservable.” If inputs from Levels 1 and 2 are not available, the FASB acknowledges that fair value measures of many assets and liabilities are less precise. Within this level, fair value is also estimated using a valuation technique. However, significant assumptions or inputs used in the valuation technique are based on inputs that are not observable in the market and, therefore, necessitate the use of internal information. This category allows “for situations in which there is little, if any, market activity for the asset or liability at the measurement date.” The FASB explains that “observable inputs” are gathered from sources other than the reporting company and that they are expected to reflect assumptions made by market participants.In contrast, “unobservable inputs” are not based on independent sources but on “the reporting entity's own assumptions about the assumptions market participants would use.” The entity may rely on internal information only if the cost and effort to obtain external information is too high. In addition, financial instruments must have an input that is observable over the entire term of the instrument. While internal inputs are used, the objective remains the same: Estimate fair value using assumptions a third party would consider in estimating fair value. This method is also known as mark to management. Despite being “assumptions about assumptions,” Level 3 inputs can provide useful information about fair values (and thus future cash flows) when they are generated legitimately and with best efforts, without any attempt to bias users’ decisions.

Examples of Level 3 inputs are broker quotes that are indicative (i.e., not being transacted on) or not corroborated and models that incorporate management assumptions that cannot be corroborated with observable market data.

Step 5: Determine Fair Value

The outcome of the market determination and the application of valuation technique(s) will be a fair value measurement. To the extent that the valuation was applied to an asset that was valued in use, the total calculated value must be allocated to each unit of account in the asset grouping based on the specific facts and circumstances.

The FASB, after extensive discussions, has concluded that fair value is the most relevant measure for financial instruments. In its deliberations on Statement 133, the FASB revisited that issue and again renewed its commitment to eventually measuring all financial instruments at fair value.

BUSINESS COMBINATIONS (ASC 805, FORMERLY FAS 141R)

In December 2007, the FASB issued Statement of Financial Accounting Standards No. 141 (revised 2007), Business Combinations, (SFAS 141R), now codified in FASB ASC 805, which changes accounting and reporting requirement for business acquisitions. As part of the board's desire to align U.S. accounting practices with international financial reporting standards, FASB ASC 805 requires companies to measure certain contingent liabilities in a merger and acquisition transaction at fair value.

Goodwill is the excess of the purchase price of the acquired enterprise over the sum of the amounts assigned to identifiable assets acquired minus liabilities assumed. Intangible assets acquired in a business combination must be reported apart from goodwill in certain cases. This occurs if assets can be separated or divided from the entity and sold, transferred, licensed, rented, or exchanged. An intangible asset that cannot be sold, transferred, licensed, rented, or exchanged individually is considered separable if it can be sold, transferred, licensed, rented, or exchanged in combination with a related contract, asset, or liability (e.g., core deposit intangibles and the related deposit base) and arises from contractual or other legal rights. Intangible assets that meet the “separable” or “contractual-legal” criteria for recognition include:

- Marketing-related intangible assets, such as trademarks and trade names

- Customer-related intangible assets, such as customer lists and order backlogs

- Creative-type intangible assets, such as books, musical compositions, and photographs

- Contract-based intangible assets, such as licensing agreements, leases, and operating rights

- Technology-based intangible assets, such as patents, domain names, databases, and trade secrets

According to the FASB, the value of an assembled workforce of “at-will” employees acquired in a business combination should be included in the amount recorded as goodwill. “At-will employees” are those employees who are not subject to a contractual employment agreement.

Although goodwill intangibles with indefinite lives are not to be amortized, they must be tested for impairment annually at the reporting unit level. The new “reporting unit” concept refers to the level at which management reviews and assesses the performance of the operating segment. Goodwill-intangible assets are carried on the reporting unit's balance sheet. Nonpublic companies with only one legal entity need only one reporting unit.

FASB ASC 805 establishes these principles and requirements:

- With limited exceptions specified in the statement, an acquirer is required to recognize and measure in its financial statements the identifiable assets acquired, the liabilities assumed, and any noncontrolling interest in the acquiree, measured at their fair values as of the acquisition date. This replaces the original Statement 141's cost allocation method, which resulted not only in not recognizing some assets and liabilities but also in measuring some assets and liabilities at amounts other than their fair values at the acquisition date.

- An acquirer in a business combination achieved in a series of purchases (a step acquisition) is required to recognize the identifiable assets and liabilities as well as the noncontrolling interest in the acquiree at the full amounts of their fair values (or other amounts determined in accordance with this statement), which results in recognizing the goodwill attributable to the noncontrolling interest in addition to that attributable to the acquirer, improving the completeness of the resulting information and making it more comparable across entities.

- An acquirer is required to recognize assets acquired and liabilities assumed arising from contractual contingencies as of the acquisition date, measured at their acquisition-date fair values. An acquirer is required to recognize assets or liabilities arising from all noncontractual contingencies as of the acquisition date, measured at their acquisition-date fair values, only if it is more likely than not that they meet the definition of an asset or a liability in FASB Concepts Statement No. 6, Elements of Financial Statements. If that criterion is not met at the acquisition date, the acquirer instead accounts for a noncontractual contingency in accordance with other applicable generally accepted accounting principles, including Statement 5, as appropriate.

- An acquirer is required to recognize and measure the goodwill acquired in the business combination or a gain from a bargain purchase. FASB ASC 805 defines a bargain purchase as a business combination in which the total acquisition-date fair value of the identifiable net assets acquired exceeds the fair value of the consideration transferred plus any noncontrolling interest in the acquiree, and it requires the acquirer to recognize that excess in earnings as a gain attributable to the acquirer. The original Statement 141 required that “negative goodwill” amount to be allocated as a pro rata reduction of the amounts that otherwise would have been assigned to particular assets acquired, and there was no immediate impact to the acquirer's income statement.

- To allow users of the financial statements to evaluate the nature and financial effects of the business combination, the acquirer is required to make certain specific disclosures or, if disclosure of any of the information is impracticable, the acquirer is required to disclose that fact and explain why the disclosure is impracticable.

FASB ASC 805 applies to all transactions or other events in which an entity obtains control of one or more businesses, including those sometimes referred to as “true mergers” or “mergers of equals” and combinations achieved without the transfer of consideration (e.g., by contract alone or through the lapse of minority veto rights). It applies to all business entities, including credit unions and other mutual entities that previously used the pooling-of-interests method of accounting for some business combinations. It does not apply to (a) the formation of a joint venture, (b) the acquisition of an asset or a group of assets that does not constitute a business, (c) a combination between entities or businesses under common control, and (d) a combination between not-for-profit organizations or the acquisition of a for-profit business by a not-for-profit organization.

FASB ASC 805 applies prospectively to business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after December 15, 2008.

IMPAIRED GOODWILL (ASC 350-20)

Pursuant to accounting rules under Accounting Standards Codification Subtopic 350-20-35-1, goodwill and certain intangibles are not amortized; rather, these assets must be tested periodically for impairment under ASC 350, Intangible–Goodwill and Other.

Under ASC 350, companies must test their goodwill for impairment at three different points in time. The first is the transitional test, which was required at the beginning of the fiscal year in which the statement was adopted. In general, the valuation methods used for the transitional test must be consistent with all subsequent impairment testing. The second type of impairment testing is the interim test, which is required if certain “trigger events” occur, such as adverse changes in the business climate or market that might negatively impact the value of a reporting unit. Finally, companies must also perform annual tests for impairment. However, upon meeting certain criteria, some firms may not require a quantitative annual test.

The goodwill impairment tests consist of two steps. The step 1 impairment test compares the fair value of a reporting unit to its carrying value. If the fair value exceeds carrying value, there is no goodwill impairment and the test is complete. If not, impairment is indicated, requiring a step 2 impairment test. The step 2 test, which is similar to an allocation of purchase price performed pursuant to ASC 805, quantifies the amount of goodwill impairment.

Other hurdles within ASC 350 must be addressed to properly apply these standards. First, companies may have to reclassify their operations into so-called reporting units. Next, intangible assets need to be properly classified and allocated among a company's various reporting units. Additionally, impairment tests of other tangible and intangible assets may need to be conducted prior to performing tests under ASC 350.

Under ASC 805, goodwill should be recognized initially as an asset in the financial statements and measured initially as any excess of the fair value of the acquired business over the fair value of the net identifiable assets acquired. Any acquired intangible assets that do not meet the criteria for recognition as a separate asset should be included in goodwill. ASC 350-20 addresses the subsequent accounting for goodwill, including the requirement that goodwill should not be amortized but should be tested for impairment, at least annually, at a level within the company referred to as the reporting unit. Goodwill cannot be tested for impairment at any level within the company other than the reporting unit level. ASC 350-20 outlines the methodology used to determine if goodwill has been impaired and to measure any loss resulting from an impairment.

In accordance with ASC 350-20, goodwill is tested for impairment at the reporting unit level on an annual basis or upon a triggering event. Impairment is the condition that exists when the carrying amount of goodwill exceeds its implied fair value.

A snapshot of the key tenets of the impaired goodwill world is provided in Exhibit 12.2.

EXHIBIT 12.2 Longitude and Latitude: Impaired Goodwill

| Definition | The amount at which an asset (or liability) could be bought (or incurred) or sold (or settled) in a current transaction between willing parties, that is, other than in a forced or liquidation sale. |

| Purpose of appraisal | To determine the fair value of a company's goodwill-intangible value, as described by SFAS No. 142. |

| Function of appraisal | An acquiring company must test goodwill and intangible assets with indefinite lives for impairment annually at the reporting unit level. |

| Quadrant | Notional regulated. |

| Authority | The FASB and SEC, both of which are located outside of the private capital markets. |

| Economic benefit stream | Operating cash flow (EBITDA minus capital expenditures). |

| Private return expectation | Risk-free rate. |

| Valuation process summary | Fair value constitutes the amount at which an asset or liability could be bought or sold in a current transaction between willing parties. Several methods can be used to determine this amount, such as a comparison to quoted market prices of similar assets. If market transactions are not available, the FASB suggests making a value estimate based on “the best information available under the circumstances.” This generally involves using probability-weighted discounted cash flow techniques and other fundamental analyses. The cost approach is generally considered as a last resort. |

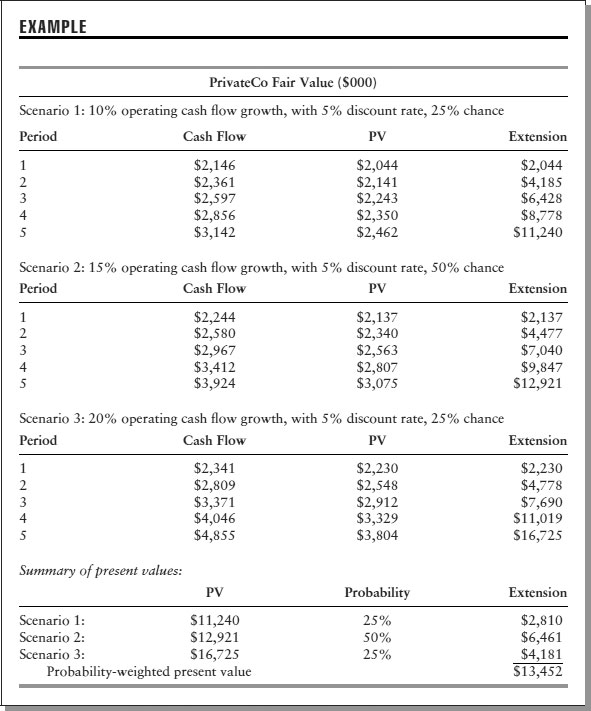

| PrivateCo Example | |

| PrivateCo operating cash flow of $1.951 MM is grown by 10%, 15%, and 20% per year for five years. Management believes the chance of each scenario's growth rate occurring is 25%, 50%, and 25%, respectively. A discount rate of 5% is used. | |

| Long-term debt at the time of the valuation is $500,000 and must be accounted for in the appraisal. | |

| Probability-weighted present value minus LTD | |

| = $13,452,000 – $500,000 | |

| = $13 million (as rounded) |

Impairment Test

Instead of amortizing goodwill, the new rules call for it to be tested at least annually for impairment at the reporting unit level. There are circumstances where the impairment test may be required more than once per year, including:

- A significant adverse change in legal factors or in the business climate

- An adverse reaction or assessment by a regulator

- Unanticipated competition

- A loss of key personnel

- A more-likely-than-not expectation that a reporting unit or a significant portion of a reporting unit will be sold or otherwise disposed of

If a reporting unit experiences none of these special cases, the impairment test should be performed at the same time each year. The requirement for an annual impairment test does not require that the fair value of each reporting unit would have to be recomputed every year. Companies may carry forward a detailed determination of the fair value of a reporting unit from year to year if all of the criteria listed in Exhibit 12.3 are met.

EXHIBIT 12.3 Fair Value Carry-Forward Criteria

|

1. The assets and liabilities that comprise the reporting unit have not changed significantly since the most recent fair value determination. In other words, there has not been a recent acquisition or reorganization of an entity's reporting structure. 2. The most recent fair value determination resulted in an amount that exceeded the carrying amount of the reporting unit by a substantial margin. 3. Based on an analysis of events that have occurred and circumstances that have changed since the most recent fair value determination, it is unlikely that a current fair value determination would be less than the current carrying amount of the reporting unit. There have been no adverse changes in the key assumptions or variables used in the previous fair value computation. |

Once companies complete the initial detailed valuations of reporting units, it may be possible to update those valuations periodically without incurring the cost of the original valuations.

The impairment test calls for the following steps:

Step 1: Determine the Fair Value of the Reporting Unit

The fair value of the reporting unit's equity, including goodwill, is compared to its book value. If the fair value of equity exceeds its book value of equity, then no impairment is indicated and no further testing is required.

Step 2: Calculate the Implied Fair Value of Goodwill

Calculate the implied fair value of goodwill by deducting the fair value of all tangible and intangible net assets of the reporting unit from the fair value of the reporting unit (as determined in step 1). In this step, companies must allocate the fair value of the reporting unit to all of the reporting unit's assets and liabilities, which is akin to a hypothetical purchase price allocation. The remaining fair value of the reporting unit after assigning fair values to all of the reporting unit's assets and liabilities represents the implied fair value of goodwill for the reporting unit.

If fair value is less than the book value, the implied fair value of goodwill is compared to its book value. Impairment loss is recognized equal to the excess of the book value of goodwill and the implied fair value of the goodwill. This becomes the new carrying value of goodwill for that reporting unit, which will be used in future impairment tests.

There are two noteworthy items here.

1. Public and nonpublic companies that follow GAAP are required to complete the impairment test each year.

2. Intangible assets with indefinite lives should not be amortized until their lives are determined to be finite. Intangible assets with finite lives should be amortized over their useful lives.

VALUATION

Fair value measurement constitutes the amount at which a reporting unit could be sold in a current transaction between willing parties. An independent valuation professional should perform this appraisal and probably will rely on:

- Comparison to quoted market prices (public companies only). The FASB states that the best evidence of fair value is quoted market prices in an active market and should be used if available.

- Prices for similar assets. When quoted market prices are not available, which is the typical situation, the estimate of fair value should be based on the best information available, including prices for similar assets and liabilities and the results of other valuation techniques.

- Other valuation techniques, such as multiples of earnings. A valuation technique based on multiples of earnings or revenue or a similar performance measure may be used if that technique is consistent with the objective of measuring fair value. Use of multiples of earnings or revenue in determining the fair value of a reporting unit may be appropriate, for example, when the fair value of an entity that has comparable operations and economic characteristics is observable and the relevant multiples of the comparable entity is known. Conversely, use of multiples would be inappropriate in situations in which an entity's operations are not of a comparable nature, scope, or size as the reporting unit.

- Present value techniques, with a reliance on probability-weighted analysis. The FASB believes present value is often the best available technique with which to estimate the fair value of a group of net assets (such as a reporting unit). If a present value technique is used to measure fair value, estimates of future cash flows used in that technique shall be consistent with the objective of measuring fair value. Cash flow estimates shall incorporate assumptions marketplace participants would use in their estimates of fair value. If that information is not available without undue cost and effort, any entity may use its own assumptions. Those cash flow estimates shall be based on reasonable and supportable assumptions and shall consider all available evidence. The weight given to the evidence shall be commensurate with the extent to which the evidence can be verified objectively. If a range is estimated for the amounts or timing of possible cash flows, the likelihood of possible outcomes shall be considered.

The FASB believes these six elements should be incorporated into the discounted cash flow model:

1. An estimate of the future cash flow or, in more complex cases, a series of future cash flows at different times

2. Expectations about possible variation in the amount or timing of those cash flows

3. The time value of money, represented by the risk-free rate of interest

4. The price for bearing the uncertainty inherent in the asset or liability

5. Unidentifiable factors, such as illiquidity and market imperfections

6. The effect of an entity's credit standing on liabilities

According to the FASB, estimated cash flows and interest rates should reflect the range of possible outcomes rather than the single most likely, minimum, or maximum possible amount.

As an example, assume PrivateCo needs to be valued using probability-weighted present value analysis. Three scenarios are analyzed:

1. PrivateCo's EBITDA less capital expenditures (operating cash flow) is expected to grow by 10% per year. Management believes this has a 25% chance of occurrence.

2. PrivateCo operating cash flow grows by 15% per year, with a 50% chance of occurrence.

3. PrivateCo's operating cash flow grows by 20% per year with a 25% chance of occurrence.

By using a 5% risk rate, the weighted present value can be derived as shown in the next example.

The probability-weighted expected present value of $13.452 million is higher than the most likely estimate ($12.921 million has a 50% probability of occurrence).

The FASB provides little additional guidance to determine fair value. The regulators are silent on whether companies would be expected to obtain outside appraisals in certain situations.

Example of Measuring Impairment

Step 1 of the impairment test requires determining the fair value of the reporting unit. The results of the fair value determination are then used in the comparison of the fair value to the carrying value, including goodwill, of the reporting unit.

EXAMPLE

At the time of the annual test, BigPrivateCo is a reporting unit with a book value of $20 million, including goodwill of $6 million. The fair value of BigPrivateCo has also been determined to be $15 million. Also assume that none of the recognized assets of BigPrivateCo other than goodwill is impaired.

| Book value of BigPrivateCo, including goodwill | $20 million |

| Fair value of BigPrivateCo | $15 million |

Because BigPrivateCo's book value is greater than its fair value, step 1 of the test is failed, and BigPrivateCo will have to complete step 2 in order to measure the impairment loss. If the book value, including goodwill, of BigPrivateCo had been $13, no further action would have been required.

Step 2 of the impairment test requires a calculation of the implied fair value of goodwill. The implied fair value of goodwill is calculated in the same manner as goodwill in a business combination. The allocation is performed as if the reporting unit had just been acquired and the fair value of the reporting unit was the purchase price.

EXAMPLE

BigPrivateCo, after failing step 1, has determined these values:

| Fair value of BigPrivateCo | $15 million |

| Net fair value of BigPrivateCo's assets and liabilities | |

| including unrecognized intangible assets | $10 million |

| Implied fair value of goodwill | $5 million |

| Carrying value of goodwill | $6 million |

| Impairment loss to be recognized | $ (1) million |

BigPrivateCo reflects an impairment loss of $1 million in operating income and the new carrying value of goodwill for BigPrivateCo is $5 million.

If BigPrivateCo's implied fair value of goodwill increases in the subsequent years, say from $5 million to $7 million, there will be no write-up of goodwill. Goodwill can be written down but not written up.

TRIANGULATION

The FASB does not emanate from the capital or transfer sides of the private capital markets. It regulates a market it does not call home. Unintended consequences often occur in these circumstances. Since it oversees U.S.-based accounting standards, the FASB's main control and sanctioning power is over accounting auditors. Presumably auditors will not sign off on an audit unless the goodwill impairment test is completed properly. Because it is in management's interest to limit the amount of actual goodwill write-offs, this becomes one more negotiating item between management and its auditors. Since fair valuation is more art than science, this situation has the potential for conflicts of interest between auditors and owner-managers.

The FASB is a creator of value worlds. This chapter highlights several new worlds. These worlds are notional, as they cannot be observed in the marketplace. These worlds are also highly regulated, as they are whatever the FASB says they are. An interesting sidebar concerning the FASB's motives in creating these new statements is its desire to converge with international accounting standards already put in place by the International Accounting Standards Board (IASB). The FASB and IASB are working toward the creation of global accounting standards. Of course, this makes sense, given the trend toward globalization of trade.

FAS 157 is having a major impact on private companies and how they determine and report asset and liability values. This is especially true for private equity groups and other larger private companies that are could-be-public entities. Transparency is important to these companies, as financial audits are routine, and going public may be a goal. It is not totally clear what effect FAS 157 will have on private companies that never receive an accounting audit.

ASC 805 addresses how companies should account for merger and acquisition transactions for financial reporting purposes. The acquirer must follow the dictates of this statement in order to record the fair value of the assets and liabilities it acquires. As with the other FASB value worlds, the goal of this world is to provide more consistency and comparability between reporting entities.

ASC 350-20 describes the process of determining if the fair values of any assets on the financials may have dropped below their carrying value after the transaction is closed. When such a condition exists, the entity is subject to an impairment test. According to the example in this chapter, PrivateCo's fair value in this world is $13 million. This world is unusual in its relationship to the transfer side of the triangle. Prior transfers cause this world to exist. Impaired goodwill can exist only if a prior acquisition caused goodwill to form on the acquirer's balance sheet. ASC 350-20 may affect future acquisitions, however. Because goodwill is not recognized in asset sales, buyers of smaller, private companies have one more reason to acquire the assets of the target rather than its stock. With asset sales of C corporations, sellers may realize less money on the sale of their business because taxes are generally higher on asset sales than stock transactions.

Purchase price allocation has become more important since the implementation of Statements 805 and 350. The purchase price is allocated between the tangible assets, and the remainder is allocated to intangibles. The private buyer will want to allocate as much as possible to intangibles with finite lives so amortization is maximized. This helps create a noncash expense in the future and reduces income taxes.

| World | PrivateCo Value |

| Asset market value | $2.4 million |

| Collateral value | $2.5 million |

| Insurable value (buy/sell) | $6.5 million |

| Fair market value | $6.8 million |

| Investment value | $7.5 million |

| Impaired goodwill | $13.0 million |

| Financial market value | $13.7 million |

| Owner value | $15.8 million |

| Synergy market value | $16.6 million |

| Public value | $18.2 million |

Under ASC 350, the pricing of deals with a high level of intangibles should decrease in the future because of the risk of impairment write-downs. Market volatility plays a part here because there is no reversal of an impairment loss should the fair value subsequently recover.

A company's capital structure is affected by impaired goodwill. A write-off due to impairment decreases shareholder equity. A reduction in equity, while not a cash loss, may affect a company's covenant position with its lenders. Certain ratios, such as debt to equity, are changed as a result of a write-off. Some banks use a covenant break to change the fee structure of the loan, which adds expense to the borrower. Of course, a lower equity figure makes it more difficult for a borrower to secure adequate financing.