CHAPTER 22

Mezzanine Capital

Mezzanine capital is subordinated debt that provides borrowing capability beyond senior debt while minimizing the dilution associated with equity capital. It may be secured through a second lien on assets, or it may be secured by company stock. Since it forms an additional layer of debt, it carries more risk for the lender than normal or senior debt. It ranks behind senior debt for purposes of principal and interest repayment. Mezzanine capital is generally the lowest-ranking debt obligation in a borrower's capital structure. Compared to a bank loan, it contains a fairly loose covenant package. These factors make mezzanine debt more expensive than senior debt for the borrower. Nevertheless, it remains cheaper than institutional equity investment and may be available when the supply of equity is limited.

The mix of senior and mezzanine debt is influenced by a borrower's cash flow projections, because mezzanine capital typically is repaid either in installments or in one balloon payment at the end of the term. Mezzanine capital is an appropriate financing option in situations where access to conventional bank debt may be limited because of a lack of tangible assets or strong guarantor, an unduly conservative assessment of a company's prospects, or when the dilution implied by raising additional equity capital is unattractive. This chapter describes mezzanine capital for private companies in need of $1 million to $25 million.

Mezzanine financing is used during transitional periods in the life of a company when extra financing is required. It is not the answer for day-to-day operations needs. Mezzanine loans are used for long-term or permanent working capital, equipment purchases, management buyouts, strategic acquisitions, recapitalizations, new product development, and other worthwhile business purposes. In situations where a company's banker is unable to fully meet its credit needs, business owners have three options for raising additional capital: (a) sell equity in the business, (b) borrow from a mezzanine lender, or (c) invest further in the business, which typically is only considered after the first two options have been exhausted. Business leaders who need a substantial investment, yet do not want to concede large amounts of equity or control, find mezzanine financing attractive. Exhibit 22.1 provides capital coordinates for mezzanine capital.

EXHIBIT 22.1 Capital Coordinates: Mezzanine Capital

|

|

| Capital Access Point | Mezzanine Capital |

| Definition | Subordinated debt that relies on cash interest, payment in kind, plus warrants for its return |

| Required rate of return | 19.5% (based on equity mezzanine example) |

| Likely provider | SBICs, private funds |

| Value world(s) | Market value |

| Transfer method(s) | Private and public auctions |

| Appropriate to use when … | The investee is experiencing high growth and possible profitability but has little free liquidity. Mezzanine is often the next type of capital to add to the capital structure if senior lending becomes restricted because mezzanine is less expensive than equity. |

| Key points to consider | Beyond the 12% to 15% cash and payment-in-kind interest rate, a provider will structure a warrant position. The longer this warrant goes unexercised, the more costly it becomes to a growing investee. |

| Performance ratchets may be used to incentivize management to reach performance targets. | |

LOAN STRUCTURE

The structure of mezzanine loans accommodates the financing needs of growing companies. The mezzanine investor predicates the investment decision on the firm's cash flow and projected growth rather than on collateral. Regardless of whether the mezzanine loan is secured, the mezzanine investor presumes there will be little or no recovery of principal from liquidation. The investment is priced accordingly. However, the investor may require a subordinate claim on corporate assets to the senior secured lender or a senior claim on the stock of the investee, which is the company that receives the investment. The terms of a mezzanine deal are usually flexible, generally involving 5- to 7-year maturities combined with amortizations ranging from 5 to 15 years. Repayment of principal usually is deferred until later in the loan term, and it is scheduled to fit the borrower's needs and cash flow projections.

Mezzanine providers earn a return by making investments with any of the next combinations:

- Cash interest. A periodic payment of cash (called a coupon) based on a percentage of the outstanding balance of the mezzanine financing. The interest rate can be either fixed throughout the term of the loan or can fluctuate (i.e., float) along with prime or LIBOR (London Interbank Offered Rate) or other base rates.

- Payment-in-kind (PIK) interest. Payment-in-kind interest is a periodic form of payment in which the interest payment is not paid in cash but rather by increasing the principal amount by the amount of the interest (e.g., a $10 million bond with an 3% PIK interest rate will have a balance of $10.3 million at the end of the period but will not pay any cash interest).

- Warrant. Along with the typical interest payment associated with debt, mezzanine capital often includes an equity stake in the form of attached warrants, similar to that of a convertible bond. Mezzanine providers use warrants as a way to increase their return, as opposed to converting into the investee's stock.

Cash Interest

According to the Pepperdine Private Capital Markets survey, cash interest varies slightly by size of funding, with a median for all deal sizes of 12% to 13%.1 For some mezzanine deals, the loan will be interest-only for one to two years, then the principal will be amortized over some period, with a balloon payment due at maturity. Mezzanine providers are extremely flexible in structuring deals to meet the needs of the borrower, and in many cases the loan will be interest-only for the life of the loan.

Payment in Kind

PIK is used to describe interest or dividend income that is paid by a borrower through the issuance of a new security instead of through periodic cash payments. Instead, the mezzanine lender receives cash when the new security is liquidated or repaid at the end of the loan term.

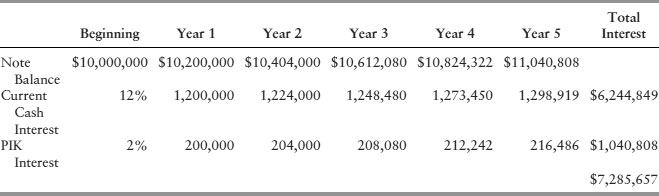

Here is a basic example of how PIK works: Assume MezzCo lends PrivateCo $10 million. MezzCo charges the company 12% in current cash interest and 2% in PIK interest. For this example, assume the lender does not receive any warrants in PrivateCo, and, as a result, the stated interest rate is 14% (or 12% plus 2%). If the note is due in five years, MezzCo will earn interest income from the $10 million note as shown in Exhibit 22.2.

EXHIBIT 22.2 Mezzanine PIK Interest

The current interest, $1.2 million, is paid in cash as required by the note. The PIK interest, $200,000, is paid in a security and is added to the principal amount of the note, increasing that amount to $10.2 million after Year 1. MezzCo will receive the PIK interest in cash when the note is paid at maturity. The PIK effectively increases the lender's return beyond the stated 14% interest rate due to compounding interest.

Mezzanine lenders use a PIK interest component when they want to improve the certainty of their investment return. The PIK portion of the return is contractually certain. Since it also compounds the return, this method allows the lender to lock in an investment return. An added benefit to PIK is that it is paid in a debt security that is senior in the portfolio company's capital structure to the equity securities that otherwise would have been received upon exercise of a warrant. In other words, PIK notes have preference in liquidation to equity securities.

Warrant

In addition to the loan feature, most mezzanine deals also include warrants to help increase the yield to the investor. A warrant is a right to buy a security at a fixed price, also known as the exercise or strike price. Warrants can be traded as independent securities. Mezzanine investments may include detachable warrants, which means the warrants can be repurchased by the borrower, normally at a predefined strike price or under defined valuation procedures, or sold to other investors. As an enticement to the investor, typically the warrants are nominally priced, which causes them to be called penny warrants.

Mezzanine investors often work backward to determine the number of warrants they need in a deal. For example, if a mezzanine investor desires a 25% return from a particular investment, she may consider the return from the coupon and then analyze the most likely projections from the borrower to determine the required warrant valuation to achieve the return.

Exhibit 22.3 describes cash interest, PIK, and warrant terms for various loan sizes for nonsponsored deals.2

EXHIBIT 22.3 Mezzanine Terms by Loan Size for Nonsponsored Deals

Nonsponsored deals are those that have no private equity group or other institutional funding participation. By way of reference, sponsored deals tend to achieve better terms for the borrower.

There are three noteworthy items regarding mezzanine terms:

1. The cash interest rate is surprisingly similar for such a wide spread of deal sizes.

2. All small deals employ warrants to help generate returns to the provider. But larger deals rely more on the total interest rate percentage than on the warrant for a return.

3. Median expected returns on a pretax basis decrease with deal size. Another way of stating this return is as a gross cash-on-cash pretax internal rate of return.

MEZZANINE INVESTORS

Several types of institutional providers offer lower-middle-market mezzanine capital. These companies make mezzanine investments usually in amounts of $500,000 to $50 million per deal. Investor types are funds, frequently organized as Small Business Investment Companies (SBICs); insurance companies; banks; and other providers, composed of economic development boards, including state and local commissions. According to Private Equity Information, a private equity information database, there are approximately 160 mezzanine providers in the market, not including SBICs.3 As of this writing, there are about 300 SBICs in operation. Many SBICs provide mezzanine capital. They are the most uniformly structured of the mezzanine players, so they are described at some length here.

Small Business Investment Companies

More than 50 years ago, an entrepreneur looking for the capital to launch a small business had few capital alternatives. Very few institutional resources were available to back up promising but untried ideas. In 1958, the U.S. Congress created the Small Business Investment Company (SBIC) program to help solve this problem. Licensed by the Small Business Administration (SBA), SBICs are privately owned, profit-motivated investment firms. They are participants in a partnership between government and the private sector economy. Using their own capital and funds borrowed at favorable rates through the federal government, SBICs provide loans and venture capital to new and established small, independent businesses.

Loans and Debt Securities

SBICs make long-term loans to small businesses for their sound financing, growth, modernization, and expansion. An SBIC may provide loans independently or in cooperation with other public or private lenders. SBIC loans to small business concerns may be secured, but the SBA does not mandate this. Such loans may have a maturity of no more than 20 years, although under certain conditions the SBIC may renew or extend a loan's maturity for an additional 10 years.

An SBIC may elect to loan or invest money in a small business concern in one of three ways: loans, debt security, or equity. Debt securities are loans for which the small business concern issues a security, which may be convertible into equity or contain rights to purchase equity in the small business concern. These securities also may have special amortization and subordination terms. By law, the SBIC must work only with small, private business concerns and may do so by purchasing the small business concern's equity securities. The SBIC may not, however, become a general partner in any unincorporated small business concern or become otherwise liable for the general obligations of an unincorporated concern. The average loan size for an SBIC is approximately $1.2 million.4

Types of Businesses

SBICs may invest only in qualifying small business concerns as defined by SBA regulations. SBICs may not invest in:

- Other SBICs

- Finance and investment companies or finance-type leasing companies

- Unimproved real estate

- Companies with less than one-half of their assets and operations in the United States

- Passive or casual businesses

- Companies not engaged in a regular and continuous business operation

- Companies that will use the proceeds to acquire farmland

An SBIC is not permitted to control, either directly or indirectly, any small business on a permanent basis. Nor may it control a small business in participation with another SBIC or its associates. In certain instances, the SBA may allow an SBIC to assume temporary control to protect its investment. But in those cases the SBIC and the small concern must have an SBA-approved plan of divestiture in effect. Without written SBA approval, an SBIC may invest no more than 20% of its private capital in securities, commitments, and/or guarantees for any one small concern.

Loans made to and debt securities purchased from small concerns should have minimum terms of five years. The small concern has the right to prepay a loan or debt security with a reasonable penalty when appropriate. Loans and debt securities with terms less than five years are acceptable only when they are necessary to protect existing financings, are made in contemplation of long-term financing, or are made to finance a change of ownership.

Other Mezzanine Providers

Many private mezzanine funds are unaffiliated with the federal government. State or local economic development boards control some of these funds. Other funds are offered through private equity groups or finance companies looking to provide most or all of the capital structure needs of the borrower. Finally, some insurance companies invest in larger deals involving higher-quality companies. Insurance companies tend to view mezzanine lending from an institutional, debt-oriented point of view and therefore are more concerned with current interest payments and scheduled return of capital. The remainder of this chapter does not differentiate between various structures of mezzanine funds. Rather, it focuses on the investment orientation of mezzanine funds in general.

TARGETED INVESTMENTS

Mezzanine investors look for businesses that have high potential for growth and earnings but currently are unable to obtain sufficient bank funding to achieve their goals. This may be because of a lack of collateral or guarantor, higher balance sheet leverage, or a variety of other reasons. As risk lenders, mezzanine investors consider investment opportunities outside conventional commercial bank parameters. Ideally mezzanine investors prefer companies that, in a three- to five-year period, can exit mezzanine financing through debt from a senior lender, an initial public offering (IPO), or sale of the company. In addition to these financial criteria, SBIC investors view the quality of the people involved as critical.

Strong management is important, and mezzanine investors look closely at an entrepreneur's hands-on operating achievement and proven management ability. The track record of a company's management team is a valuable indicator of its ability to achieve future success. Mezzanine investors are not interested in situations such as seed capital funding, early-stage financing, research and development funding, and problem situations.

Investment Preferences

Mezzanine capital is the flexible bridge between secured senior debt and equity capital. Flexibility is very important since the mezzanine capital may be close to senior debt, herein called debt mezzanine capital (DMC), or closer to equity, called equity mezzanine capital (EMC). The marketplace does not refer to DMC or EMC; rather, mezzanine funds tend to focus on one or the other and structure deal terms based on how they view the subject. Since all-in returns for DMC and EMC can be quite different, each will be described separately. Exhibit 22.4 describes characteristics of each mezzanine type.

EXHIBIT 22.4 Investor Preferences

| Debt Mezzanine Capital | Equity Mezzanine Capital |

| Subject has adequate free cash flow. | Subject has little free liquidity. |

| For stable, high-profit companies. | For high-growth companies. |

| Mezzanine fills the “stretch” piece. | Mezzanine fills the equity piece. |

| Capital preservation is goal. | Capital appreciation is goal. |

| Partners incentivized partly on upside. | Partners incentivized mainly on upside. |

| Bank-driven deals. | Equity-driven deals. |

DMC is the debt-oriented type of mezzanine capital used where the invested company is profitable with continuing growth prospects. Typical applications for DMC are strong management buyout or management buy-in transactions as well as later-stage company expansions, where a strong operating leverage can be achieved.

EMC is the type of mezzanine financial instrument available for growth companies with an ambitious business plan resulting in less financial liquidity. Therefore, the mezzanine investor provides the financing with a lower-than-adequate running yield but a higher-equity kicker, offsetting the risk-capital aspects of the investment. Equity mezzanine investors seek to fund pre-IPO situations, acquisitions of small and medium-size companies, and high-growth situations.

PRICING

Mezzanine financing presents a fairly high degree of risk to the investor, so it is far more expensive than a bank loan. The price of mezzanine debt typically includes a base interest or “coupon” rate on the loan with an additional pricing vehicle to ensure that the investor participates in the success (or failure) of the business. This vehicle takes the form of a stock warrant or a royalty, often called a success or revenue participation fee, which is based on the growth of the business. The pricing is structured to fit the unique characteristics of the business and the deal.

The portion of the pricing that rewards the investor based on the firm's success should be carefully considered. A high warrant position may have disadvantages and costs similar to those of a straight equity investment. Mezzanine investors that do not use a high level of warrants usually have a lower cost, have fewer management control features, and employ an easier exit strategy. Instead of using an equity-based vehicle, these investors base a portion of the pricing on the firm's measurable financial success during the loan term, using a fee-based formula tied to the firm's income statement.

If the company wishes to exit the mezzanine investment prematurely, it may face sizable costs, including a prepayment penalty or a yield maintenance calculation to ensure that the investor is guaranteed a minimum return on the investment. These costs should be defined up front to ensure a smooth exit strategy.

Pricing terms are different between debt and equity mezzanine deals. This is reasonable since the riskiness of the investment positions can be quite different.

DEBT MEZZANINE CAPITAL

Debt-oriented mezzanine investors tend to focus their investments on capital preservation, investing in transactions with consistent historical cash flows, conservative capital structures, and a strong equity sponsor. Insurance companies often fill this role. In spite of having large amounts of capital to invest, they tend to operate with relatively small staffs and therefore have less time to devote to understanding a potential investment.

Exhibit 22.5 shows the credit box and sample terms for DMC.5 Since there are numerous debt mezzanine players with constantly changing investment appetites, prospective investees should canvass the market to determine the current credit box and terms offered.

EXHIBIT 22.5 Debt Mezzanine Credit Box and Sample Terms

| Credit Box | |

| To qualify for debt mezzanine capital, an applicant must: | |

|

|

| Sample Terms | |

| Example loan | $25 million loan |

| Cash interest rate | 12% fixed (prime = 3.5%) |

| PIK rate | 2% fixed |

| Term | 5 years |

| Principal amortization | Equal quarterly payments |

| Detachable warrants | None |

| Commitment fee | .3% of loan |

| Closing fee | 1% of loan |

The credit box describes the qualities necessary to access DMC. While many of the characteristics are qualitative in nature, each has a quantitative corollary. For example, “employ a conservative capital structure” might also be stated as “mezzanine debt to net worth shall not exceed 3.5 to 1.” Also, historical and future cash flows coverage ultimately breaks down to ratios and numbers. A strong equity sponsor may be the most important item in the credit box. This equity partner may represent a private equity group or current ownership with financial depth. Since debt mezzanine investors do not knowingly put themselves at equity risk, they must have a capable equity partner.

Exhibit 22.5 is an illustration of the terms a typical debt mezzanine deal might convey. In this case, the interest rate is fixed at 14%, with 12% representing the cash interest rate and 2% in PIK interest. At the end of five years, the borrower's option to defer interest shall cease, and all deferred interest shall be due and payable. With a $25 million loan, this means that the current coupon is paid at $250,000 per month ($25 million × 12% ÷ 12 months), with the PIK adding $500,000 per year to the note ($25 million × 2%). The borrower will pay the PIK interest at the maturity of the note. In this example, the mezzanine provider is not using warrants to enhance the return.

The next figures show the expected return to the debt mezzanine provider.

| 1. Total interest cost ($25 million loan × 14% interest rate) | $3,500,000 |

| 2. Commitment fee ($25 million loan amount × .3% ÷ 5 years) | 15,000 |

| 3. Closing fee ($25 million loan amount × 1% ÷ 5 years) | 50,000 |

| Annual returns of loan | $3,565,000 |

| Expected rate of return | 14.3% |

| ($3,565,000/$25,000,000) |

The cash interest rate of 12% plus the PIK rate of 2% and the “terms cost” of .3% yields an expected rate of return of 14.3%. For ease of presentation, the amortization of the PIK interest and fees are shown on a noncompounded basis.

EQUITY MEZZANINE CAPITAL

Equity-oriented mezzanine investors tend to be more interested in capital appreciation. They focus on companies with more volatile earnings, less experienced equity sponsors, and riskier future projections. Most mezzanine funds favor this approach because the general partners are incentivized by upside capital growth. Exhibit 22.6 shows a credit box and sample terms for EMC.6

EXHIBIT 22.6 Equity Mezzanine Credit Box and Sample Terms

| Credit Box | |

| To qualify for equity mezzanine capital, an applicant must: | |

|

|

| Sample Terms | |

| Example loan | $7 million loan |

| Interest rate | 12% fixed, payable monthly (prime = 3.5%) |

| PIK interest | 2% |

| Term | Interest only for 12 months; monthly principal + interest on 10-yearamortization, with all principal due in 5 years |

| Detachable warrants | 5% of the fully diluted common |

| Commitment fee | 1% of loan |

| Closing fee | 2% of loan |

The credit box describes the qualities necessary to access EMC. Perhaps the most important combination of factors is a strong management team that can scale the business model. “Scalability” means that as the company grows, profits grow at an increasing rate. This usually creates substantial stock appreciation in a fairly short period of time. An example of a scalable business model is the creation of an interrelated family of software programs. Once the platform program is written, other similar programs can be created for other sales channels. Since most of the cost is incurred for the initial launch, future sales have a much smaller cost component.

Sample terms illustrate terms that a typical equity mezzanine deal might convey. In this case, the interest rate is fixed at 14% (cash interest rate of 12% and PIK interest of 2%), interest only is charged for the first 12 months, and then principal is amortized using a 10-year amortization schedule. Principal repayment is due in full at the end of the fifth year.

In this example, detachable warrants of 5% of the common stock are included in the deal. These warrants are valued separately from the loan, and the terms for the equity valuation normally are predefined in the agreements. The enterprise equity value is determined as the greater of these valuation procedures:

- The company's book value

- Eight times the company's average net profits before taxes for the prior two years (restated for shareholder compensation greater than $150,000) less long-term debt

- Six times the company's earnings before interest, taxes, depreciation, and amortization (EBITDA) for the prior year (restated for shareholder compensation greater than $150,000) less long-term debt

Warrant value is 5% of the equity value for this example. To illustrate the determination of this equity value, the year 5 numbers for the three valuation criteria are given. By that point, book value is estimated at $9 million, annual average net profits are $4.2 million, and the restated EBITDA is $5.75 million. Once again, it is assumed that the company has no long-term debt. The expected equity value in year 5 is:

Book value = $9 million

Net profits calculation: 8 × $4.2 million = $33.6 million

EBITDA calculation: 6 × $5.75 million = $34.5 million

The highest valuation is the EBITDA formula, or $34.5 million. The warrants are therefore expected to be worth $1.73 million in year 5 ($34.5 million × 5%).

The expected rate of return to the equity mezzanine can now be calculated:

| 1. Total interest cost ($7 million loan × 14% interest rate) | $980,000 |

| 2. Warrant cost ($1.73 million spread over 5 years) | 346,000 |

| 3. Commitment fee ($7 million loan amount × 1% ÷ 5 years) | 14,000 |

| 4. Closing fee ($7 million loan amount × 2% ÷ 5 years) | 28,000 |

| Annual returns of loan | $1,368,000 |

| Expected rate of return | 19.5% |

| ($1,368,000/$7,000,000) |

The stated interest rate of 14% is increased by the “terms cost” of 5.5%, which yields an expected rate of return to the provider of 19.5%. Once again, for purposes of this presentation, the various costs and fees are amortized on a noncompounded basis.

OTHER DEAL TERMS

Numerous terms and conditions are involved in closing a mezzanine loan. These are described in the term sheet and legal documentation.

Tranches

Borrowers may have capital needs that need funding over several years, such as a project or division build-out. In these cases, the borrower still wants to arrange the entire capital structure but to draw the funds as needed. In mezzanine terms, a funding commitment describes the entire amount of capital needed by the borrower and committed by the mezzanine provider. The borrower then draws tranches as needed. Normally there are minimal tranche amounts available. For example, a mezzanine provider may make a $10 million commitment, with $2.5 million tranches available to the borrower. The borrower may not be required to draw all of the tranches, but the commitment by the mezzanine provider will be available for some period of time. The terms of each tranche are negotiated between the parties at the time of the total commitment.

Warrant Terms

To avoid the possibility that the borrower may not repurchase the warrants, investors create warrants with a variety of equity features, such as:

- Tag-along rights. A procedure used to protect a minority shareholder when a majority shareholder sells his stake. The minority shareholder has the right to join the transaction and sell his minority stake in the company.

- Drag-along rights. A right that enables a majority shareholder, in the sale of a company, to force a minority shareholder to join in the sale. The majority owner doing the dragging must give the minority shareholder the same price, terms, and conditions for the security being sold as any other seller.

- Piggyback registration. When an underwriter allows existing holdings of shares in a corporation to be sold in conjunction with an offering of new shares.

- Antidilution rights. An investor's shares in a company cannot be diluted if the company issues more stock, such as in issuing grants to employees. Chapter 23 describes these rights in detail.

- Voting rights. An investor requests certain rights in governing activities, such as a right to veto in decisions concerning whether a company sells itself or merges with another.

- Registration rights. These rights govern how a company goes public, who pays the costs associated with the process, and how many times a company can file an IPO. In general, these rights are determined much further along in the process, and in many cases the investment bank handling the offering sets the terms.

All of these warrant terms are explained further in Chapter 23.

Prepayment Premiums

Most mezzanine loans have prepayment penalties. These penalties usually are stated as a percentage of the unpaid loan balance. According to the Pepperdine survey, median prepayment penalties by year are: 5%, 3.5%, 3.0%, 2.0%, and .8% respectively. Nearly all loans require payment in full, including penalties, if the loan is prepaid.7

Covenants

Mezzanine investors rely on covenant protection because there probably is insufficient collateral coverage. Typical covenants include:

- Cross-default and cross-acceleration provisions

- Minimum fixed-charge and interest-coverage tests

- Total debt, capital expenditure, dividend, and management fee limitations

- Maximum total indebtedness to cash flow test

- Change in business management and control restrictions

- Limitations on dividends and distributions

- Caps on compensation and pay raises to senior management

- Sale of assets and merger and acquisition limitations

It is also typical for the lender to charge a default interest rate in the event of a major default. This rate may be 5% to 6% above the stated rate and is in force until the default is cured.

Subordination

The mezzanine lender must work out a subordination agreement with the senior lender before closing the loan with the borrower. The subordination agreement spells out the relative rights and responsibilities of each lender. These include cross default; cross acceleration; and a standstill period, which is a limited period of suspension of rights and remedies. Some collateral of the subordinated or junior lenders can be specifically excluded from the agreement, such as life insurance and stock pledges, provided the senior lender does not claim the same collateral.

Debt subordination is a contractually established relationship between lenders to a single borrower. Subordination terms set the relationships between the parties. Primarily, the junior creditor “subordinates” to the senior creditor its right to receive payments from the debtor. In extreme cases, subordinated debt will be placed so low in the capital structure that it is tantamount to equity. Basically, there are three types of subordination:8

1. Total or complete subordination. No payments on junior debt at all until senior debt is paid in full. Definitions of Junior and senior debt are worded broadly. This level of subordination is often accompanied by a complete block on remedies.

2. Partial subordinations. Certain specific payments are permitted to be made to the junior creditor (e.g., interest). In a closely held corporation, salary, dividends, and the like might also be permitted. Principal payments may be allowed, although in a limited fashion. Payments can be stopped, however, upon the occurrence of certain events, such as a senior loan default.

3. Contingent subordination. This level of subordination allows all scheduled payments to be received until the occurrence of certain events, such as insolvency.

In almost all cases, a well-written subordination agreement prohibits prepayments of subordinated debt.

Subordination, also called intercreditor agreements, must be negotiated with care. Some banks also offer mezzanine capital along with the senior loan, which makes the subordination issues easier.

Board Seats and Visitation

Investors usually get one or more seats on the board of directors, or they have visitation rights to attend board meetings and meet with management on a periodic basis. They also receive information such as monthly operating reports and quarterly unaudited and annual audited financial statements. Separate approval of the directors appointed by the investor may be required for items such as major capital expenditures, borrowing from banks, approving management compensation and stock option plans, and deviations from previously approved business plans.

NEGOTIATING POINTS

Raising mezzanine capital is a complicated process. This is not a good time to “learn on the job.” It is recommended that those inexperienced in this area should hire an investment banker or other professional who has already completed many deals. The next negotiating points help cut a better deal.

Warrant Position and Valuation

The size of the warrant and its valuation are totally negotiated items. The mezzanine lender proposes a certain warrant position in an attempt to meet its return expectation. Typically, warrants have a nominal price to the investor (i.e., penny warrants). Usually the size of a lender's warrant position is inversely related to the interest rate; that is, the higher the interest rate, the fewer the warrants required. Since the interest from a mezzanine loan is tax deductible and a warrant payoff is not, it may make sense for a borrower to put more weight on the coupon and less on the warrant.

The valuation procedures for the warrant are tailored to each deal and therefore have a lot of room for negotiation. Borrowers should not blindly accept formulas for valuing the warrant. The proper deal should mirror the marketplace for similar equity interests.

Warrant Exercise Date

Typically, the cost of buying a detachable warrant increases the longer it is in force. For example, borrowers should seek to purchase the warrant sooner rather than later, but in any event, they must prepay the corresponding loan first. Although most mezzanine lenders do not offer to sell the warrant before three years, a borrower with a good deal might negotiate this down to two years.

Deferred-Interest Balloons

Some debt-oriented mezzanine lenders employ a deferred-interest balloon as part of the loan. A deferred-interest balloon is a structure that stalls a stated amount of interest into the future, at which point it is due in full. This balloon payment may be in the borrowers’ best interest for two reasons.

1. If borrowers are tight on cash flow during the first few years of the loan, the deferral of a large part of the interest may enable them to achieve their business plan goals without a liquidity crunch.

2. The deferred interest balloon may be deductible on a current period basis for taxes, even though it actually will be paid in the future. This may be the case if the balloon is a legal contract that is an obligation of the borrower, and the company is on an accrual basis for tax reporting. For instance, if a $3 million deferred-interest balloon is due five years after the closing, the borrower may be able to write off $600,000 per year in interest deductions. Readers are encouraged to check with their tax professionals to confirm whether this deduction is possible for their situation.

PRICING QUESTIONS TO ASK A MEZZANINE INVESTOR

- What is the cash interest or “coupon” rate of the loan?

- What are the other pricing components?

- Is there an equity component to the price?

- What are the costs to exit the relationship and pay off the loan?

Default Interest Rates

Most lenders increase the interest rate during the period of covenant default. As stated, it is not unusual for the interest rate to increase by 5% to 6% until the default is cured. Borrowers should negotiate each covenant and determine whether the default interest rate should apply. For instance, certainly the default rate should apply for payment defaults. But should it apply if capital expenditures exceeded the plan by $20,000? It may be desirable to separate major and minor defaults, with the default rate applying only to the more serious infractions.

Performance Ratchets

Performance ratchets sometimes are structured into mezzanine financing, especially in an equity mezzanine deal. Such ratchets are a matter for discussion and agreement between the parties. In essence, performance ratchets encourage management to perform against defined targets. These targets usually are defined by reference to profits but additionally or alternatively can be related to the time of exit.

Performance ratchets are designed to give the management team an enhanced proportion of the shares if performance reaches agreed levels. A reverse ratchet reduces the management's proportion of the shares if performance falls below agreed levels. It is important to have a clear, shared understanding between the parties of what is being agreed and how it is to be measured. Because there are many variables and alternative methods of measuring and interpreting accounting concepts, contentious situations will arise unless very precise terms of agreement are laid down up front.

Other Items

A handful of other items are negotiated with mezzanine deals. A majority of investors prefer the investee to use a C corporation legal structure. Few mezzanine players prefer investing in pass-through entities, such as limited liability companies, because tax distributions disrupt the target's cash flow. Most mezzanine investors prefer to have cash reinvested in the company to enable growth, thereby making the company and the warrant more valuable. Also, stock pledged as collateral for a mezzanine loan by a company owner is open for discussion. Many mezzanine deals occur without any pledge. If an owner is forced to pledge stock, it should have limits, such as a limit on the amount pledged and the performance benchmarks that trigger a release of the pledge.

Comparison to Other Capital

Mezzanine capital fills the capital void between secured debt and equity capital. Compare various characteristics of mezzanine capital to other capital types. Exhibit 22.7 compares mezzanine capital to bank debt and equity.

EXHIBIT 22.7 Comparison of Mezzanine Capital to Bank Debt and Equity

Mezzanine capital is characterized by a fairly high coupon rate of interest, a defined term, and attributes that lead to a lack of management control. Quite often shareholders do not guarantee mezzanine debt, which is an advantage over bank debt. Equity mezzanine might be dilutive, but typically investors prefer to sell their warrant position back to the investee rather than exercising the warrant. Mezzanine return expectations fall between bank debt and equity. Companies probably should use bank debt when it is available but employ mezzanine capital rather than add equity.

TRIANGULATION

Capital availability directly affects the value of a firm. High-growth companies often suffer from lack of capital because banks prefer conservative growth scenarios. Further, owners often do not want to dilute their ownership positions, so private equity is viewed as less desirable. Mezzanine capital may be a good option for companies experiencing earnings’ growth rates of more than 20% per year.

Companies in need of mezzanine capital are viewed in either the collateral value or market value world. DMC providers consider the collateral position of the company, with an eye on market value. EMC investors are more concerned with open market values than they are with collateral values. With both types of investors, warrants are structured based on the market value of the company.

The real power of mezzanine financing is realized through the added leverage it provides to the borrower. For a typical company, every dollar of mezzanine capital can be leveraged, with up to three dollars of additional bank debt capacity. This is because banks normally view mezzanine capital as a form of quasi-equity, which expands the borrower's effective equity base. Thus, banks can lend more to the company without exceeding the borrower's existing debt-to-equity ratio. A corrugated box manufacturer recently used this added leverage to its advantage. By raising $5 million in equity mezzanine financing, its bank committed to an additional $10 million in low-cost financing. The blended cost of the total financing enabled the company to meet its business plan, which created substantial wealth for the shareholders.

If a company obtains mezzanine capital, it is forced to seek cheaper sources of capital to pay off the mezzanine at the end of its term. Most mezzanine investments are satisfied either through a change-of-control sale or a recapitalization of the company. A sale of the company is especially likely when the warrant position is too high to refinance. A recapitalization is likely when the company meets or exceeds its expectations. It is clear that obtaining mezzanine capital, like obtaining private equity, ultimately puts a company in play.

NOTES

1. John K. Paglia, Pepperdine Private Capital Markets Project Survey Report, April 2010, bschool.pepperdine.edu/privatecapital.

2. Ibid.

3. See the SBA Web site, www.sba.gov.

4. Ibid.

5. John K. Paglia, Pepperdine Private Capital Markets Project Survey Report.

6. Ibid.

7. Ibid.

8. Taken from: www.Archadvisors.com.