CHAPTER 19

Equipment Leasing

Most businesses in the United States lease equipment at some point. Many of these companies use leasing to finance the eventual purchase of the equipment. This chapter discusses the various types of leases, the advantages and disadvantages of leasing over purchasing, the lease process, the effective costs of leasing, and negotiating points.

An equipment lease is a legally binding and generally noncancellable document that details an agreement between two parties: The lessor is the party that owns the asset, and the lessee is the party that uses the asset. Lessees choose the asset they wish to use and the vendor(s) they want to supply it. They also negotiate the purchase price and performance requirements directly with the vendor of their choice. The lessor, on behalf of the lessee and at the lessee's instruction, purchases the specific asset from the specified vendor.

The lessee agrees to keep and use the asset for a specific time period defined as the lease term. During this period, the lessee must pay a predetermined periodic rental, usually monthly; pay any and all taxes or other equipment assessments; maintain the required insurance; and keep the asset in good working condition.

EXHIBIT 19.1 Capital Coordinates: Bank and Captive/Vendor Equipment Leasing

| Capital Access Point | Bank | Captive/Vendor |

| Definition | Banks are a major source of equipment leases. Because of the bank's cheap source of funds, they may offer the least expensive lease terms. | Many large manufacturers provide financing to their customers, often in the form of an equipment lease. |

| Expected rate of return | 5%–7% | 5%–7% |

| Authority | Banks | Vendors |

| Value world(s) | Collateral value | Collateral value |

| Transfer method(s) | Available to all transfer methods | Available to all transfer methods |

| Appropriate to use when . . . | The least expensive lease is sought and residual value of the equipment is fairly predictable. | A vendor subsidizes equipment sales with favorable lease terms. |

| Key points to consider | Finance leases become part of a borrower's capital structure, having the same balance sheet effect as a loan. | The lease versus purchase analysis should be performed to determine the cheapest method of financing. |

Companies are motivated to seek equipment leasing primarily because leases tend to be relatively easy to obtain. Just about every company can obtain an equipment lease. Lessors not only finance the equipment for the lessee, expecting to earn a fair return for providing this service, but also may commingle the financing and sale of the equipment, which often results in a good deal for the lessee.

Lessors are the authorities in equipment leasing: They make the rules. Lessors have the power to veto all transactions, which gives them authority over lessees. Five different equipment lessor types are discussed in this chapter. Exhibit 19.1 depicts the capital coordinates for bank and captive/vendor equipment leasing. The Pepperdine Private Capital Market Line is not shown because equipment leasing has not yet been surveyed.

TYPES OF LEASES

There are a number of different types of leases, and this chapter describes three general types. The first type is a true lease, defined as

A lease in which the lessor takes the risk of ownership, as determined by various Internal Revenue Service (IRS) pronouncements, and, as owner, is entitled to the benefits of ownership including tax benefits. This type of lease is sometimes called a tax lease.

Structuring a lease as a true lease is important because the lessor becomes the tax owner of the property, with all of the rights and privileges this confers. Improper structuring may cause the lease to be recognized as a conditional sale or secured loan. Instead of payments being recognized as rent, as is the case with a true lease, improper structuring would cause the lessee's payment be broken into imputed principal and interest, which does not offer tax advantages to the lessor.

To help taxpayers determine the type of lease, the IRS issued Revenue Ruling 55-540 in 1955, which defined what was not a true lease for tax purposes, commonly referred to as a lease intended as a security. This ruling holds that a transaction is not a true lease if any one or more of these conditions are present:

- Any portion of the periodic lease payment is applied to an equity position in the asset to be acquired by the lessee.

- The lessee automatically acquires title to the property upon payment of a specified amount of “rentals” he or she is required to make.

- The total amount, which a lessee is required to pay for a relatively short period of use, constitutes an inordinately large proportion of the total sum required to be paid to secure the transfer of the title.

- The agreed “rental” payments materially exceed the current fair rental value.

- The property may be acquired for a nominal purchase option in relation to the value of the property at the time the option may be exercised.

- Some portion of the periodic payment is specifically designated as interest or its equivalent.

Readers should consult their leasing professional and CPA to determine if a proposed lease is a true lease or not.

The second type of lease described here is a finance lease, probably the most common type of lease used worldwide, defined as:

A lease agreement that requires the lessee to remit payments of lease rentals, which total the cost of the asset plus the lessor's required profit. It is noncancellable and requires the lessee to pay all of the taxes and other assessments, provide insurance, and maintain the asset according to the manufacturer's guidelines. It provides that the lessee will acquire title to the asset at the conclusion of the lease term.

Like nearly every lease, the finance lease probably contains a hell-or-high-water clause that states the lessee's commitment to pay rent is unconditional during the term. In other words, the lessee must pay regardless of what may occur during the term.

The third type of lease mentioned here is the operating lease, which extends for a relatively small part of the useful life of the equipment. Unlike the finance lease, lessors expect lessees to return the equipment at the end of the lease term. In some cases, an operating lease can last a day or two, such as a short-term truck rental, or several years, such as a long-term truck rental. An operating lease is almost always a true lease and may have a hell-or-high-water provision.

A difficulty with lease terminology is that the perspective of the participants determines which terminology to use. There are three main participants involved in the leasing discussion, and they are focused on different aspects of the lease. These participants are the:

1. Leasing industry. This group is most concerned with earning an economic return on the lease. They may use terms such as a “full payout lease,” which means the total lease payments back to the lessor for the entire cost of the equipment including financing, overhead, and a reasonable rate of return, with little or no dependence on the residual value.

2. Tax people. This group, which consists of the people who are most concerned with the after-tax cost of the lease such as the IRS and tax CPAs, tries to ascertain whether the lease is a true lease or finance lease. The tax ramifications are extreme, depending on the type of lease that this group mainly focuses on.

3. Accountants. Accountants focus on the accounting treatment of the lease. Once again, different terminology is used to describe their perspective, such as a capital lease and an operating lease (different from the type described earlier, of course). A capital lease (accounting perspective) is the same as a finance lease (tax perspective). An operating lease (accounting) is the same as a true lease (tax).

Since the lease ultimately affects both the lessor's and the lessee's financial statements, the accounting treatment deserves extra mention here. Accountants typically refer to a finance lease as a capital lease. The accounting definition of a capital lease is:

A lease that meets at least one of the criteria outlined in paragraph seven of FASB [Financial Accounting Standards Board] 13, the standard for accounting and reporting of leases and, therefore, must be treated essentially as a loan for book accounting purposes. The four criteria are

1. Title passes automatically by the end of the lease term.

2. Lease contains a bargain purchase option (i.e., less than the fair market value).

3. Lease term is greater than 75% of the estimated economic life of the equipment.

4. The present value of the lease payments is equal to or greater than 90% of the equipment's fair market value.1

A capital lease is used by the lessee both to borrow funds and to acquire an asset to be depreciated. Thus, the equipment is recorded on the lessee's balance sheet as an asset and the lease as a corresponding liability. Periodic lessee expenses consist of interest on the debt and depreciation of the asset.

Accountants also view operating leases in specific terms. Operating leases, from a financial reporting perspective, have the characteristics of a true rental agreement and must meet certain criteria established by FASB. These criteria are:

- Title to the asset may not automatically transfer to the lessee at any time during the lease term or immediately after the lease term.

- There is no provision for a bargain purchase option.

- The lease is noncancellable for its term, and that term is less than 75% of the economic life of the asset.

- The present value of lease payments is less than 90% of the equipment's fair market value.

The lessee accounts for an operating lease without showing an asset or a liability on the balance sheet. The lessee accounts for periodic payments as operating expenses of the period on the profit and loss statement. Payments due in the periods following the preparation of the financial statement must be footnoted in the financial report.

A subtype of the operating lease is the sale-leaseback. The sale-leaseback occurs when an asset that is owned by the lessee is sold to the lessor and then leased back to the lessee. This can be an effective way for a lessee to raise cash for its business or to effect a change in asset utilization strategy. This type of lease is chosen as part of the sale-leaseback negotiations. For example, if PrivateCo sells $2 million of used equipment to LeaseCo, which then turns around and leases the equipment back to PrivateCo, it is necessary to negotiate what type of lease is involved. Most sale-leasebacks are structured as operating leases because the equipment is fairly old by the end of the lease.

LEASE RATE FACTORS

The lease factor is a shorthand mathematical expression that describes the lease payment as a decimal or fraction of the equipment acquisition cost. In other words, the lease factor is the fraction of the equipment cost each month that is paid to lease the equipment. For example, in a 36-month lease, a lease factor of .035 means that the lessee will pay 3.5% of the equipment cost per month. For equipment costing $100,000, the monthly payment would be $3,500. When added together and measured against the equipment's cost, it is possible to calculate the lease rate, or the effective interest rate implicit in the payments.

LEASE FACTORS

36-Month Lease

| Monthly Factor | Noncompounded Equivalent Financing Rate | APR |

| .03 | 8% | 5.1% |

| .035 | 26% | 15.7% |

| .04 | 44% | 25.5% |

Lease rate factors simplify calculating the cost of leasing. Using the example of 3.5% of equipment cost per month for 36 months, we get 126% in all. This 126% consists of two components: 100% represents the cost of the equipment, and 26% is the lease finance charge for the three-year period. Lease factors are stated in noncompounded terms; that is, the 26% finance charge in the example is spread monthly over three years rather than considered as a present value.

Lease rates are negotiated between the parties and are affected by many considerations. Some of these factors are:

- The cost of the leased asset

- The financial strength of the lessee, including term debt requirements and available cash flow

- The credit profile of the lessee, including historical reduction of other term debt

- The forecasted value of the leased asset at lease end or if it is sold in a distressed situation

- The lease term

- The lessor's cost and availability of funds

- Charges and documentation fees

Leasing Process

The generic lease process consists of eight steps.

1. The lessee selects the equipment and the vendor or supplier, and then the lessee negotiates the best price with that supplier.

2. The lessee submits an application to a leasing company and provides the credit and other information required by the leasing company.

3. The leasing company conducts a credit investigation and evaluation.

4. If the lessee's credit is approved, the leasing company conveys, in writing, all of the terms and conditions of the lease to the lessee.

5. Once the terms and conditions are agreed, the supplier of the equipment is contacted and asked for a pro forma invoice, which details the exact equipment configuration and the exact cost.

6. Once the leasing company receives the executed documents and a check from the lessee to cover any up-front costs, it will issue a purchase order to the supplier.

7. The lessee signs all documents except the acceptance notice. This is not signed until the equipment is installed to the lessee's satisfaction.

8. Once the installation is complete and insurance on the equipment is in force, the lessor pays for the equipment and the lease starts.

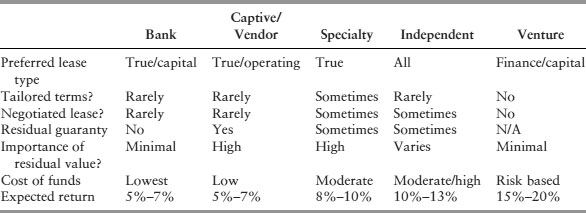

LESSOR TYPES

There are a number of lessor types in the market. Each has a unique business model that may or may not fit the needs of a particular lessee. The next sections summarize each lessor type, then compare them relative to the major leasing characteristics.

Banks

Banks are a major source of equipment leases. Because of their relatively cheap cost of funds, banks may offer the least expensive lease. Banks require a lessee with strong credit and usually already have a lending or other relationship with the borrower. Banks are at a disadvantage when it comes to residual value of the equipment, since they are less active players in the equipment market. For this reason, banks tend not to be competitive in situations where residual value is difficult to predict.

Captive and Vendors

Many large manufacturing companies provide financing to their customers, sometimes in the form of an equipment lease. Captive leasing companies tend to be divisions or subsidiaries of these manufacturers, and are dedicated to offering leasing primarily for the manufacturer's products. Since captive lessors generally are part of a large company, their cost of funds tends to be low, making them highly competitive.

With vendor leasing, the manufacturer does not use a subsidiary leasing company; rather, the manufacturer offers the lease to customers directly. Many vendors earn higher lease rates in this scenario, with the hope of bundling the leases and selling them to other lessors.

It should be noted that both captive and vendor lessors exist for the purpose of supporting the manufacturers and may, from time to time, offer very aggressive lease plans as part of a sales promotion driven by the manufacturer.

Specialty Equipment Lessors

Some lessors specialize in an industry or in certain types of equipment. These lessors have an advantage in situations where the underlying equipment has an uncertain secondary market (i.e., where specialized knowledge about equipment obsolescence can create a lessor advantage). Specialized equipment lessors may be more expensive than other lessor types at the outset, because of the higher cost of funds and the lack of reliance on residual value. However, for specialized equipment, this lessor may be cheaper over time than the other lessors. This is because this lessor works with the lessee over time and absorbs some of the obsolescence risk of the equipment. Exhibit 19.2 provides a snapshot of specialty and venture leasing.

EXHIBIT 19.2 Capital Coordinates: Specialty and Venture Equipment Leasing

| Capital Access Point | Specialty | Venture |

| Definition | These lessors specialize in an industry or with certain types of equipment. | Venture leasing provides equipment to start-up and early-stage companies. |

| Expected rate of return | 8%–10% | 15%–20% |

| Authority | Specialized lessors | Venture lessors |

| Value world(s) | Collateral value | World of early equity value; collateral value |

| Transfer method(s) | Available to all transfer methods | Available to all transfer methods |

| Appropriate to use when . . . | Residual value is not predictable, thereby making this lessor cost competitive. | Traditional leasing methods are unavailable. |

| Key points to consider | This lessor generally absorbs some of the obsolescence risk of the equipment, which may benefit the lessee in certain circumstances. | Warrant costs add to the required rate of return listed above and must be negotiated separately from the standard lease terms. |

Independent Lessors

These general leasing companies may be affiliated with a larger finance company. Independent lessors offer leases on most types of equipment and may find equipment niches where banks cannot participate. These lessors are more likely to offer creative solutions than the competition. Independent lessors usually have a higher cost of funds than the competition.

QUESTIONS TO ASK BEFORE SIGNING A LEASE

Here is a list of ten questions that should be asked prior to signing a lease.

Before the Lease

1. How am I planning to use this equipment in my business, and how long will I need it?

2. Does the leasing representative understand my business and how this transaction helps me do business?

During the Lease Period

3. What is the total lease payment, and are there any other costs that I could incur before the lease ends?

4. What happens if I want to change this lease or end the lease early?

5. How am I responsible if the equipment is damaged or destroyed?

6. What are my obligations for the equipment (such as insurance, taxes, and maintenance) during the lease?

7. Can I upgrade the equipment or add equipment under the lease?

After the Lease Ends

8. What are my options at the end of the lease?

9. What procedures must I follow if I choose to return the equipment?

10. Are there any extra costs at the end of the lease?

Venture Lessors

Venture leasing provides general-purpose equipment, such as computers, telecommunication systems, and office equipment, to start-up and early-stage companies. In exchange for the lease financing, the venture lessor receives monthly equipment payments, the equipment's residual value, and, in some cases, equity in the company. Even without accounting for the warrant cost, this lessor type probably offers the highest-cost lease to lessees.

EXHIBIT 19.3 Comparison of Lessor Types

Exhibit 19.3 compares lessor types across a number of characteristics. The exhibit raises four issues.

1. Because leasing is so varied as to the providers and deal structures, it is difficult to draw definitive conclusions by lessor types. Thus, the exhibit needs to be viewed in directionally accurate terms.

2. It is important for prospective lessees to understand the underlying different approaches used by the various lessor types. For instance, some lessors have a preferred lease type, some negotiate lease terms, and some rely heavily on residual value for their return.

3. The lessors have different costs of funds. Banks generally have the lowest cost of funds, whereas venture lessors may have the highest.

4. Expected returns are quite varied in equipment leasing. Deals in this market are not as standardized as many of the other capital access points. For this reason, expected return is shown as ranges, with only venture leasing (described in the next section) shown as an exact return.

Expected Returns

Equipment leasing is too varied relative to pricing and terms to employ the credit box depiction that this book uses to describe most of the other capital access points. Each lease should be analyzed separately to determine the expected returns. Little research has been done to determine lease returns by lessor type. At least one study was done to show expected lease returns to the lessor.2 This study involved venture leasing, which provides general-purpose equipment, such as computers, telecommunication systems, and office equipment, to start-up and early-stage companies. In exchange for the lease financing, the venture lessor receives monthly equipment payments, the equipment's residual value, and equity warrants in the company. Exhibit 19.4 shows pretax yields assuming a residual value of 15%.

EXHIBIT 19.4 Venture Leasing Study

| Pretax Yields on 44 Lease Agreements | |

| Assumes residual value of 15% | |

| Yield | |

| Maximum | 37.2% |

| Minimum | 11.1% |

| Average | 17.7% |

| Median | 16.5% |

A couple of items are noteworthy regarding this study. The median yield of 16.5% might be higher than nonventure leasing, since lessors might require an extra return for the risk of leasing to early-stage companies. Also, the median yield for this study when assuming a zero residual value is 9.4%. Finally, the warrants associated with the leases were not considered in the yield pricing.

EXHIBIT 19.5 Comparison of Leasing and Borrowing (Purchasing)

| Item | Leasing | Borrowing |

| Effective Cost | May be lowest cost when all tax savings are considered. | Normally the lowest pretax effective cost. |

| Ongoing Fees | May have service fees. | No service fees unless loan origination or compensating balances are required. |

| Ownership of Asset | No ownership with operating lease; ownership eventually with capital lease. Also, leasing may better match the duration need of the lessee. | Ownership from the outset. This may or may not match the lessee's duration need. |

| Down Payment | Some leases provide 100% financing | Normally requires a 20%–25% down payment |

| Borrowing Capacity | Operating leases do not affect a company's capacity since they are off the balance sheet. Also, the lessee can avoid loan covenant restrictions that may exist with a loan. | Loans reduce borrowing capacity. Loan covenants must be negotiated and complied with. |

| Hedge Against Inflation | By delaying the outlay of funds until the lease payment, the lessee benefits from increases in equipment costs. | Ownership absorbs devaluation and inflation risk. |

| Residual Value | Accrues to the lessor with a true lease. | Accrues to the purchaser with a finance lease. |

| Tax Benefits | For true leases, rent expense is deducted as payments are made. | Depreciation and interest expense reduce taxable income. |

COMPARISON OF LEASING AND PURCHASING

There are a number of advantages when comparing leasing with purchasing equipment. Exhibit 19.5 shows the major differences.

Cost of Lease versus Purchase

The costs of the lease versus purchase can be determined through discounted cash flow analysis. This analysis compares the cost of each alternative by considering the timing of the payments, tax benefits, the interest rate on a loan, the lease rate, and other financial arrangements. Of course, the ultimate cost is dependent on the validity of assumptions about future values and changes in the value of money.

To perform the analysis, certain assumptions about the economic life of the equipment, residual value, and depreciation need to be made. To evaluate a lease, the net cash outlay in each year of the lease term is determined. These amounts are derived by subtracting the tax savings from the lease payment. This calculation yields the net cash outlay for each year of the lease. Each year's net cash outlay is discounted to take into account the time value of money. This discounting derives the present value of each of the amounts. The sum of the discounted cash flows is called the net present value of the cost of leasing. This figure is compared with the final sum of the discounted cash flows for the loan and purchase alternative.

EXHIBIT 19.6 Purchase versus Lease Terms Estimates

Evaluation of the borrow/buy option is a little more complicated because of the tax benefits that go with ownership through loan interest deductions and a depreciation method called Modified Accelerated Cost Recovery System (MACRS). The interest portion of each loan payment is found by multiplying the loan interest rate by the outstanding loan balance for the preceding period.

As noted earlier, a claim on the residual value is one of the advantages of ownership. It is discounted at a higher rate than the cash outlays. In the next example, the firm's assumed average cost of capital is 15%. This rate is used because the residual value is not known with the same certainty as are the loan payment, depreciation, and interest payments.

The major difference in cost, of course, comes from the residual value. If that value is ignored, the alternatives are very close in their net present value of costs. Naturally, it is possible that residual costs for each asset could be very high or be next to nothing. Residual value assumptions need to be made carefully. Outside sources that offer residual valuations can assist in the determination.

The next sections analyze the differences between purchasing and signing an operating lease. Assuming that PrivateCo needs a machining center, Exhibit 19.6 contains estimates for this equipment.

Purchase Option

Several items listed in the chart in Exhibit 19.6 require further explanation. First, the interest rate represents the incremental borrowing rate of the firm. The net cash flows are discounted by this rate. The discount rate, however, represents the weighted average cost of capital of the firm. The residual value is discounted by the discount rate to reflect the additional risk of estimating this value five years before realization.

Second, for most business property placed in service after 1986, the owner either claims the equipment expensing deduction for the full cost of the item (for small-ticket items) or uses MACRS. This method categorizes all business assets into classes and specifies the time period over which the assets can be written off. The equipment used in this example qualifies under “7-year property” and therefore can be written off over a seven-year period using these percentages: 14.29%, 24.49%, 17.49%, 12.49%, 8.93%, 8.92%, 8.93%, and 4.46% for the last year (called the “half-year convention”).

Finally, this example does not incorporate maintenance costs into the calculations. Although the lessee is normally responsible for maintaining the equipment, this is a negotiated item between the parties.

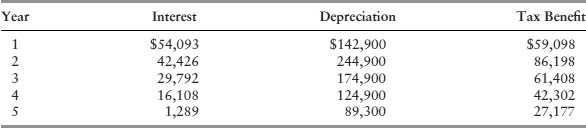

To determine the net present value of the purchasing cash flows, the calculations in Exhibit 19.7 are necessary. The cost of purchasing in this example, on a present value basis, is $(683,802). This present value number represents the net cost, in today's dollars, of financing the purchase of the equipment.

The interest was calculated based on end-of-period principal and interest payments. Beginning balance: $800,000. Interest rate: 8%. Depreciation was calculated using the MACRS tables with 7-year property. The tax benefit is calculated by adding the interest and depreciation expenses and multiplying by the assumed 30% tax rate.

EXHIBIT 19.7 Cost of Purchasing

1. The Tax Benefits listed in the cost of purchasing table are calculated as follows:

EXHIBIT 19.8 Cost of an Operating Lease

1. The tax benefits listed in the cost of an operating lease table are calculated as follows:

| Year | Lease Payment | Tax Benefit |

| 1 | $252,000 | $75,600 |

| 2 | $252,000 | $75,600 |

| 3 | $252,000 | $75,600 |

| 4 | $252,000 | $75,600 |

| 5 | $252,000 | $75,600 |

Lease

The calculation regarding the present value of an operating lease is much simpler than the cost of purchasing presentation. With an operating lease, the lessee does not have benefit of claiming depreciation or interest expense. However, the lease expense is tax-deductible. Exhibit 19.8 shows the present value calculations for this example.

The lease payments are provided in the example. The tax benefit is calculated by adding the lease payment and multiplying by the assumed 30% tax rate.

The present value of the operating lease cash flows is $(704,313), which is slightly more expensive than the cost of purchasing shown in the previous example. It should be noted, however, that residual value is extremely important to the cost of purchasing calculations. For example, if PrivateCo believes it can sell the machining center in year 6 for $250,000, instead of the $160,000 used in the example, the present value of purchasing becomes $(653,857), which is considerably less than the present value cost of purchasing example.3

Several of the variables are sensitive enough in this purchase versus lease analysis so that slight changes in an estimate yield a different result. Aside from residual value, changes in the required down payment, lease payments, tax rates, and discount rate all can change the ultimate decision. Although this sort of analysis is useful, a lease/buy decision should not be made solely on cost analysis figures. The advantages and disadvantages, while tough to quantify, may outweigh differences in cost, especially if costs are reasonably close.

Aside from the stated costs, there can be hidden costs in a lease, such as:

- Document fees. These fees are administrative costs due upon signing the lease and can amount to hundreds of dollars, depending on the complexity of the lease contract and size of the transaction.

- Broker fees. Some leasing companies are not full-service lessors; rather, they are leasing brokers that charge a fee by marking up the lease rate factor.

- UCC-1 fees. These are fees required by the secretary of the state where the equipment is being leased. A UCC-1 fee is a one-time fee due at signing.

- Title fees. Some lessors charge a fee to obtain clean title to the equipment in the event the option to purchase the equipment is exercised at the end of the lease.

- Taxes. In most states, there is a tax on goods purchased. Some states tax at 5% to 6% or more. The tax is factored into lease payments, so this cost should be considered, because it could increase the monthly lease payments, depending on the total cost of the equipment and the state of purchase. Also, if the lease is structured as an installment sale, tax may be due up front or as part of the amount to be financed.

NEGOTIATING POINTS

Leases contain many variables that are negotiated. Therefore, there are many negotiating points to consider. Some of the more important points are described in the next sections.

Start Period

Most equipment leases start with acceptance or commencement. Lessees should not begin paying for an equipment lease until the equipment is operating successfully. This is all the more important since most equipment leases include a nonnegotiable hell-or-high-water clause that takes effect regardless of whether equipment works.4

ABC Lease

Some lessors try to lock up lessees forever whereby the lessee can escape only by paying an inordinate fee. With an ABC lease, the lessee can exercise only one of three options: (1) buy the equipment at a mutually acceptable price, (2) extend the lease at a mutually acceptable price, or (3) return the equipment to the lessor only if a new deal is negotiated with the lessor at a mutually acceptable price.5

Changes

Lessees need to know whether they can move equipment to a new location without written consent for which they must pay. Computers and other technology products need upgrades more than every three to five years. Lessees should negotiate strong lease language if they want the lessor to pay for upgrades, which adds to the cost of the lease.

Termination

Early termination probably is the most common equipment leasing problem because the lessee's needs may change during the lease term, but the termination cost may be high. Often the termination price is the total of all payments remaining. Other approaches involve preserving the lessor's originally anticipated yield. Provisions for early termination, early buyout, subleasing, and assignment can protect lessees. They are not, however, part of the written lease unless the lessee puts them there.

Along a similar line, most lessors require some type of notification period near the end of the lease term. If the leasing company is going to remarket the equipment successfully, it probably needs to know 60 to 90 days in advance of its return. The lease may even mandate an automatic extension of the lease term if adequate notice is not given. For example, it may mandate an additional 90 days if the lessee waits until the very end of the lease to notify the lessor of its intent to return leased equipment. If a lease requires notification or extension clauses substantially longer than 90 days, the leasing company may be trying to take advantage of the lessee.

If a lessee chooses to return the equipment, it is fairly standard practice to require the lessee to crate and ship it back to the lessor at the lessee's expense. Making the return provisions too difficult is a way to increase the likelihood that the lessee will elect to purchase the equipment at lease end rather than return it. Such provisions as the way the equipment must be crated, the return of manuals and cables, how it must be shipped and to what location(s) can all impact that decision.6

Purchase Rights

Most leases give the lessee an end-of-lease purchase or release option at the then-current fair market value. Prudence requires that fair market value (FMV) is defined up front. Some of the largest leasing companies use FMV as the purchase standard of value, but they determine what that fair market value is! The lessee has a right to buy the equipment but only at the number the lessor stipulates. It is almost always better to have FMV determined through independent appraisals.

Maintenance Responsibility

Lessees should clarify which service and maintenance programs are included in the lease. If lessees are responsible for service and maintenance, they should make sure the expectation is reasonable.

Master Lease versus Schedules

Another point of consideration is to review both the master lease and specific equipment schedules.7 When reviewing copies of documents, the master lease usually gets most of the scrutiny, as it governs virtually all of the standard terms of a lease. The schedules usually define specific equipment, payments, lease length, and so on. Since terms and conditions of the schedule often take precedence over the master lease, lessees need to review them both.

TRIANGULATION

Equipment leasing is the most readily available type of capital for businesses. Since access to capital affects the value of a business, equipment leasing probably does more to increase the value of private companies than any other capital type. As the private capital access line demonstrates, equipment lessors expect returns somewhat in the middle of the line. In other words, equipment leasing is not the cheapest or the most expensive form of capital.

Lessees consciously make a trade-off between time and money with regard to equipment leasing. Many lessees spend a fair amount of time and effort to finance the required equipment through their normal banking relationship, probably by purchasing the equipment up front. Other lessees choose to pay extra for a lease because it is easier to accomplish than dealing with the bank, and they find that that it is just not that much more expensive than a bank loan. As one owner of a wood kilning and planing operation explained, “For an extra point or two, I get the leased equipment delivered to me within days. It might take weeks or months to get the same response from my banker.”

The leasing market is bifurcated by lessor return expectations. Companies that lease with banks or captive/vendors, typically the lessors with the lowest return expectations, usually have the choice as to whether to purchase or lease. Lessees that deal with specialty or venture lessors, however, may not have the luxury of moving down the access line. Within the leasing industry, companies shop for the least expensive credit available.

Equipment leases are also the most tailored form of capital. With the variety of lessors in the market, the needs of the borrower can almost always be met. Since lessors maintain a security interest in the equipment, they can regain possession of the equipment in case of payment or other default. Lessors view lessees in the world of collateral value because the residual value of equipment tends to have greater value when in place and operating.

Equipment leasing often eases transfer of a business because operating leases tend to slide through to the new owner. Even finance leases typically can be reworked to suit to the next owner. Some buyers employ an equipment sale-leaseback as a source for a cash down payment.

NOTES

1. FASB 13, paragraph 7(a)

2. Robert T. Kleiman, “The Characteristics of Venture Lease Financing,” Journal of Equipment Lease Financing (Spring 2001).

3. The $653,857 present value based on a $250,000 residual value is calculated as:

Residual value = $250,000

Gain over book value = $79,559

Tax on gain = $23,868 (taxed at 30%, which might be an overstatement)

Net cash flow of residual value = $226,132 ($250,000 residual value – $23,868 gain)

Present value of $226,132 = $(97,763), which is shown as a negative because it improves the cash flow

Present value of net cash flows = $653,857 ($200,000 + 125,835 + 93,280 + 106,050 + 112,238 + 114,217 + (97,763)

4. Michael J. Fleming, A Guide to Equipment Leasing, February 17, 2000, www.bpubs.com.

5. The first several points were taken from Martin Paskind, “Act with Care When You Lease Equipment,” SOHO America, 2000, www.soho.org.

6. Robb Aldridge, “Gotcha! Be Wary of Leasing Documentation,” AS400 Technology Showcase (August 1998).

7. Ibid., p. 2.