7.3 FPGA MARKET AND START-UP COMPANIES

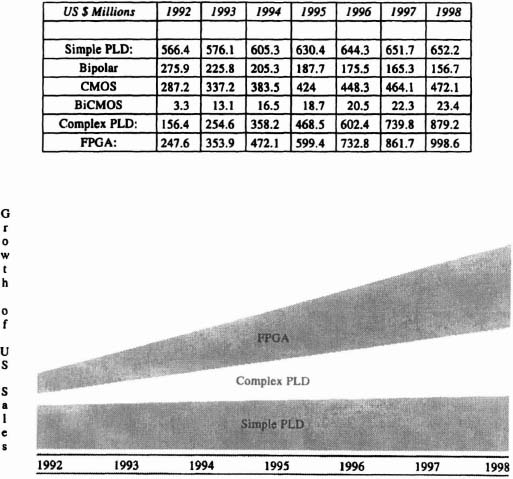

The FPGA market has progressed through several evolutions, beginning with logic replacement and rapid prototyping to an emerging technology allowing dynamic reconfiguration. The market has consistently grown due the advantages of the device and the continuing development of new applications. In 1990 worldwide sales of FPGAs were $108 million, expanding to $187 million in 1991 [Willett92]. By 1992 U.S. sales of FPGAs reached $247.6 million, representing a 56.7% growth rate for the FPGA within the U.S. programmable logic market. According to In-Stat, Inc., the U.S. FPGA market grew 42.9% from 1992 to 1993. In-Stat, Inc., has projected the U.S. FPGA market will grow from $353.9 million in 1993 to $998.6 million by 1998; a compounded annual growth rate of 23.1% [Rohl94] (see Figures 7–1 and 7–2).

The FPGA enabled companies in telecommunications, cable, medical device development, among others, to move products to market more efficiently. There are distinct phases of application development, as designers and managers see the potential of a new approach, ranging from initial, hesitant steps to major paradigm shifts, that is, exploiting the new device for its unique capabilities.

Figure 7–1. Programmable logic market, 5-year forecast as of April 1994. Derived from data provided by In-Stat, Inc. †

7.3.1 Rapid Prototyping

Due to the user-programmable feature of the FPGA, new designs could be created more efficiently and quickly. Testing and modification of new designs became possible with lower nonrecurring engineering (NRE) costs.

7.3.2 Logic Replacement

Printed-circuit-board design, fabrication, and component insertion costs can be reduced, since much logic can be compressed into a single FPGA package. In addition, this improves the reliability and often, but not always, the speed of a digital system. Designs may exploit FPGA reconfiguration, for example, in an instrument that changes major functions or applicable standards, for example, European (PAL, or SECAM) TV measurements compared with U.S. (NTSC) TV. System upgrades, whether due to design error or improved performance, can be carried out particularly easily compared with older implementations that require printed-circuit or component changes.

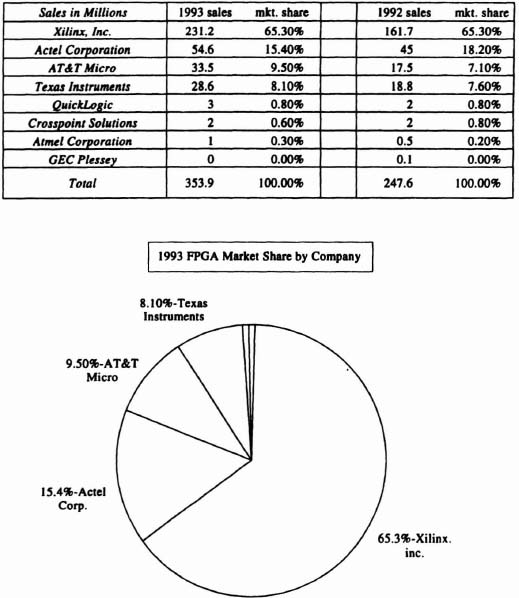

Figure 7–2. 1993 FPGA market share by company. Derived from data provided by In-Stat, Inc. as of April 1994.

7.3.3 Arrays of FPGA Chips

The term custom computing refers to the creation of special-purpose, often highly parallel, computer systems for specialized tasks, such as genetic string distance evaluation and cryptography, the subject of Chapter 6. The performance must be orders of magnitude greater than conventional computers (including parallel ones) to make this worthwhile. More importantly, the fraction of the task must be substantial. For example, if the FPGA array reduces, say, 50% of the task to virtually zero time, the overall application is only accelerated by a factor of 2, and the user may well prefer to wait for the next “winner” of the reduced instruction set computer (RISC) microprocessor race!

7.3.4 Dynamic Reconfiguration

Only RAM-based FPGAs, like the ones discussed in this book, can be changed quickly enough (< 10 ms) for in-system reconfiguration. Erasable-programmable-read-only-memory-based (EPROM) FPGAs must be removed to an external ultraviolet erasure device and a device programmer. But most of the present-day FPGAs are configured in a serial fashion, that is, by sending a string of bits via a single input pin. Thus a single change requires shutting-down the application and totally reloading the on-chip RAM. A few FPGAs, notably Algotronix, Atmel (Concurrent Logic), and Pilkington allow the configuration memory to be addressed at run-time, and so an individual bit may be changed. This is a highly novel, even hazardous type of computing, changing the logic while the data remains in place. There are few convincing applications yet, but this feature represents a major paradigm shift that will probably be exploited in the next decade.

Start-up FPGA companies opted to devote financial and human resources to research and development, and consequently produced novel architectures such as fine-grain fuse-programmable transistor arrays (Crosspoint Solutions), a relatively fine-grain SRAM-based architecture (Concurrent Logic), and coarse-grain antifuse architecture (QuickLogic). Start-up companies also relied upon third-party providers of “front-end” CAD software, for such tasks as schematic entry and simulation, while providing their own “back-end” software for the architecturally dependent aspects, such as technology mapping, placement, routing, and configuration. Even the back-end will not remain a monopoly of the FPGA vendor, since electronic CAD companies are developing rival software capable of mapping to a variety of architectures (e.g., Mine, NeoCAD, etc.). This trend will be furthered by electronic system designers who prefer to work with alternative FPGAs, rather than be locked into a particular vendor. The “front-end” software is also being extended toward higher levels of system specification, for example, VHDL, a standard language for specifying digital systems. VHDL has a particular merit of reusability, for building blocks of earlier systems expressed in VHDL can be incorporated into new systems without concern for FPGA architectural details.

7.3.5 Do You Need a Fabrication Facility?

The semiconductor industry is in a state of rapid change, both organizationally as well as technically. It has evolved from a few vertically integrated companies with high-volume in-house wafer fabrication, to a more diverse industry with silicon foundries serving low- to medium-volume demand, as well as bulk fabricators of memory and microprocessor products. Start-up FPGA companies have benefited from worldwide availability of state-of-the-art fabrication facilities.

In reviewing the state of the U.S. computer industry, Andrew Rappaport and Shmuel Halevi [Rappaport91] point to the advantage of defining and controlling a computing environment, as distinct from delivering raw computing horsepower. They contrast the success of Microsoft with its Windows operating system, which provides a distinct computing paradigm for vast numbers of computer users and software developers, with the proliferation of marginally differentiated producers of personal computers and workstations. They suggest that the primary, strategic goal of U.S. computer companies should be “to create persistent value in computing,” rather than to build the hardware on which computer applications run. Are there parallels here for the programmable semiconductor industry? Rappaport and Halevi point out that semiconductor value is now largely a function of design specialization rather than processing, and the overabundance of advanced processing facilities is becoming more pronounced.

“Commodity” semiconductors are high-volume components, which are largely interchangeable, and for which competitive advantage is based on price and performance (e.g., memory, simple microprocessors, and controllers.) Prices are often driven down by aggressive worldwide competition. In contrast, highly differentiated components such as FPGAs can be produced in lower volumes with higher profit margins due to their distinctive purpose. Applying FPGAs in products allows design-oriented-system companies to concentrate on delivering and controlling value. The utilization of flexible, programmable integrated circuits and superior design tools will enable competitive electronics companies to add value to their product stream via continuous improvements. To quote from [Rappaport91], “Maximize the sophistication of the value you deliver; minimize the sophistication of the technology you consume.”