STEVEN V. MANN, PhD

Professor of Finance, Moore School of Management, University of South Carolina

FRANK J. FABOZZI, PhD, CFA, CPA

Professor in the Practice of Finance, Yale School of Management

Abstract: The money market is the market for short-term debt instruments. Short-term debt is traditionally defined as having original maturities of one year or less. Some of these instruments are interest bearing while others are discount instruments. Moreover, many of these securities calculate interest based on a 360-day year while others use a 365-day year. There are some essential money market calculations including day count conventions and basic formulas of price/yield one needs to know to understand how the money market works.

Keywords: day count convention, day count basis, actual/actual, actual/360, 30/360, yield on a bank discount basis, CD equivalent yield, bond-equivalent yield, effective annual yield

The purpose of this chapter is to introduce some of the fundamental calculations used every day in the money market. First, we will introduce day count conventions used in markets around the world. In addition, we will discuss the basic formulas for price/yield for both discount and interest-bearing securities.

To those unfamiliar with the workings of financial markets, it may come as a shock that there is no widespread agreement as to how many days there are in a year. The procedures used for calculating the number of days between two dates (e.g., the number of days between the settlement date and the maturity date) are called day count conventions. Day count conventions vary across different types of securities and across countries. In this section, we will introduce the day count conventions relevant to the money markets.

The day count basis specifies the convention used to determine the number of days in a month and a year. According to the Securities Industry Association Standard Securities Calculation Methods book, Volume 2, the notation used to identify the day count basis

(Number of days in a month)/(Number of days in a year)

Although there are numerous day count conventions used in the fixed income markets around the world, there are three basic types. All day count conventions used worldwide are variations of these three types. The first type specifies that each month has the actual number of calendar days in that month and each year has the actual number of calendar days in that year or in a coupon period (e.g., actual/actual). The second type specifies that each month has the actual number of calendar days in that month but restricts the number of days in each year to a certain number of days regardless of the actual number of days in that year (e.g., actual/360). Finally, the third types restricts both the number of days in a month and in a year to a certain number of days regardless of the actual number of days in that month/year (e.g., 30/360). Below we will define and illustrate the three types of day count conventions.

Treasury notes, bonds, and separate trading of registered interest and principal of securities (STRIPS) use an actual/ actual (in period) day count convention. When calculating the number of days between two dates, the Actual/ Actual day count convention uses the actual number of calendar days as the name implies. Let's illustrate the actual/actual day count convention with a 4.75% coupon, 30-year U.S. Treasury bond with a maturity date of February 15, 2037. Interest starts accruing on February 15, 2007 (the issuance date) and the first coupon date is August 15,2007. Suppose this bond is traded with a settlement date of June 4, 2007. How many days are there between February 15, 2007, and June 4, 2007, using the actual/actual day count convention?

To answer this question, we simply count the actual number of days between these two dates or 109 actual days between February 15, 2007, and June 4, 2007. In the same manner, we can also determine the actual number of calendars days in the full coupon period. A full six-month coupon period can only have 181, 182, 183, or 184 calendar days. For example, the actual number of days between February 15, 2007, and August 15, 2007, is 181 days.

Actual/360 is the second type of day count convention. Specifically, Actual/360 specifies that each month has the same number of days as indicated by the calendar. However, each year is assumed to have 360 days regardless of the actual number of days in a year. Actual/360 is the day count convention used in U.S. money markets and most money markets around the world. Let's illustrate the actual/360 day count with a 26-week U.S. Treasury bill that matures on November 29,2007. Suppose this Treasury bill is purchased with a settlement date on June 4, 2007 at a price of 97.640. How many days does this bill have until maturity using the actual/360 day count convention? The answer is 178 days.

When computing the number of days between two dates, Actual/360 and actual/actual will give the same answer. What, then, is the importance of the 360-day year in the actual/360 day count? The difference is apparent when we want to compare, say, the yield on 26-week Treasury bill with a coupon Treasury that has six months remaining to maturity. U.S. Treasury bills, like many money market instruments, are discount instruments. As such, their yields are quoted on a bank discount basis which determine the bill's price. The quoted yield on a bank discount basis for a Treasury bill is not directly comparable to the yield on a coupon Treasury using an actual/actual day count for two reasons. First, the Treasury bill's yield is based on a face-value investment rather than on the price. Second, the Treasury bill yield is an-nualized according to a 360-day year while a coupon Treasury's yield is annualized using the actual number of days in a calendar year (365 or 366). These factors make it difficult to compare Treasury bill yields with yields on Treasury notes and bonds. We demonstrate how these yields can be adjusted to make them comparable shortly.

Another variant of this second day count type is the actual/365. Actual/365 specifies that each month has the same number of days as indicated by the calendar and each year is assumed to have 365 days regardless of the actual number of days in a year. Actual/365 does not consider the extra day in a leap year. This day count convention is used in the UK money markets.

The 30/360 day count is the most prominent example of the third type of day count convention which restricts both the number of days in a month and in a year to a certain number of days regardless of the actual number of days in that month/year. With the 30/360 day count all months are assumed to have 30 days and all years are assumed to have 360 days. The number of days between two dates using a 30/360 day will usually differ from the actual number of days between two dates.

To determine the number of days between two dates, we will adopt the following notation:

| Yl = year of the earlier date |

| Ml = month of the earlier date |

| Dl = day of the earlier date |

| Y2 = year of the later date |

| M2 = month of the later date |

| D2 = day of the later date |

Since the 30/360 day count assumes that all months have 30 days, some adjustments must be made for months having 31 days and February which has 28 days (29 days in a leap year). The following adjustments accomplish this task.

If the bond follows the end-of-month rule and D2 is the last day of February (the 28th in a non-leap year and the 29th in a leap year) and Dl is the last day of February, change D2 to 30.

If the bond follows the end-of-month rule and Dl is the last day of February, change Dl to 30.

If D2 is 31 and Dl is 30 or 31, change D2 to 30.

If Dl is 31, change Dl to 30.

Once these adjustments are made, the formula for calculating the number of days between two dates is as follows:

To illustrate the 30/360 day count convention, let's use a 4.625% coupon bond which matures on December 15, 2009, issued by Fannie Mae. Suppose the bond is purchased with a settlement date of June 4, 2007. The first coupon date is June 15, 2007, and the first interest accrual date is December 19, 2006. How many days have elapsed in the first coupon period from December 19, 2006, until the settlement date of June 4, 2007, using the 30/360 day count convention?

Referring back to the 30/360 day count rule, we see that adjustments 1 through 4 do not apply in this example so no adjustments to Dl and D2 are required. Accordingly, in this example:

| Yl= 2006 |

| Ml = 12 |

| Dl = 19 |

| Y2 = 2007 |

| M2 = 6 |

| D2 = 4 |

Inserting these numbers into the formula, we find that the number of days between these two dates is 165, which is calculated as follows:

The actual number of days between these two dates is 165.

Many money market instruments are discount securities (e.g. U.S. Treasury bills, agency discount notes, and commercial paper). Unlike bonds that pay coupon interest, discount securities are like zero-coupon bonds in that they are sold at a discount from their face value and are redeemed for full face value at maturity. Further, most discount securities use an actual/360 day count convention. In this section, we discuss how yields on discount securities are quoted, how discount securities are priced, and how the yields on discount securities can be adjusted so that they can be compared to the yields on interest-bearing securities.

The convention for quoting bids and offers is different for discount securities from that of coupon-paying bonds. Prices of discount securities are quoted in a special way.

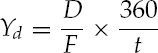

Bids and offers of these securities are quoted on a bank discount basis, not on a price basis. The yield on a bank discount basis is computed as follows:

where

| Yd = annualized yield on a bank discount basis (expressed as a decimal) |

| D = dollar discount, which is equal to the difference between the face value and the price |

| F = face value |

| t = actual number of days remaining to maturity |

As an example, suppose a Treasury bill with 91 days to maturity and a face value of $100 trading at a price of $98.5846. The dollar discount, D, is computed as follows:

Therefore, the annualized yield on a bank discount basis (expressed as a decimal)

Given the yield on a bank discount basis, the price of a Treasury bill is found by first solving the formula for the dollar discount (D) as follows:

As an example, suppose a 91-day bill with a face value of $100 has a yield on bank discount basis of 5.56%, D is equal to

Therefore,

As noted earlier, the quoted yield on a bank discount basis is not a meaningful measure of the potential return from holding a discount instrument for two reasons. First, the measure is based on a face-value investment rather than on the actual dollar amount invested. Second, the yield is annualized according to a 360-day rather than a 365-day year, making it difficult to compare discount yields with the yields on Treasury notes and bonds that pay interest on an actual/actual basis. The use of 360 days for a year is a common money market convention. Despite its shortcomings as a measure of return, this is the method that dealers have adopted to quote discount notes like Treasury bills. Many dealer quote sheets and some other reporting services provide two other yield measures that attempt to make the quoted yield comparable to that for a coupon bond and interest-bearing money market instrument—the CD equivalent yield and the bond equivalent yield.

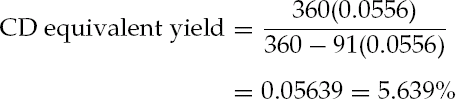

The CD equivalent yield (also called the money market equivalent yield) makes the quoted yield on a bank discount basis more comparable to yield quotations on other money market instruments that pay interest on a 360-day basis. It does this by taking into consideration the price of the discount security (that is, the amount invested) rather than its face value. The formula for the CD equivalent yield is

To illustrate the calculation of the CD equivalent, suppose a 91-day Treasury bill has a yield on a bank discount basis is 5.56%. The CD equivalent yield is computed as follows:

The measure that seeks to make a discount instrument like a Treasury bill or an agency discount note comparable to coupon Treasuries is the bond equivalent yield as discussed earlier in the chapter. This yield measure makes the quoted yield on a bank discount basis more comparable to yields on Treasury notes and bonds that use an actual/actual day count convention. The calculations depend on whether the short-term discount instrument has 182 days or less to maturity or more than 182 days to maturity.

Discount Instruments with Less Than 182 Days to Maturity

To convert the yield on a bank discount to a bond-equivalent yield for a bill with less than 182 days to maturity, we use the following formula:

where T is the actual number of days in the calendar year (that is, 365 or 366). As an example, using a Treasury bill with 91 days to maturity yielding 5.56% on a bank discount basis, the bond-equivalent yield is calculated as follows:

Note the formula for the bond-equivalent yield presented above assumes that the current maturity of the discount instrument in question is 182 days or less.

Discount Instruments with More Than 182 Days to Maturity

When a discount instrument (e.g., a 52-week Fannie Mae Benchmark bill) has a current maturity of more than 182 days, converting a yield on a bank discount basis into a bond-equivalent yield is more involved. Specifically, the calculation must reflect the fact that a Benchmark bill is a discount instrument while a coupon Treasury delivers coupon payments semiannually and the semiannual coupon payment can be reinvested. In order to make this adjustment, we assume that interest is paid after six months at a rate equal to the discount instrument's bond-equivalent yield and that this interest is reinvested at this rate.

In contrast to discount instruments, some money market instruments pay interest at maturity on a simple interest basis. Notable examples include federal funds, repos, and certificates of deposit. Interest accrues for these instruments using an actual/360 day count convention. We define the following terms:

| F = face value of the instrument |

| I = amount of interest paid at maturity |

| t = actual number of days until maturity |

| Y360 = yield on a simple interest basis assuming a 360 day year |

The following formula is used to calculate the dollar interest on a certificate of deposit:

As an illustration, suppose a bank offers a rate of 4% on a 180-day certificate of deposit with a face value of $1 million. If an investor buys this CD and holds it to maturity, how much interest is earned? The interest at maturity is $20,000 and is determined as follows:

It is often helpful to convert a CD yield that pays simple interest on an actual/360 into a simple yield on an actual/ 365 basis. The transformation is straightforward and is accomplished using the following formula:

To illustrate, let's return to the 180-day certificate of deposit yielding 4% on a simple interest basis. We pose the question: What is this investor earning on an actual/365 basis? The answer is 4.056% and is calculated as follows:

Suppose that $100 is invested for one year at an annual interest rate of interest of 4%. At the end of the year, the interest received is $4. Suppose, instead, that $100 is invested for one year at an annual rate, but the interest is paid semiannually at 2% (one-half the annual interest rate). The interest at the end of the year is found by first calculating the future value of $100 one year hence:

Interest is therefore $4.04 on a $100 investment. The interest rate or yield on the $100 invested is 4.04%. The 4.04% is called the effective annual yield.

Investors in certificates of deposit will at once recognize the difference between the annual interest rate and effective annual yield. Typically, both of these interest rates are quoted for a certificate of deposit, the higher interest rate being the effective annual yield.

To obtain the effective annual yield corresponding to a given periodic rate, the following formula is used:

where m is equal to the number of payments per year.

To illustrate, suppose the periodic yield is 2% and the number of payments per year is two. Therefore,

We can also determine the periodic interest rate that will produce a given effective annual yield. For example, suppose we need to know what semiannual interest rate would produce an effective annual yield of 5.25%. The following formula can be used:

Using this formula to determine the semiannual interest rate to produce an effective annual yield of 5.25%, we find

This chapter introduces some of the fundamental calculations used in money markets around the world. The chapter started with the procedures used for calculating the number of days between two dates called day count conventions. Some money market instruments are discount instruments. The basic formulas for yield and price are discussed for each. Furthermore, some of these securities calculate interest using a 360-day while others use a 365-day year. The method for converting a CD yield into a simple yield on a 365-day basis is presented. The last section of the chapter details the conversion of a periodic interest rate into an effective annual yield.

Fabozzi, F. J., and Mann, S. V. (2001). Introduction to Fixed Income Analytics. Hoboken, NJ: John Wiley & Sons.

Fabozzi, F, Mann, S. V., and Choudhry, M. (2002). The Global Money Markets. Hoboken, NJ: John Wiley & Sons.

Fabozzi, F. J., and Thurston, T. (1986). State taxes and reserve requirements as major determinants of yield spreads among money market instruments. Journal of Financial and Quantitative Analysis, December: 427-436.

Mayle, J. (1994). Standard Securities Calculation Methods, vols. 1 and 2. New York: Securities Industry Association.

Stigum, M., and Robinson, F. (1996). Money Market & Bond Calculations. Chicago: Irwin.