G. TIMOTHY HAIGHT, DBA

President, Menlo College and Chair of the Board, Board of Commonwealth Business Bank (Los Angeles)

DANIEL D. SINGER, PhD

Professor of Finance, Towson University

Abstract: Commercial real estate is seen as providing an attractive alternative to investing strictly in stocks and bonds. Even though commercial real estate values can be volatile their addition to an investor's portfolio of assets will reduce risk without necessarily compromising return. In fact, the advantages of personal control, financial leverage, tax shields, and an inflation hedge promise to increase the returns available to investors in commercial real estate. To be successful, commercial real estate investors must take consideration of the location, type of commercial real estate, and the stage of the local commercial real estate cycle. The greatest risk to investors of well-chosen commercial real estate is a lack of liquidity, but this problem can be minimized through the ability to successfully manage long-term compounding cash flows. The returns and risks to the commercial real estate investor are found to be sensitive to the organizational form in which the property is held. While the advantages and disadvantages of various organizational forms are considered, particular attention is paid to the limited liability company as being the vehicle of choice for most commercial real estate investors.

Keywords: location, diversification, financial leverage, operating leverage, limited liability partnership, limited liability company

Investors have a wide array of opportunities when seeking to build wealth and achieve financial independence. Each path will expose the investors to substantial rewards while also exposing them to unanticipated risks. Ultimately, one must choose the investment strategy that best suits his/her long-term goals, time horizon, temperament, and risk aversion. For many individuals, commercial real estate investing has proven to be a very rewarding choice. Over time, commercial real estate has performed remarkably well and is expected to continue to perform well over the next few decades. However, as in all investments, success in commercial real estate investing requires one to have a complete understanding of the market. The real estate market is characterized by cycles of overbuilding and price declines. Thus, timing becomes a crucial ingredient in the development of a successful wealth creation formula.

In this chapter we introduce some basic principles in real estate investing, explain the advantages and disadvantages of real estate as an investment, and the various types of business forms that can be used when investing in real estate. In the next chapter, the types of commercial real estate are explained.

Regardless of the type of commercial real estate selected, the leading factor affecting value and therefore investment performance is location. Real estate properties are differentiated from most other financial or real assets by their uniqueness. No two hotels are exactly alike, no two pieces of undeveloped land are alike, no two office buildings are alike, no two shopping centers are alike, and so on. Commercial real estate is not a commodity. As such one property may not be interchangeable with another. Each property is different because it is in a different physical location. This makes location one of the most important attributes of any piece of commercial real estate.

The first thing to understand about location is that location is not an absolute. There is no such thing as a generically "good" location (or a generically "bad" location.) The desirability of a particular site is relevant only in terms of its intended purpose. A property that is good for a shopping center is not necessarily good for an apartment, an office building or a factory. Assessing the value of a property always requires the strategic perspective that begins with a determination of the intended purpose for the property.

Only in that context are the actual physical attributes of that site relevant. Physical attributes of a site would include the current use of the property, its location with respect to traffic patterns, relevant zoning laws, the contour of the land, the attributes and uses of adjacent or neighboring parcels of land, the effective marketing area or impact zone of the property and trends in adjacent, neighborhood, local, or regional land use.

Another factor to consider in the valuation of commercial real estate is the impact of subjective perception. Certainly, a piece of property has an objective reality. However, that objective reality may not be as important as the subjective lens through which that property is viewed. An objective reality might describe 50 acres of rugged land surrounding a dismal swamp located 20 miles from the nearest urban area. A subjective perspective might be to consider land as a nature preserve, featuring select executive home sites surrounding ecologically important wetlands, which provide protection for a living environmental laboratory. The objective reality might be a rundown hotel adjacent to a metropolitan central business district whose desirability is threatened by crime in the neighborhood. The subjective perspective might be that the (refurbished) hotel could become a badly needed retirement community for area residents that is distinguished by its access to urban amenities and its significant architectural and historic significance. An investment in such a property could be thought of as a beacon of successful urban renewal that could revitalize the neighborhood. It is all in the perspective. A lot of highly successful commercial real estate development occurs because someone is able to think "outside the box."

A key to successful investing, in general, is diversification. Specifically, diversification has that wonderful property of lowering risk without necessarily lowering gain (and often raising gain). We recommend that most investors should be diversified into real estate. The inclusion of commercial real estate into an equities portfolio may enhance the overall performance and lead to risk reduction. We further argue for diversification within the commercial real estate sector for the same reasons. To be sure, commercial real estate entails a range of investment choices from apartments, hotels and motels, office buildings, manufacturing facilities, and many more alternatives.

"Give me where to stand, and I will move the earth," said Archimedes, referring to the notion that with a long enough lever he could move the earth itself. The power of leverage is that great. This is as true in finance as it is in physics. Financial leverage is simply the extent to which debt is used to finance real estate. For example, let us assume that an individual purchases an apartment building for $1 million. Further assume that the owner may put down as little as 25% of the purchase price and borrow the rest ($250,000 equity and a $750,000 mortgage). Now, let us assume that the apartment complex rises in value to $1,100,000. This results in a gain of 10%. By employing leverage, the owner experiences a gain of 40%. This is due to his $250,000 equity investment growing to $350,000. Leverage makes the investor's money work harder.

Leverage is not unique to real estate. Stockbrokers typically offer "margin" financing on stocks bought through their brokerage. However, more leverage is generally available for real estate investment because, while the commercial real estate market certainly has its ups and downs, it has nothing like the volatility of the stock market. Lenders feel more secure about their ability to recover their obligations when the value of those obligations is secured by a mortgage to real property whose value stays relatively constant.

Successful real estate investors optimize (not maximize) their leverage. The general rule is "Borrow to buy, sell for cash." More leverage can make a good investment a great investment. Wise real estate investors generally look for those properties that provide the most financing. To optimize leverage, many investors have a specific strategy that they use in identifying investment opportunities. This involves acquisition strategies that minimize the cash necessary to get into a project and divestiture strategies that look to all cash exits. Such strategies would include minimizing the down payment, borrowing the down payment, extending the life of the loan, and borrowing interest only with a balloon payment for the principal.

The reason investors want to optimize leverage, rather than maximize it, is that increased leverage brings about increased risk. In this case the additional risk comes from the fixed obligations to pay interest (and perhaps principal). Real estate investing always involves juxtaposing an uncertain cash flow coming in against a certain cash flow that must be paid out. Where this cash flow coming in is used to fund the cash flow going out (as is usually the case), this raises the possibility that the funds that were supposed to come in do not. This then puts the highly leveraged investor in a hard place. Money can fail to come in because the lessee is unable to pay, an argument with the lessee goes to court (the legal process is unbelievably slow and typically works to the disadvantage of the creditor), or the lessee, for some other reason, does not want to pay. Compelling such a person to pay is typically a long and arduous process, and while this process goes on, no money is coming in. Thus, how much leverage to use is ultimately a decision the investor makes based upon his or her preferred trade-off between risk and return.

Operating leverage is a characteristic commonly found in real estate properties due to its high proportion of fixed cost to total costs. This characteristic can be described in terms of the relationship between sales volume and profitability of a piece of property. Commercial real estate generally has a large degree of operating leverage due to its fixed costs. When fixed costs are high relative to variable costs, small increases in sales will generate large increases in profits. The other side of the coin is that large fixed costs require a substantial volume of sales to break even.

The presence of such operating leverage means that when the revenues are large, the project is wildly successful, but if the revenue is not there, disaster looms. The point about operating leverage is that very small differences in sales can make for very large differences in profits. This makes predicting the failure or success of a real estate project more difficult.

Operating leverage translates into business risk. Even where the real estate investor intends to take a very passive role in a development as a lessor, he or she is still effectively a partner with the lessee. Where the lessee is successful, the course of the lease will run successfully and both parties will be happy. Where the lessee is unsuccessful, the course of the lease will be troubled and both parties will be unhappy.

Real estate values tend to rise with inflation. In fact, much real estate often rises faster than inflation because it is in relative limited supply compared to other consumer goods and services. Because real estate supply tends to be inelastic (insensitive to prices), as demand increases prices will rise faster in this sector.

Of course, a word of caution is necessary. Not all real estate rises in lockstep with inflation. There are variations in the price of real estate between regions, within regions, within states, within cities, and even within neighborhoods. Much depends on location and the demand for property at that location. Great care must be exercised in the selection of specific commercial real estate opportunities (location, location, location.)

Real estate ownership is encouraged by the tax system. Two important advantages come into play here. The first is interest costs. The second has to do with the concept of depreciation. Both of these factors combine to make real estate investing very attractive.

Interest costs can be fully tax deductible for any commercial real estate investment. This means the cost of funds is reduced by your marginal tax rate. As an owner, if you finance real estate at 8% and you are in the 40% tax bracket, your real cost of financing will be 8% × (1 — 0.4) = 4.8%.

The second important tax advantage to owning real estate is the ability to depreciate any property (the buildings, not the land) being rented. Depreciation is a legitimate (noncash) deduction used to offset revenue that would otherwise be subject to taxes. This means you can show a loss on your real estate investment, and, depending on how the deal is structured, use that loss to reduce your personal income, and thus lower your taxes. Anything to do with taxes tends to be a bit tricky and depreciation is no exception. Real estate rental is considered a passive activity and losses from a passive activity can only be used to offset passive income (not wages and salaries). However, if an individual actively participates in managing the rental property (as evidenced by selecting tenants, collecting rents, visiting the property, and doing maintenance—all of which are tax deductible in themselves), then the individual may deduct up to $25,000 from earned income, provided he or she does not have adjusted gross income in excess of $100,000 when the amount of loss that can be deducted is phased down to where adjusted gross income reaches $150,000 and no loss at all may be applied to earned income. There are a number of other constraints here having to do with marital status and the like. There is also something called an alternative minimum tax (AMT) to consider. An investor needs to consult with a tax professional to see how he or she may be impacted by the tax code. If an investor can write off $25,000 of paper losses due to depreciation and is in the 40% tax bracket, then he or she will receive a tax saving-a bottom line-of $10,000 in real dollars.

Many individuals want to gain more "control" over their lives. The regimen of working for someone else, taking orders, and being subject to an array of arbitrary rules may feel stultifying. It is not uncommon for such individuals to want to "start their own business" to gain more control over their lives. For many people, this may not be a practical alternative. However, there may be another path to financial independence. Commercial real estate is an activity you control entirely. You find the opportunities, arrange the financing, bring all the elements together, and create something where there was nothing before. An individual can enter this business starting small and staying small, with the real estate investing being a profitable hobby. As an alternative, an investor can start small and over time, with a few good moves, grow his or her business into a high-paying full-time job.

Commercial real estate investors are debtors. They borrow money now to pay it back later. In an inflationary environment this confers a tremendous advantage to the buyer. In theory, interest rates adjust for the level of inflation by adding an inflation premium to the real rate of interest. In the real world, this adjustment process appears slow and uncertain. There have been a number of times within the past two decades where the rate of inflation exceeded the nominal rate of interest. Monetary history suggests a pattern in the world of modern finance where debtors have benefited from borrowing more valuable dollars and paying back with less valuable dollars.

The value of a dollar (or any unit of currency) is ultimately determined by what it will buy. What it will buy is determined by the price level of goods and services that, in turn, is determined by the demand for and supply of those goods and services. While government statistics show little inflation in the first few years of this decade, these indices do not necessarily reflect the buying pattern of real estate investors. It may be argued that broad-based indices (such as the Consumer Price Index), which rely on fixed market baskets of goods and services really understate the true level of inflation relevant to business decision makers.

There are a number of possible causes of inflation. One of the most common causes of inflation can result from the money supply increasing as a result of increasing government debt. Government debt increases because politicians basically find that, when they vote for benefits for people, they get congratulated for doing a good job by those people affected. When they vote for more taxes, they generally get voted out of office. Therefore, politicians tend to spend more without generating the needed tax revenues. The only way that can be done is to create more debt. What is the future for inflation in the United States? The effects of inflation are so powerful and pervasive that economists see inflation as a primary factor in redistributing wealth in our society. If inflation is inevitable, the real question is which side of this transfer will you be on?

A hallmark of commercial real estate investment is that such investments yield compounding cash flows. Taking advantage of this requires a fairly long-term horizon, but that gets back to the tortoise and hare metaphor. An individual can go to Las Vegas, put down $10,000 on black at a casino roulette table, and double his or her money—or lose it all! The odds are against winning and there is a high degree of risk, but at least the issue is decided quickly. Or an individual can put $10,000 down on a well-located duplex apartment that will earn 21% annually over the next 15 years with very little risk. It takes a long time, but the $10,000 turns into $174,494! This is the miracle of compound interest. In finance, the tortoise not only finishes the race, the tortoise wins the race, too! Rabbits show a burst of speed that looks good for a short time, but they rarely finish the race and almost never win the race. Compounding cash flows are the surest way to wealth creation.

Liquidity in finance refers to the ability of an asset to be exchanged for cash without loss of value. Publicly traded stocks have good liquidity. (That is the purpose of having "stock markets.") Commercial real estate investments typically do not. If you have invested in a small office building and the time has come to liquidate that investment, it cannot be done overnight, or, at least, it cannot be done overnight without great loss of value.

Of course, much will depend on prevailing supply and demand conditions. It is possible that an investor will decide to liquidate in a period of high demand and short supply. In that case, a sale may be arranged in a few weeks. If the decision is made to liquidate, when market conditions are adverse, then arranging a sale may take months or years.

Investing, in whatever form, deals with uncertainty. This is true for stocks, bonds, and, most importantly, commercial real estate. Uncertainty about the future translates into risk. Financial statements are tools of tremendous power that can be used to reduce that uncertainty. Financial statements may not lead the investor to a definitive answer. However, they will lead to a better understanding of these risks.

Income statements are often not what they seem. "The devil is in the details" is never truer than when it comes to determining what financial statements mean. Income statements attempt to show how a business performs over a specified period of time. Most commonly, income statements are presented on a yearly, quarterly, or monthly basis. If the purpose of the income statement is to provide insight into a property's performance, an immediate problem arises over what "performance" means. Performance is often discussed in generalities like "profit," "earnings," or "the bottom line." There is nothing wrong with using such terms per se. The problem is they tend to mean different things to different people. Using such terms without defining them leads to misunderstandings and misunderstandings lead to mistakes.

There are two basic kinds of income statements. They bear some similarity but are, in fact, quite different. They are most powerful when used in combination. One type of income statement depicts past performance. Thus, a property's revenues, expenses, profits, and losses are reported for a specific time period. As investors, we are generally more interested in the future than the past. Thus, the true worth of these historic financial reports is that they may give us some hints into the future. The statements can help us in constructing the second type of income statement, which is called a pro forma income statement. The astute investor must have the ability to read and understand the income statement.

This issue is closely related to liquidity. If real estate is inherently illiquid, that means it takes time to realize the property's value. But what is its value anyway? This is certainly an area that it is easy to disagree on.

When investors are selling a commercial property, they are really selling a stream of income. Valuing this stream of income requires two factors to be considered. First, one must quantify the stream of income itself, and secondly, one must determine the risk associated with that stream of income.

The stream is simply the net of cash inflows and outflows associated with a given real estate investment. Typically, the inflows can be from rental income while the outflows are associated with normal operating and maintenance expenses along with financial costs (interest and principal) and taxes. The income statement described earlier is a useful tool in constructing cash flow statements.

The second element (after determining income) in determining value is determining the risk associated with that value. This risk has to do with the fact that the income anticipated might not occur, or its value may in some sense be diminished. The use of a discount factor is commonly used to adjust the cash flows to take this into account.

Thus, discounting that income to its present value explicitly quantifies the risk associated with income.

If a property is generating an income stream of $10,000 per year, and that condition is expected to persist for the foreseeable future and a discount factor of 20% is considered appropriate to the risk level of that income, then the value of that property may be determined by the following equation (where n is any number of periods of time):

Equation (48.1) says that the value of the property is the present value of its income (however measured) discounted at a rate of 20%. (Stated in real estate lingo, "its value is equal to five times earnings.") This is the general rule for determining the value of every kind of commercial real estate property. That is, ultimately, its future earnings and its corresponding risks determine real estate's value. In this case the income level is determined to be $10,000 and those earnings in the future are discounted at an annual rate of 20%. The exponential in this series allows for the compounding effect to take place.

Where disagreements over value take place (and divergent opinions are common in this area), those disagreements center either on the quantity of earnings or the quality (associated risks) of those earnings, that is, whether this property is really generating $10,000 in income or whether there is another way to look at it. Where the buyers and sellers forecast of future earning differ, each will arrive at different valuations. Furthermore, perhaps the seller is basing his analysis on cash flow, while the buyer thinks the net income figure would be more appropriate.

The future is always hard to predict. One way to deal with the risk of the unknown is to increase the discount rate to reflect that risk. A seller might be offering the property for the $50,000, as shown in equation (48.2), because he or she has confidence in the future ability of the property to generate that $10,000 year after year. Potential buyers may not share that confidence. For example, potential buyers may know less about the property and thus, may have less confidence in the property's ability to generate income in the future. Thus, prospective buyers might want to discount that $10,000 at a higher rate, say 40%, to compensate for that uncertainty. Therefore, these buyers will offer to buy the property at 2.5 (1/0.4) times earnings. When market conditions deteriorate, buyers become increasingly fearful of what the future might bring. They respond by seeing the real estate as deserving of higher discount rates. That is why prices fall on the downside of the market.

Another variation of equation (48.1) commonly encountered is where future income is likely to grow. (In equation (48.1), future income was projected to be constant.) This situation is expressed in equation (48.3).

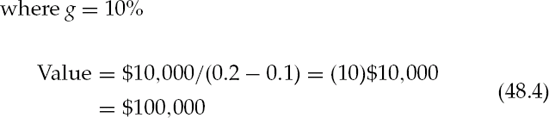

Again, equation (48.4) is just a simpler way of expressing equation (48.3), which says that the property is now worth $100,000 (10 times earnings) because this income stream is expected to grow at 10% annually. Here again the assumptions underlying the valuation may cause differing views as to the property's value. If it is easy to disagree on the income measure to be used and what the appropriate discount rate is determined to be, then it is really easy to disagree on what the future rate of growth will be.

Equation (48.4) is the most commonly used framework to determine value. That is, the value of a commercial real estate property depends on how much income it will generate, the appropriate rate at which that income should be discounted, and how much that future is likely to grow in the future.

Leverage is a good thing, but too much leverage can be a bad thing. Leverage increases the potential return on a project, while at the same time increasing the risk associated with that project. This is why it is better to optimize leverage than maximize it. Too much borrowing jeopardizes the success of a real estate investment as surely as too little leverage. It is a matter of balance to be decided by the investor's taste and preference for the trade-off between risk and return.

Where ownership of the property is direct, the commercial real estate investor is going to need to be involved with searching for the project, evaluating the project, financing the project, and (if acquired) managing the project. Even where the commercial real estate investment involves a sale-lease-back arrangement and there is no property to search for, and the evaluation is cut and dry, the project will still not manage itself. There are always ongoing issues to be dealt with between the lessor (the owner) and lessee (the tenant). Commercial real estate investment is not a passive activity. It requires active, focused, intense participation or things are likely to go terribly wrong. Commercial real estate investment is not for the detached.

The choice of which business form to adopt, as a vehicle to invest in commercial real estate, is critical to the success of the real estate investor. Different business forms have different tax implications, different implications for investor liability, different implications for control, and different implications for cost. There is no one "best" business form. The business form adopted should be the one that best meets the individual investor's needs. The investor's needs have to do with the investor's goals, personal situation, and the particular type of investment being considered. In this context the investor must weigh the trade-offs between tax advantages, liability, control, and cost.

Perhaps the most important issue impacting the business form chosen is the potential liability for the investor by the business organization or agents of the business organization. The legal principle is qui facet per ahum, facet per se. That is, "who acts through another, acts himself." All business forms are governed by the concept of agency. Agency is a legal relationship in which one person (real or artificial, that is, a corporation, limited liability company, and so on) represents another and is authorized to act on his or her behalf. Agency law is quite broad and covers the whole body of rules that society recognizes and enforces in regards to situations where one person acts for another. Without agency law, business could not act. Each individual would only be able to represent himself.

The form that the business takes affects the liability of the owners. To what extent is the business and the investor the same? To the extent they are the same, the investor will be responsible for torts of any agents of the business. (A tort is damage, injury, or a wrongful act done willfully, negligently, and not involving breach of contract. If the issue is a breach of contract, then the issue is dealt with in a civil suit.)

Agents of a business include employees and those to whom the business has given a power of attorney. Independent contractors are not considered agents. Principals in a business are generally responsible for the acts of their employees. (Agency can be created by contract, by conduct that implies agency or by "estoppel" (apparent authority). This means an employee of the business may bind the principal contractually, whether the employee has the actual authority to do so, as long as the employee has the apparent authority to do so. Further, even though the owner has committed no act of negligence, the principle can be held negligent if that employee is acting within the scope of their employment.

Agents are expected by law to exhibit a high degree of fidelity to the principal. This would include obeying instructions, acting with skill, protecting confidential information, and the duty to avoid a conflict of interest. The principal, in turn, has a duty to compensate the agent and inform him or her of any risks associated with the agency. When an agent acting within the scope of their employment commits a tort, both the employee, and the principal can be held liable for the tort. This is known as the doctrine of joint and several liability.

The legal framework for business organizations is created at the state level. Although the forms are similar across state lines, the keyword here is similar. A form that would provide a desired advantage in one state may well not do so in another. There is no barrier to creating a business form in a state offering the most advantages. The laws of the state in which it is formed, not the state in which it operates, govern the liability and internal affairs of a business entity. While forming the business in your home state may offer simplicity and cost savings, states such as Delaware and Nevada may, in most cases, offer superior liability and other offsetting advantages.

The following discussion deals with the attributes of these business forms in general. The specific needs of an investor should always be discussed with an experienced attorney to determine the relevance of the laws in that state to the investor's need.

A sole proprietorship is the easiest, most convenient, and least expensive form of business organization. Unfortunately, for the real estate investor interested in increasing and preserving wealth, it is not very good. This form of business has only one owner. There are no formal requirements to create or operate this form. The owner has unlimited, personal liability for all of the business's debts. The owner personally hires all employees, and thus the owner has unlimited, personal liability for the acts of employees. A sole proprietorship is not a separate taxpaying entity. Income is reported on the owner's personal tax return and does not require the filing of a separate tax return. For these reasons, this form of business should usually be avoided.

A general partnership (or simply partnership) must have two or more owners. No formal requirements are necessary to create and/or operate this form. Some states provide for the filing of "Articles of Partnership," so that the arrangement is a matter of public record. All owners have unlimited, personal liability for all of the businesses debts. All owners personally hire all employees, and thus all of the owners have unlimited, personal liability for the acts of employees. In addition, each owner has unlimited, personal liability for the acts of all of the other owners. Partnerships are a separate taxpaying entity: Income is prorated to the owners' personal tax returns and the business files only an information return with the Internal Revenue Service (IRS). Partnerships are a relatively simple business form to create and operate. Exposure to liability is so great in this form that it should not be used. Thus, this form is in a tie for the worst form of business with sole proprietorship.

A limited partnership must have two or more owners and are formally created under state law. One or more owners of the limited partners must be a general partner who has unlimited, personal liability in all of the same ways as a partner in a in a general partnership. At least one owner must be a limited partner (frequently all of the other owners will be limited partners) who has limited liability. Owners who are limited partners are prohibited from participating in the management of the business. Limited partnerships are frequently used to build tax shelters and for estate planning purposes. Income to the partnership is passed through to the owners' personal tax returns and the business files only an information return with the IRS.

The limited liability partnership requires two or more owners as a limited partnership. This business form is formally created under state law, as is a limited partnership, but all of the owners have limited liability for the business's debts. In many states, however, this "limited liability" is less than that afforded to the owners of a limited liability company or a corporation. In some states, notably California and New York, the limited liability partnership may be used only in "professional" practices. Income is passed through to the owners' personal tax returns, and the business files only an information return with the IRS.

In some states, the limited partnership can register as a limited liability limited partnership that has the effect of giving the general partner limited liability. Therefore, all of the owners of the this form of business organization have limited liability for the debts of the business. This form of business organization is usually more costly to start and maintain than a limited partnership because it is subject to more formal statutory rules regarding officers and record keeping. Income is passed through to the personal tax returns of the owners and the business files only an information return with the IRS.

Some states provide for the creation of "registered" limited liability partnerships. This occurs where the limited liability partnership is really a general partnership that has "registered" in the limited liability partnership form to achieve some version of limited liability for all of the owners of the business.

A limited liability company may have one or more owners. This business form is created by state statute where all of the owners have limited liability for the debts of the business. A limited liability company is usually less costly than a corporation to create and maintain because it has more relaxed, less burdensome rules governing operation compared to a corporation. A limited liability company is not a separate taxpaying entity: Income is reported on the personal tax returns of its owners and does not require the filing of a separate tax return when there is only one owner.

In many states, the business interests of the owners of a limited liability company are protected from the claims of the personal creditors of the owners. This advantage is not enjoyed by the limited liability partnership. This advantage may be significant for preserving wealth under adverse conditions. Therefore, the limited liability company combines into one form the best elements from a corporate entity (limited liability for all of the owners) and the general partnership (absence of formalities, low costs, tax benefits). For most commercial real estate investors, this is probably the business form of choice.

It should be noted that while owners have "limited liability" in a limited liability corporation, that limitation only means that the creditors of the corporation cannot go after the personal assets of the owner. To the extent that the owner has assets that remain in the limited liability corporation, those assets are not immune from the claims of creditors. As this form of business organization is relatively new to the business arena, it is important to form the limited liability corporation in a state (such as Delaware or Nevada) that follows the Revised Uniform Limited Partnership Act (RULPA) view in its LLC statutes.

Corporations are formally chartered at the state level and provide for a separation of ownership from management. They are more costly to establish and maintain that other business, but they provide unparalleled protection for the owners from claims against the business itself. Owners elect directors who have the formal responsibility for selecting and monitoring corporate management. C corporations are taxed as entities themselves and repatriate profits to their owners through dividends, which are then subject to the personal income tax (so-called double taxation).

It should be noted that while owners have "limited liability" in a C corporation, that limitation means only that the creditors of the corporation cannot go after the personal assets of the owner. To the extent that the owner has assets that remain in the corporation, those assets are not immune from the claims of creditors.

Subchapter S corporations differ from C corporations only in that profits are not subject to a separate corporate tax and such profits are prorated to the various owners directly where they will be subject to the personal income tax. The term used to describe this is that Subchapter S corporations are treated as "conduits" for tax purposes.

Closed corporations have all the characteristics of a C corporation (double taxation, limited liability, etc.), but are less expensive to charter and maintain. Laws on this type of corporation vary considerable from state to state, however:

Closed corporations generally are held by a single shareholder or closely knit group of shareholders.

The corporation may be formed initially as a closed corporation or may amend its articles of incorporation to include this statement.

A closed corporation's profits are taxed twice: once at the corporate level and again when profits are distributed as dividends to their shareholders. If a closed corporation meets specific IRS requirements, a corporation can file for Subchapter S corporation status and generally avoid paying tax at the corporate level.

The shareholders of a closed corporation are personally liable for the debts and liabilities of the closed corporation only to the extent of their capital contribution.

There are no public investors, and its shareholders are active in the conduct of the business.

Bylaws are not required if provisions, normally included in bylaws, are included in the shareholders' agreement.

Professional corporations are designed to meet the needs of groups of professionals (physicians, dentists, lawyers, etc.) who wish to practice together and wish to organize their business association in a corporate framework. (This will have advantages in transferring and valuing ownership, in the corporation's existence separate from the owners and an indefinite life, but will also include taxation at both the corporate level and the personal level.) Control will be vested in a board of directors that is elected by the shareholders. Costs are formal registration and filing, and reporting requirements vary from state to state.

Professional associations are designed to meet the needs of groups of professionals (physicians, dentists, lawyers, etc.) who wish to practice together and wish to organize their business association in a corporate framework. (This will have advantages in transferring and valuing ownership, in the corporation's existence separate from the owners, and an indefinite life, but will also include taxation at both the corporate level and the personal level.) Control will be vested in a board of directors that is elected by the shareholders. Costs are formal registration and filing, and reporting requirements vary from state to state.

Service corporations are corporations designed to meet the needs of groups of professionals such as physicians, dentists, and lawyers who wish to practice together and wish to organize their business association in a corporate framework. (This will have advantages in transferring and valuing ownership, in the corporation's existence separate from the owners, and an indefinite life, but will also include taxation at both the corporate level and the personal level.) Control will be vested in a board of directors that is elected by the shareholders. Costs are formal registration and filing, and reporting requirements will vary from state to state.

It is possible to reap further advantages in terms of minimizing taxes and minimizing liability by layering different business forms for holding an investment and operating the investment. Using different forms for holding and operating an investment involves using a two-entity structure. In this type of arrangement, an operating entity will carry out the actual business functions, and a holding entity will own the major capital assets of the company, often including the operating entity itself. In this way, you can provide a nearly impermeable shield for your business assets against the claims of business and personal creditors. It is possible for business owners who desire a simplified structure to personally act as the holding entity, although in that case the liability shield will not be as strong.

The use of multiple business forms can be effective in protecting assets by minimizing the amount of vulnerable capital invested within the operating entity. Strategies that would accomplish this result would include:

The owner's personally owning and leasing assets to the operating entity.

A strategic combination of equity and debt funding (debt funding for the operating entity, equity funding for the holding entity).

Encumbering the operating entity's assets with liens that run in favor of the holding entity or owner.

Systematic withdrawals of funds as they are generated.

To avoid the problem of the limited liability being challenged by charging orders, withdrawals of funds should be done on a regular basis, following due procedures. Such withdrawals could include the use of dividends, earned salary and wages to the owners, payments to the owners on leases of property or equipment held by the owner, and factoring account receivables.

Another advantage of a two-entity structure would be to allow for proper planning for federal estate taxes. This important issue is often overlooked in the hurley-burley context of business formation. Many commercial real estate investments thrive and grow to produce tremendous wealth for the owner. Yet, in the absence of effective estate planning, much of this wealth may be paid to the federal government in the form of estate taxes, rather than to the owner's family, when the business owner dies.

A franchise is a contractual arrangement between the owner (franchisor) of some property or type of business that permits another (franchisee) to use that property or type of business. A franchise involves a relationship between the owner and the user. There are a number of situations in which a real estate investor would find it desirable to be either a franchisor or a franchisee. A real estate investor could function as a franchisor to use franchisees to provide capital for a business undertaking, provide en-trepreneurship for a business, and to absorb the risk of loss. A real estate investor might wish to be a franchisee when experience or expertise in a particular business is needed, or when the franchisor's brand or goodwill is a valuable asset.

There are three basic types of franchises: (1) distributorships, (2) business systems, and (3) process systems. Distributorships involve licensing dealers to sell products such as Texaco gasoline stations. Business systems involve the use of a standard method of operation in conjunction with a brand name like Jiffy Lube. Process systems involve the ingredients and procedures used in making something like Pepsi Cola.

The relationship between the franchisor and franchisee is governed by a franchise agreement. As there is normally one large franchisor and many small franchisees, the franchisor usually has a franchise agreement prepared that is offered to prospective franchisees on a take-it-or-leave-it basis. Since franchisors have so much power relative to franchisees, courts will generally interpret any ambiguities in the franchisee agreement in favor of the franchisee. The courts will find the franchisor has an obligation of good faith in such an agreement and will generally not enforce any provision that is inherently unfair.

Entering into a franchisee agreement requires a good deal of disclosure about the nature of the franchise. Both state statutes and Federal Trade Commission rules generally requires such disclosure. Information is the commercial real estate investor's friend in considering the desirability of a franchise. It is important to evaluate all data associated with the franchise and to speak to existing franchisees about their experiences with the franchisor. Information collected should be subject to a thorough analysis of historical and pro forma income statements.

Commercial real estate offers investors significant returns while providing them with means to control risks. Location continues to be the single most important determinant of real estate value. This certainly holds true for commercial real estate. Investors can enhance their diversification and thus reduce risks by including commercial real estate as part of their overall investment portfolio.

There are many advantages to investing in real estate. These include the ability to benefit from financial and operating leverage. Tax advantages also make commercial real estate and attractive investment. Historically, commercial real estate has been an effective hedge against inflation. Clearly, there are disadvantages as well. Real estate is a very illiquid investment. Thus, the holding periods can be quite long. Many investors may become overextended. Additionally, real estate investing requires a degree of management expertise.

The choice of a business form offers greatest opportunities for the investor to control risk, maximize cash flow, and minimize taxes. While there are a variety of choices available, most small (that is, less than $1 million equity) commercial real estate investors will want to choose a structure involving a limited liability company or a Subchapter S corporation. Particularly in combination, a Subchapter S corporation as the holding company and a limited liability company as the operating company offer the most effective protection for both personal assets outside the business and the investment in the business itself. Larger investors may well prefer the more formal setting of a limited liability company holding an operating, conventional C corporation.

Bowman, J. L. (2005). How to Succeed in Commercial Real Estate. Ft. Worth, TX: Mesa House Publishing.

Fisher, S. D. (2006). The Real Estate Investor's Handbook: The Complete Guide for the Individual Investor. Ocala, FL: Atlantic Publishing Group.

Freedman, R. (2006). Broker to Broker: Management Lessons from America's Most Successful Real Estate Companies. Hoboken, NJ: John Wiley & Sons.

Gallinelli, F. (2004). What Every Real Estate Investor Needs to Know about Cash Flow ... and 36 Other Key Financial Measures. New York: McGraw-Hill.

Haden, J. (2006). The Complete Dictionary of Real Estate Terms Explained Simply: What Smart Investors Need to Know. Ocala, FL: Atlantic Publishing Group.

Haight, G. T., and Singer, D. D. (2005). The Real Estate Handbook. Hoboken, NJ: John Wiley & Sons

Hudson-Wilson, S., Fabozzi, F. J., and Gordon, J. N. (2003). Why real estate? An expanding role for institutional investors. Journal of Portfolio Management, Special Real Estate Issue: 12-27.

Hudson-Wilson, S., Gordon, J. N., Fabozzi, F. J., Anson, M., and Gilberto, S. M. (2005). Why real estate? And ... how? Where? And when? Journal of Portfolio Management, Special Real Estate Issue: 12-22.

Kolbe, P., and Greer, G. (1977). Investment Analysis for Real Estate Decisions, 6th edition. Chicago: Dearborn Financial Publishing.

McMahan, J. (2006.) The Handbook of Commercial Real Estate Investing. New York: McGraw-Hill.

Masters, N. (2006) How to Make Money in Commercial Real Estate: For The Small Investor. Hoboken, NJ: John Wiley & Sons.

Peiser, R. B., and Frej, A. B. (2003). Professional Real Estate Development, 2nd edition, Washington, DC: Urban Land Institute.

Schmitz, A., and Brett, D. (2001). Real Estate Market Analysis: A Case Study Approach. Washington, DC: Urban Land Institute.