SHANI SHAMAH

Consultant, E J Consultants

Foreign Exchange Options 702

Abstract: The currency options market shares its origins with the new markets in derivative products. They were developed to cope with the rise in volatility in the financial markets worldwide. In the foreign exchange markets, the dramatic rise (1983 to 1985) and the subsequent fall (1985 to 1987) in the dollar caused major problems for central banks, corporate treasurers, and international investors alike. Windfall foreign exchange losses became enormous for the treasurer who failed to hedge, or who hedged too soon, or who borrowed money in the wrong currency. The investor in the international bond market soon discovered that the risk on their bond position could appear insignificant relative to their currency exposure. Therefore, currency options were developed, not as another interesting off-balance-sheet trading vehicle but as an alternative risk management tool to the spot and forward foreign exchange markets. They are a product of currency market volatility and owe their existence to the demands of foreign exchange users for alternative hedging and exposure management techniques.

Keywords: premium, option writer, call, put, exercise, strike price, European-style option, American-style option, exchange-traded, over-the-counter (OTC), expiry, contract size, spot value, hedge, volatility, spot rate, option buyer, option seller, margin, intrinsic value, time value, delta, gamma, theta, marked-to-market, at-the-money, in-the-money, out-of-the-money, historical volatility, implied volatility, actual volatility

Since the breakdown of the Bretton Woods agreement in the early 1970s, currencies of the major industrial nations have fluctuated widely in response to trade imbalances, interest rates, commodity prices, war, and political uncertainty. In recent years, the pressure of governments maintaining currency parity has led to the breakdown of quite a few exchange rate mechanisms and has, thus, reinforced the need for companies, in particular, to take active foreign exchange hedging decisions in order to prevent the erosion of profit margins.

The currency options market shares it origins with the new markets in derivative products and were developed to bring an extra dimension to the markets in order to cope with the rise in volatility in the financial markets worldwide. Today, currency options are traded in their listed form mainly in Philadelphia and Chicago. There is also a liquid interbank market or over-the-counter (OTC) market, which exists in all of the world's financial centers. By using options, it is possible to take a view not only on the direction of a price change, but also on the volatility of that price.

The aim of this chapter is to give the currency options novice a thorough and comprehensive guide to the product, with clear explanations of the definitions and the technicalities. The math-averse will be pleased to see that there are very few formulae and although Black-Scholes option pricing formulae and the "Greeks" are touched on, the chapter is almost entirely calculus free.

In order to understand foreign exchange options, the most important factor of an option, in comparison to a foreign exchange transaction, is that the buyer has the right but not the obligation to buy or sell a specified quantity of a currency at a specified rate on or before a specified date. For this right, the buyer pays a premium to the seller or writer of the currency option, usually at the outset. For currency options, the premium is often expressed as a percentage of the notional amount covered. The essential characteristics of a currency option for its owner are those of risk limitation and unlimited profit potential. It is similar to an insurance policy. Instead of an individual paying a premium and insuring a house against fire risk, a company pays a premium to insure itself against adverse foreign exchange risk movements. This premium is the buyer's maximum cost.

The terms used in the options market can be confusing, but the principal terms or jargon used can be summarized as:

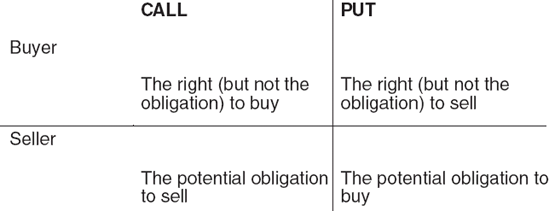

The option buyer is called the buyer and the option seller the writer.

A call gives the buyer the right to buy a specific quantity of a currency at an agreed rate over a given period.

A put gives the buyer the right to sell a specific quantity of a currency at an agreed rate over a given period.

The premium is the price paid for the option. With a currency option this can be expressed in different ways and is usually paid with spot value from the initial deal date.

The principal amount is the amount of currency that the buyer can buy or sell.

Exercise is the process by which the option is converted into an underlying foreign exchange contract.

The strike price or exercise rate is the exchange rate at which the option may be exercised.

Expiry date is the final date on which the option may be exercised.

A European-style option can be exercised at any time but the funds will be transferred on the maturity date. In practice, most European style options are not exercised until the expiry date;

An American-style option can be exercised at any time up to and including the expiry date with the funds being transferred with spot value from exercise.

It is important to note, that due to the nature of foreign exchange, all currency options are a put on one currency and a call on another. For example, a dollar call/Swiss franc put gives the buyer the right to buy dollars and the right to sell Swiss francs.

With a call option, the holder of the option has the right but not the obligation to buy an asset. Essentially, the buyer of a currency call option has the right to buy (take delivery of) a predetermined amount of one currency in exchange for a predetermined amount of another currency up to a predetermined date and at a predetermined exchange rate. The writer of a currency call option has the obligation to sell (deliver) a predetermined amount of one currency in exchange for a predetermined amount of another currency up to a predetermined date and at a predetermined exchange rate.

For example, a call option of Swiss francs against the dollar, expiring in three months' time, for 10 million francs, struck at an exchange rate of 1.67 francs per dollar. (The specified exchange rate in an option contract is known as the exercise or strike price). The buyer of the call option has the right to receive ten million francs from the call option writer and deliver to the writer 5,988,023.95 dollars (10 million francs divided by 1.67 francs per dollar) The writer of this call option, therefore, has the obligation to deliver 10 million francs to the call option buyer in exchange for 5,988,023.95 dollars, at any time up to and including the three-month expiry date.

In the case of a put option, the holder has the right but not the obligation to sell an asset. The buyer of a currency put option has the right to sell (deliver) a predetermined amount of one currency in exchange for a predetermined amount of another currency up to a predetermined date and at a predetermined exchange rate. The writer of a currency put option has the obligation to buy (take delivery of) a predetermined amount of one currency in exchange for a predetermined amount of another currency in exchange for a predetermined amount of another currency up to a predetermined date and at a predetermined exchange rate.

For example, take a put option on Swiss francs against the dollar, expiring in three months time, for 6 million Swiss francs struck at an exchange rate of 1.50 francs per dollar. The buyer of the put option has the right to deliver 6 million Swiss francs to the put option writer in exchange for four million dollars (6 million francs divided by 1.50 francs per dollar) from the option writer. This right expires in three months' time. The writer of this put option, thus, has the obligation to receive 6 million francs from the option holder in exchange for $4 million, at any time, up to and including the three-month expiry date.

The differences between a call and a put option can be shown thus:

Foreign exchange options can be traded on an exchange or in the OTC market (that is, between two parties). Exchange-traded options are standardized contracts with fixed maturity dates, strike prices, and contract sizes, although each exchange has its own contract specifications and trading rules. OTC option specifications are much more flexible as maturity, strike price, amount, and the like can be negotiated before dealing.

Exchange-traded options can be characterized by:

Currencies are quoted mainly against dollars, although recently some crosses have become available.

Strike prices are at fixed intervals and quoted in dollars or cents per unit(s) of currency.

Fixed contract sizes.

Fixed expiry dates, generally at three-month intervals (e.g. delivery on the third Wednesday of March, June, September and December).

Premium paid up front and on the same day as the transaction.

Options are usually American style.

One major advantage of standardized contracts is that the exchange acts as the counterparty to each trade. Credit risk (the risk of the writer defaulting on the option) is therefore minimized, and anonymity between counterparties can be preserved. It should be noted that currency options on the Chicago Mercantile Exchange (CME) are options on futures rather than options on the spot currency. Hence, if a call is exercised, the buyer receives a long futures position rather than a spot position and the opposite for the buyer of a put.

OTC options have the following characteristics:

Strike rates, contract sizes and maturity are all subject to negotiation. An institution can structure its own option requirements, enabling it, for example, to make cross rate transactions.

Maturities can be from several hours up to five years plus.

The buyer has the direct credit risk on the writer.

Only the counterparties directly involved know the price at which the option is dealt.

The premium is normally paid with spot value from the transaction date with delivery of the underlying instrument also typically with spot value from expiry.

Options can be either style but the majority are European style.

For example, Bank A buys from Bank B a 1.5700 European-style sterling call/dollar put on 10 million pounds, with a maturity of six months. Bank A buys the option through the OTC market for a premium of $0.02 per £1 principal. In this example:

Buyer: | Bank A |

Writer (seller): | Bank B |

Strike price: | 1.5700 |

Principal amount: | €10 million |

Expiry date: | 6 months |

Premium: | $200,000(€10 million × $0.02) |

The users of the option market are widespread and varied, but the main users are organizations whose business involves foreign exchange risk. Options may be a suitable means of removing that risk and are an alternative to forward foreign exchange transactions. In general, the exchange-traded option markets will be accessed by the professional market makers and currency risk managers. The standardization of options contracts promotes trad-ability, but this is at the expense of flexibility.

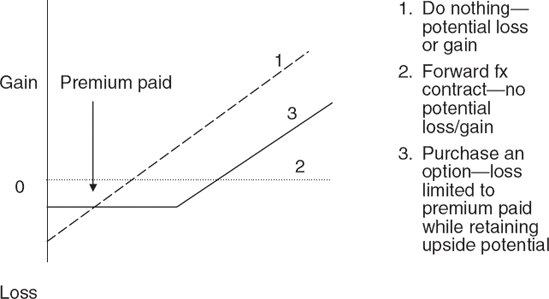

In spite of the fact that options are becoming more and more popular with corporate clients, funds, and private individuals, there is still some client resistance to using options to mange currency exposures. Some clients consider options to be expensive and/or speculative. When you buy an option, the most you can lose is the premium (price paid for the option). In some cases, options can help minimize downside risk, while allowing participation in the upside potential. One of the reasons a client may choose to use an option instead of a forward to manage their downside risk is this opportunity to participate in the upside profit potential, which is given up with a forward contract. Clients who buy currency options enjoy protection from any unfavorable exchange rate movements. This can be seen in Figure 66.1.

Companies use currency options to hedge contingent/economic exposures, hedge an existing currency exposure, and possibly profit from currency fluctuations, while funds may use options to enhance yield.

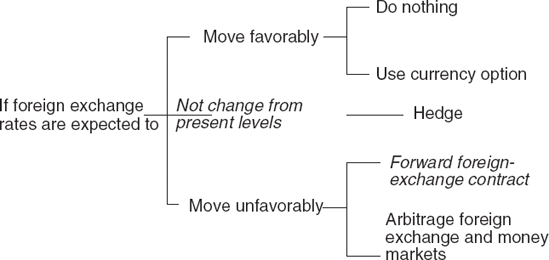

A simplified decision tree as to when to use options, or the various other products available, can be quite useful. The decision-making process assumes a firm view of likely future rate movements, as indecisiveness can only be accommodated by the use of currency options, which can be an expensive solution for many hedging requirements. The more confident the forecast, the simpler the products needed to satisfy needs. The simpler the product, the cheaper the cost. If the forecast is confident that rates will be favorable, then it is best to stay unhedged or to take out an option with the full confidence that the premium cost will be recovered, as the option means that any unexpected downturn will be catered for. Similarly, if no change is expected, then the position should be covered with the cheapest hedge possible. A confident forecast that rates will be unfavorable would call for a forward contract. An example of an exposure management decision tree is shown in Figure 66.2.

Sometimes a strategy may involve more than one option, and some option strategies employ multiple and complex combinations. Certain combinations can yield a low- or no-cost option strategy by trading off the premium spent on buying an option with the premium earned by selling an option.

Hence, in buying a currency option, it may help by limiting downside currency fluctuation risk while retaining upside potential, providing unlimited potential for gain, providing a hedge for a contingent risk, and enabling planning with more certainty. On the other side of the coin, in selling a currency option, it may assist in providing immediate income from premium received and provides flexibility when used with other tools as part of an exchange rate strategy.

Table 66.1 summarizes the applications of foreign exchange options.

For a hedger, in terms of exchange rate risk management, currency options can be used to guarantee a budget rate for a transaction. By buying a call (the right to buy), the maximum cost can be fixed for a purchase; and by purchasing a put (the right to sell), the minimum size of a receipt can be fixed. The purchase of the option involves paying a premium but gives the buyer the full protection against unfavorable moves while retaining full potential to profit should rates subsequently move beneficially. This contrasts with a forward contract, which locks the hedger into a fixed exchange rate, where no premium is payable but no benefit can be taken from subsequent favorable moves.

Table 66.1. Summary of Applications of Foreign Exchange Options

To cover foreign | On existing exposure |

exchange exposure: | On contingent exposure Against a budget rate As disaster insurance |

To speculate: | On the direction of spot On a volatile or quiet market On the timing of spot movement |

To lock in profit: | On changing interest rate differentials |

As an investment: | In a speculative asset To alleviate loan costs To improve deposit yields |

As a funding tool: | To generate a cash flow (short position) To transfer cash to another entity |

As a tax management tool: | To transfer profit and loss over time |

In the case of trading, to assume risk in order to make a profit, traders use options to benefit from both directional views and/or changes in volatility. (This allows profit to be made from expecting volatility to either increase or decrease over a period of time.) For example, in order to take a directional view, an options trader might feel strongly that the dollar will strengthen against the Swiss franc in the next three months from its current level of USD/CHF 1.66. The trader buys a dollar call (right to buy), Swiss franc put (right to sell) option with a strike price of 1.6835, with expiry in three months' time.

The trader has two choices: to hold the option to expiry and if the spot rate has risen to, for example, USD/CHF 1.73, the trader would exercise his right to buy dollars and sell Swiss francs at 1.6835 and, hence, make money. If the spot rate is below USD/CHF 1.6835 at expiry, then the maximum loss is limited to the premium paid for the option. Alternatively, if the spot rate rises, say one month after the trader has purchased the option, the trader could choose to sell the option back. By doing this, the trader will recoup both the time value and intrinsic value of the option.

Quite often, there really seems to be little point in paying a premium for an option when a foreign exchange forward would suffice, but the benefits of an option really do have to be considered. The differences between OTC foreign exchange options and foreign exchange forwards are summarized in Table 66.2 The differences between buying an OTC foreign exchange option and leaving the position unhedged (that is, leaving the position open) are summarized in Table 66.3.

Table 66.2. Summary of the Differences Between OTC Foreign Exchange Options and Foreign Exchange Forwards

Foreign Exchange Options | Foreign Exchange Forwards |

|---|---|

Right but not the obligation to buy or sell a currency | Obligation to buy or sell a currency |

Premium payable | No premium payable |

Wide range of strike prices | Only one forward rate for a particular date |

Retains unlimited profit potential whilst limiting downside risk | Eliminates the upside potential as well as the downside risk |

Flexible delivery date of currency (can buy an option for a longer period than necessary) | Fixed delivery date of currency |

Table 66.3. Summary of the Differences between Buying an OTC Foreign Exchange Option and Leaving the Position Unhedged

Foreign Exchange Option | Open Foreign Exchange Position: |

|---|---|

Right but no obligation to buy or sell a currency | No obligation to buy or sell a currency |

Premium payable | No premium payable |

Retains unlimited profit potential whilst limiting downside risk | Profit and loss potential unlimited |

Flexible delivery date of currency (can buy an option for a longer period than needed) | Indefinite delivery date of currency |

There are two parties involved in foreign exchange options: the option buyer and the option seller (writer). The option buyer has the right to demand fulfilment of the option contract. The owner can exercise the option. The option buyer pays a premium for that right. The option seller (writer) grants the right and receives a premium for accepting the obligation to fulfil the option contract, if the buyer demands. Table 66.4 provides a summary of the risk profile of an options buyer/seller.

Just like with spot and forward foreign exchange contracts, there are risks involved in currency options. If the option expires worthless (that is, is not exercised), then there is no real credit risk. There is transaction-related risk if it is exercised, which is similar to risk on a spot settlement. Because an option buyer enjoys the dual benefits of insurance and upside potential, the option seller/writer is subject to a greater degree of market/price risk than when it enters into a forward contract. As for country risk, it is similar to that for forwards and swaps. Table 66.5 provides an expanded summary of the risk profile of an options buyer/seller.

Because a foreign exchange transaction is, by definition, an exchange of one currency for another, the purchase of one currency is also the sale of another currency. Therefore, the right to buy one currency is also the right to sell another currency. For example, the owner of a Swiss franc call option has the right to buy Swiss francs and also has the right to sell dollars. The writer of a Japanese yen put option is also the writer of a dollar call option. Hence, the terms "call" and "put" option in foreign exchange are interchangeable.

This can be a source of some confusion in the market. For example, a call option struck at a dollar/Japanese rate of 130, is it the right to buy dollars or to buy Japanese yen? Indeed, there is no definitive answer and much depends on the viewpoint of the user and whether the dollar is seen as the base currency or the foreign currency. For the sake of clarity, it is common practice to use both terms, calls and puts. For example, a trader may well ask for a price for a Swiss franc call/dollar put at a strike of 1.67 in order to avoid this confusion.

As shown in the risk profile of an options buyer/seller, there is one very important factor to remember regarding currency options, in that for the buyer of an option, the maximum risk is limited to the premium paid, while for the option seller, the maximum profit is limited to the premium received and the seller is potentially exposed to unlimited losses. Additionally, because of the credit risk involved when writing options, typically there are fewer restrictions on those wishing to buy options than those who wish to sell.

Writing options on exchanges tends to be simpler as the credit risks are controlled by a margin system. The margin is a small percentage of the value of the contract, which must be deposited to cover losses up to a certain limit. The margin is usually adjusted on each trading day and occasionally more frequently to take account of market movements. However, the greater flexibility available in the OTC market allows some of the credit difficulties to be pursued and overcome. Participants in the foreign exchange currency options market include:

Banks providing a service for their clients, to manage their own foreign exchange risk, and in order to take a directional and/or volatility view.

Table 66.4. Summary of Risk Profile of an Options Buyer/Seller

Financial Risk

Profit Potential

Credit Risk

Option buyer

Limited to premium paid

Unlimited

Creditworthiness of option seller

Option seller (writer)

Unlimited

Limited to premium earned

Settlement risk if option is exercised

Table 66.5. Expanded Summary of the Risk Profile of an Options Buyer/Seller

Buy Option Limited risk?

Sell Unlimited risk?

HEDGER

INSURANCE

PROFIT TAKING

Hedging a position against a possible risk: "I am happy not to exercise the option."

Making the most of an existing position: "I don't mind being exercised."

SPECULATOR

LOTTERY

WIZARDRY

Betting on a strong directional market movement: "I must exercise or lose all my money."

Making money out of thin air-based on a market view: "I must absolutely not be exercised."

Supranationals and sovereigns managing the risk exposure of debt denominated in foreign currencies that it has issued.

Multinational companies and their subsidiaries having funds and cross-border transactions in several currencies subject to foreign exchange risk.

Importers and exporters with exposure to fluctuations in exchange rates.

Investors in foreign currency securities with exposure to fluctuations in the currency in which the securities are denominated.

High-net-worth individuals using exchange-traded currency options for speculation on exchange rates because of the gearing they offer.

For example, a British-based company that exports consumer goods to several countries. Currently, the company has contracted to supply US$10 million worth of goods to America and expect to receive payment in three months time, in dollars. The company believe that the dollar will appreciate against sterling over the next three months. There are several alternative strategies:

The company can leave the future cash flow unhedged, as they believe that the exchange rate will move in their favor.

Enter into a forward contract to sell dollars and buy sterling in three months time.

Purchase a three-month sterling call option (the right to buy sterling and sell dollars).

The possible results are:

If the exchange rate does move in the company's favor, then the company will receive a windfall profit on their long dollar position. However, this strategy is very dangerous because if the exchange rate moves contrary to their expectations, their sterling profits will be reduced and could become a loss as their costs are fixed in sterling.

If the company enters into a forward contract, the company is locking in an exchange rate for the supply deal. This gives the company protection against a dollar depreciation but does not allow them to take any profit from a dollar appreciation, which is contrary to their expectations for the exchange rate.

If the company purchases a sterling call option, this will require the company to pay out a premium upfront. However, it will guarantee the company a minimum exchange rate for the supply contract. It allows the company to indulge their expectations that the dollar will appreciate from current levels as, should this expected appreciation occur, they are free to abandon the option and transact in the market at the more favorable exchange rate.

If the company decides to purchase a currency option, it could buy a three-month option, European-style sterling call/dollar put option, with a strike price of £/$1.75 (the right to buy sterling and sell dollars at a rate of £/$1.75). Assume the cost of the option is 1.74% of the sterling amount, that is, £99,428.57 ($10 million/1.75 = £5,714,285.71 × 1.74%). The outcome at maturity is:

Spot Rate | Option Exercised/Not Exercised | Sterling Amount from Deal (Less Premium) |

|---|---|---|

1.8500 | Exercised | €5,614,857.14 |

1.8000 | Exercised | €5,614,857.14 |

1.7000 | Not exercised-buy spot | €5,782,924.37 |

1.6500 | Not exercised-buy spot | €5,961,177.49 |

In viewing whether an option should be viewed as a hedge or as a speculative instrument, a hedger's main concern is the value of the option at maturity. For this reason, any fluctuation of the option's intrinsic value during its life is important but any change in its time value is largely irrelevant. Also, as the option is itself a hedge, no further hedging is required and therefore there are no extra costs. The option premium for a hedger represents:

| Option premium = Intrinsic value + Time value |

where:

Intrinsic value is the advantage to the holder of the option of the strike rate over the forward outright rate.

Time value is a mathematical function of implied volatility, time to maturity, interest rate differentials, spot and the strike of an option.

For example, if the forward outright rate of the dollar against Swiss francs is 1.6000, then for a dollar call (right to buy), Swiss franc put (right to sell) option, with a strike of 1.5700, the intrinsic value of the option would be 0.0300 dollar against Swiss francs. For a dollar put (right to sell), Swiss franc call (right to buy) option, with a strike of 1.5700, then the intrinsic value of the option is 0.0000 dollar against Swiss francs.

In essence, time value represents the additional value of an option due to the opportunity for the intrinsic value of the option to increase and for a trader/speculator, the option premium represents the expected net present value of the cost of delta hedging the option.

A trader's main concern is the value of the option whenever it is marked-to-market. For this reason, any fluctuation in the intrinsic value of the option is important but also any change in the time value will be significant. If the trader, at any time, decided to hedge or partially hedge the option, extra transaction costs may be incurred, which might affect the overall return.

Options can be priced as European-style or as American-style options. The holder of a European-style option has the right to exercise the option only on the expiration date, while the writer of this option may be assigned only on the expiration date of the option. However, the holder of an American-style option has the right to exercise the option on any day until expiry, while the writer of an American-style option may be assigned on any day until expiry.

For example, if an option expires on March 28, with an American-style option, the holder could exercise the option on the March 5 and expect delivery of the currencies involved to take effect two business days later. With a European-style option, exercise can only occur on March 28, with delivery then two business days later. It must be remembered that there is a difference in price between the two styles of option, but only sometimes. The difference in price occurs because there is a difference in the interest rates each currency attracts. With American options, the intrinsic value is priced against the spot or the forward outright price, whichever is the most advantageous. This is because the American option can be exercised for spot value at any time during its life.

If the call currency of the option has a higher interest rate than the put currency, there will be an advantage in calculating the intrinsic value against spot rather than against the forward outright rate. Therefore, the risk that the writer has, is that at some point in time, if the option is so far in-the-money that there is negligible time value remaining, the holder may exercise early. This would mean the writer would incur the differential interest cost of borrowing the higher interest rate currency and lending the lower interest rate currency.

Hence, there is a price difference between the two styles of option, but only sometimes. The difference in price occurs because there is a difference in the interest rates each currency attracts. With American options, the intrinsic value is priced against the spot or the forward outright price, whichever is the most advantageous. This is because the American option can be exercised for spot value at any time during its life. If the call currency (right to buy) of the option has a higher interest rate than the put currency (right to sell), there will be an advantage in calculating the intrinsic value against spot rather than against the forward outright rate. Therefore, the risk that the writer of the American option has is that at some point in time, if the option is so far in-the-money that there is negligible time value remaining, the holder may exercise early. This would mean the writer would incur the differential interest cost of borrowing the higher interest rate currency and lending the lower interest rate currency. If this happens, the option is said to be at logical exercise.

As the American-style option is more flexible, shouldn't it be more expensive all the time? Actually, the American option is not really more flexible than the European option. True, it can be exercised early and therefore the intrinsic value can be realized immediately but unless the option is at logical exercise, the holder would be better to sell the option back and receive the premium. (Remember, the premium represents the intrinsic value of an option plus time value). This is true for both American and European options and in both cases, if the option is not at logical exercise, and the aim is to realize maximum profit, it would be better to sell than to exercise the option.

Examples of cases when it would be better to pay the extra premium and buy a more expensive American-style option are:

In buying an option where the call currency has the higher interest rate and it is expected that the interest rate differential will widen significantly.

In buying an option where the interest rates are close to each other and it is expected that the call interest rate will move above the put interest rate.

In buying an out-of-the-money option with interest rates as in both above and it is expected that the option will move significantly into the money, then the American-style option is more highly leveraged and will produce higher profits.

Delta is the change in premium per change in the underlying. Technically, the underlying is the forward outright rate, but as the option-pricing model assumes constant interest rates, this is often calculated using spot. For example, if an option has a delta of 25 and spot moved 100 basis points, then the option price gain/loss would be 25 basis points. For this reason, delta is sometimes thought of as representing the "spot sensitive" amount of the option.

In addition, delta can also be thought of as the estimated probability of exercise of the option. As the option-pricing model assumes an outcome profile based around the forward outright rate, an at-the-money option has a delta of 50%. It falls out-of-the-money options and increases for in-the-money options, but the change is nonlinear, in that it changes much faster when the option is close-to-the-money.

An option is said to be delta-hedged if a position has been taken in the underlying in proportion to its delta. For example, if one is short a call option on an underlying with a face value of $1 million and a delta of 0.25, a long position of $250 000 in the underlying will leave one delta-neutral with no exposure to changes in the price of the underlying, but only if these are infinitesimally small.

The delta of an option is altered by changes in the price of the underlying and by its volatility time to expiry and interest rates. Hence, the delta hedge must be rebalanced frequently. This is known as delta-neutral hedging.

Gamma is the change in delta per change in the underlying and is important because the option model assumes that delta hedging is performed on a continuous basis. In practice, however, this is not possible as the market gaps and the net amounts requiring further hedging would be too small to make it worthwhile. The gapping effect that has to be dealt with in hedging an option gives the risk proportional to the gamma of the options.

An option's gamma is at its greatest when an option is at-the-money and decreases as the price of the underlying moves further away from the strike price. Therefore, gamma is U-shaped and is also greater for short-term options than for long-term options.

Volatility, in essence, is a measure of the variability (but not the direction) of the price of the underlying instrument, essecntially the chances of an option being exercised. It is defined as the annualized standard deviation of the natural log of the ratio of two successive prices. Historical volatility is a measure of the standard deviation of the underlying instrument over a past period. Implied volatility is the volatility implied in the price of an option. Actual volatility is the actual volatility that occurs during the life of an option. It is the difference between actual volatility that occurs during delta hedging and the implied volatility used to price an option at the outset, which determines if a trader makes or loses money on that option.

Theta is the depreciation of the time value element of the premium, that is, it measures the effect on an option's price of a one-day decrease in the time to expiration. The more the market and strike price diverge, the less effect theta has on an option's price.

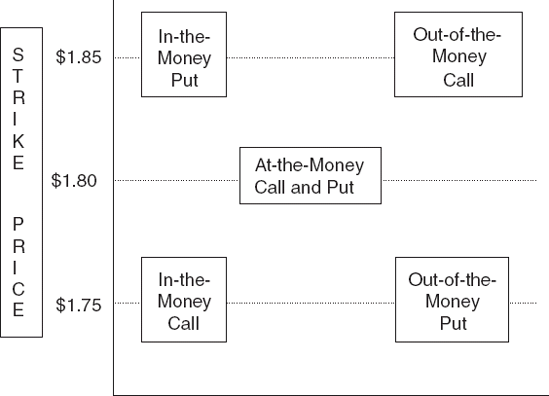

An in-the-money option is an option that describes an option whose strike price is more advantageous than the current market price of the underlying and has intrinsic value, that is, the extent to which it is in the money. For a call option, the strike is below the spot rate and for a put option, the strike is above the spot rate. For example, if the pound spot rate against the dollar is at £/$1.80, a $1.75 call on sterling is in-the-money, as is a $1.85 put on sterling. The more an option is in-the-money, the higher the intrinsic value and the more expensive it becomes. As an option becomes more in-the-money, its delta increases and it behaves more like the underlying in profit and loss terms. Hence, deep in-the-money options will have a delta of close to one.

Also, the option has time value, which is a mathematical function of implied volatility, time to maturity, interest rate differentials, spot and the strike of an option. It represents the additional value of an option due to the opportunity for the intrinsic value of the option to increase. However, it is difficult to quantify, as it is very subjective. It is a wasting asset, so time value declines as expiration approaches and at a more rapid rate.

An option is said to be out-of-the-money when it has no intrinsic value and describes an option whose underlying is above the strike price in the case of a call, or below it in the case of a put. For a call option the strike is above the spot rate and for a put option, the strike is below the spot rate. Again, as above, using a spot rate of $1.80 per pound, a $1.85 sterling call and a $1.75 sterling put option are both out-of-the-money.

The more the option is out-of-the-money, the cheaper it is, since the chances of it being exercised gets slimmer. Its delta also declines and it becomes less sensitive to movements in the underlying.

An option that is at-the-money is one whose strike price is set at the same level as the prevailing market price of the spot or underlying forward contract. For example, with a pound against the dollar spot rate at $/£1.80, a $1.80 sterling call option is said to be at-the-money spot (see Figure 66.3).

In summary, intrinsic value is simply the difference between the spot price and the strike price.

For call options:

In-the-money | = Spot price is below option strike (exercise) price. |

Out-of-the-money | = Spot price is above option strike (exercise) price. |

At-the-money | = Spot price and option strike (exercise) price are the same. |

and for put options:

In-the-money | = Spot price is below option strike (exercise) price. |

Out-of-the-money | = Spot price is above option strike (exercise) price. |

At-the-money | = Spot price and option strike (exercise) price are the same. |

In addition, it should be noted that intrinsic value versus time value can be explained as:

In-the-Money | Out-of-the-Money | At-the-Money |

|---|---|---|

Put/Call Time-value decreases as the option gets deeperin-the-money, while intrinsic value increases | Time-value decreases as the option gets deeper out-of-the-money, while intrinsic value is zero | Time value is at a maximum when an option is at-the-money, while intrinsic value is zero |

A cause of some confusion in the market, which is more semantic than real, occurs when the forward or futures price differs from the spot. For example, if sterling against the dollar spot is $1.80 and the March forward/futures price is $1.75, the $1.80 sterling call for March could be said to be at-the-money against the spot but out-of-the-money against the forward/futures price. Alternatively, the $1.75 sterling call for March is in-the-money against the spot rate but at-the-money against the forward/future price. Thus, traders usually resolve these problems by using the terms "at-the-money spot" to refer to the $1.80 call and "at-the-money forward" to refer to the $1.75 call, in this particular example. Hence, with a Black-Scholes model, the delta of a European-style at-the-money forward option will always be 0.5. However, because forwards commonly trade at a premium or discount to the spot, the delta may not be equal to 0.5.

The premium is the price paid for an option and with a currency option this can be expressed in different ways. It is usually paid with spot value (two business days) from the initial deal date. Hence, the option premium is paid up front.

It is the option buyer who pays the premium so that they may have the opportunity of benefiting from a favorable exchange rate movement. The potential loss is limited to the option premium, and there is usually unlimited profit potential. However, the option seller receives a premium as payment to assume the risk of an adverse exchange rate movement. As summarized in Table 66.6, the seller's potential profit is limited to the option premium and there is unlimited risk of loss.

The option buyer pays a premium to the seller for the right to benefit if the underlying moves in a favorable direction, but risks only the premium if the underlying moves in an unfavorable direction. Thus, from a profit/loss standpoint, a long call option can be described as being equivalent to a long position in the underlying with insurance against the value of the underlying decreasing. Also, again from a profit/loss perspective, a long put option can be described as being equivalent to a short position in the underlying with insurance against the value of the underlying increasing.

Table 66.6. Summary of Potential Profit/Loss for Basic Option Positions

Maximum Profit | Maximum Loss | |

|---|---|---|

Short call | Premium received | Unlimited[a] |

Short put | Premium received | Unlimited[b] |

Long call | Unlimited[a] | Premium paid |

Long put | Unlimited[b] | Premium paid |

[a] Since the order of magnitude of the profit/loss potential is so much greater than the premium, it is unnecessary to subtract the option premium from it. For a long call, the maximum profit would be reduced by the premium paid. For a short call, the maximum loss would be reduced by the premium. [b] Since the price or value of the underlying asset cannot fall below zero, the maximum profit of a long put is actually the strike price minus the premium paid. Similarly, the maximum loss of a short put is actually the strike price minus the premium received. | ||

One unfortunate source of confusion in the currency options market is in the method of quoting the option premium itself. This is not a problem encountered in other option markets as for equities or with gold options. For example, the premium is normally expressed in the same terms as used in the underlying instrument, like $5 per share or $3 per ounce. However, with currency options, as with the foreign exchange market itself, there are alternative ways of quoting the same premium.

For instance, currency futures in Chicago are expressed in the reciprocal form, dollars per currency, and the futures option market adopts the same pricing convention. Thus, the holder of one contract of a February 77 call has the right to buy 125,000 Swiss francs (the underlying value of one futures contract) at an exercise price of $0.77 per Swiss franc. However, in conventional European terms, this would be expressed as a call on Swiss francs struck at $/CHF 1.2987 (1 divided by 0.77). If we assume the premium for this February 77 call is 2.33 ($0.0233) per Swiss franc, then the premium amount per Swiss franc option contract would be:

Were this same trade to have been executed in the OTC market, the premium would more likely have been expressed as a percentage of the strike price, in this case 3.026% (2.33/77 × 100 = 3.026). The total premium amount (ignoring rounding) is the same as the above and is calculated by multiplying the underlying dollar amount by the percentage figure:

This would be the case if the option were purchased in either London or New York. But, if the option were purchased in Switzerland or Germany, also in the OTC market, the premium would more likely be expressed in terms of Swiss francs per dollar rather than dollars per Swiss franc. This can be calculated by multiplying the percentage premium by the Swiss franc spot rate, say $/CHF 1.2850:

This would normally be expressed as 3.89 centimes per dollar. The total premium, in Swiss francs, is therefore:

Components of the premium can be split into two parts, intrinsic value and time value. Thus, as has already been mentioned earlier:

Where intrinsic value is the advantage to the holder of the option of the strike rate over the forward outright rate and time value is a mathematical function of implied volatility, time to maturity, interest rate differentials, spot and the strike of an option.

For example, if the forward outright rate of the dollar against Swiss francs is $/CHF 1.6000, then for a dollar call (right to buy), Swiss franc put (right to sell) option, with a strike of 1.5700, the intrinsic value of the option would be 0.0300 dollars against Swiss francs. For a dollar put (right to sell), Swiss franc call (right to buy) option, with a strike of 1.5700, then the intrinsic value of the option is 0.0000 dollars against Swiss francs.

In fact, time value represents the additional value of an option due to the opportunity for the intrinsic value of the option to increase. In addition, intrinsic value for an American-style option can be defined as the amount the option would be worth if it were exercised immediately. In other words, it is the difference between the strike price and the spot rate. For example, with spot sterling against the dollar at £/$1.8000, the $1.7500 call option has $0.05 intrinsic value. Another way of putting it is to say that the £/$1.7500 call option is in-the-money by 5 cents. Any option trading less than intrinsic value represents a riskless profit for an arbitrageur.

Thus, intrinsic value is simply the amount the option would be worth on expiry, whereby a currency call option has value on expiry by the amount the spot rate is higher than the strike rate and whereby a currency put option has value in expiry by the amount the spot rate is below the strike rate. Obviously, an option will not be worth any more than intrinsic value on expiry because there will be no inherent advantage in owning it. Only if there is some time remaining before expiry will the option have any in addition to its intrinsic worth.

Theorists have devoted a substantial amount of work developing a mathematical model for pricing options and a number of different models exist as a result. All make certain assumptions about market behavior, which are not totally accurate but which give the best solution to the price of an option. Although the formulae for pricing options are complex, they are all based on the same pricing principles.

As mentioned earlier, the price of an option is made up of two separate components:

| Option premium = Intrinsic value + Time value |

There are six factors that contribute to this pricing of an option:

Prevailing spot price

Interest rate differential (forward rate)

Strike price

Time to expiry

Volatility

Intrinsic value

For European-style options, intrinsic value is the value of an option relative to the outright forward price; that is, it represents the difference between the strike price of the option and the forward rate at which one could transact today. Intrinsic value can be zero, but it is never negative.

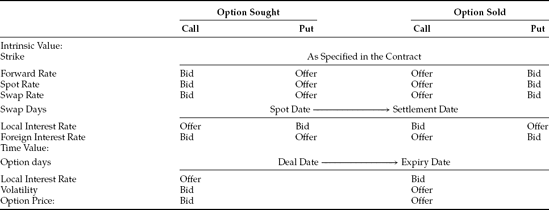

How should one ask for an option price? The required pieces of information, in the preferred order, are as follows:

The two currencies involved and which is the put and which is the call (e.g., dollar put, Swiss franc call).

The period (e.g. two months) or the expiry or delivery date (e.g., expiry December 12, or delivery December 14).

The strike (e.g., 1.5010).

The style (e.g., European or American style).

The amount (e.g. US$10 million).

There are many ways of stating the period, but usually, if one date is stated, it is assumed to be the expiry date but it is much safer to always specify. In the same way, if a 10-day option is requested, it is assumed that the required option has an expiry date 10 days from the current date. If, however, an option is requested with a period in terms of months or years (e.g., three months), the dates of the option are worked out as follows:

Calculate the spot date for that currency pair, using the same conventions as the spot market.

Take the period (e.g., three months from that date), using the forward market conventions.

This gives the delivery date. The expiry date will then usually be two working days before that.

The exceptions occur in any currency pair where spot is not two working days, for example, the Canadian dollar, where the expiry date would be one working date before the delivery date.

Please note that with cross-currencies and dates involving American holidays or in any case where there may be confusion, it is always best to quote both the expiry and delivery dates required.

In asking for an option price, always state which currency is the call and which is the put. For example, does dollar Swiss franc (USD/CHF) put mean a dollar put or a Swiss franc put? On the option exchanges and in the OTC interbank market, this would usually refer to a Swiss franc put dollar call. However, most corporations would probably mean a dollar put. For this reason, always state the case in full (e.g., dollar call Swiss franc put or vice versa).

The preset price is called the strike price or the exercise price, which is the predetermined rate of exchange at which exercise takes place. The strike is usually chosen at a level close to the current foreign exchange spot or forward rate but may be at any reasonable level. The premium (price) of an option is very sensitive to the relationship of the strike to the current spot foreign exchange rate. However, in general, both buyers and sellers of options will select a strike rate based on several factors, including their forecast or expectations of the value of the underlying currency during the lifetime of the option and the option's payoff (profit/loss) profile.

In essence, when selecting a strike rate, the participant will need to consider the upfront premium payment, the break-even point (the point where gains begin), and the leverage of the given risk. If there are limited funds to spend on the premium, then an out-of-the-money strike, which is relatively inexpensive, reflecting less protection and higher leverage, will be chosen. This may, perhaps, be better understood by considering the Table 66.7. As for a person who is pricing up the requested option, Table 66.8 should be used:

In dealing with options, there are two main means for counterparties to enter into a transaction: live pricing or volatile pricing/quotation.

What does a "live price" mean? The price of an option is obviously dependent on the spot price in the market. As an option trader needs to delta hedge the option straightaway, the spot at which the trader can hedge is the rate the trader uses to price the option. If a price is being quoted live, it means that the person asking for the price will be quoted a premium price for the option and the option trader will take the risk that spot moves during the transaction.

The alternative to dealing live is to deal "with delta." This means that the person asking the price will deal the delta hedge with the option trader as well as the option.

The premium is normally quoted as a percentage of the base currency amount of the option. However, in the interbank market, it is normally quoted as pips per currency amount of the option. For example, if the option is a dollar/Swiss franc option, the premium can be quoted in the following ways:

Percentage of the dollar amount of the option.

Percentage of the Swiss franc amount of the option.

Swiss franc pips per dollar amount of the option.

Dollar pips per Swiss franc amount of the option.

If the option were being dealt in a round amount of dollars (e.g., $10 million), then either 1 or 3 would be the usual quote. If 2 or 4 were required, however, the Swiss franc amount of the option is found by multiplying the dollar amount by the strike of the option.

How can one form of premium be quoted to another? The following formula can be used:

| BC = base currency (commodity currency) |

| NBC = nonbase currency (terms currency) |

| % BC = % NBC × strike/spot |

| % NBC = % BC × spot/strike |

| NBC/BC = % NBC × strike |

| BC/NBC = % BC/strike |

For example, if a Swiss franc dollar option costs 2.05% dollar amount, spot is 1.5500 and the strike of the option is 1.5200, then

| Swiss franc/dollar = 0.0205 × 1.5500 = 0.031775 |

or

| 318 Swiss franc pips per dollar |

When an option is exercised, the physical exchange of the two currencies is effected and normally, settlement takes place in full; for example, if a dollar put (right to sell) Swiss franc call (right to buy) option is exercised, the full amount of the dollars will be paid to the option writer and the exerciser will receive the full amount of Swiss francs from the option writer. As mentioned before, settlement takes place on the delivery date unless the option is American and has been exercised early, in which case settlement takes place spot from the date the option is exercised.

Is it necessary to settle both amounts in full? No, it is possible to "net settle" the option. This means that only the profit on the option is paid from the writer to the holder of the option. If this is decided at the time of exercise, the writer will normally quote the holder a spot rate and if this rate is acceptable, the option profit will be determined accordingly. If net settlement is agreed at the time of the original deal, it may be necessary to have a more formal arrangement for determining the profit on the option at the time of exercise.

It is sufficient that the option writer receives notice of exercise before the exercise time on the expiry date. This time is 15.00 hours London time, 15.00 hours Tokyo or 10.00 hours New York time.

It is important to note that there is a significant difference between the expectations and the risks assumed by the three main different players in the currency options market. The first group—investors—typically look to use options in order to improve the risk/rewards ratio compared with entering a spot foreign exchange transaction. As such, the investor is concerned with the total cost of the option from which it can be determined by how far the market must move in order to profit. Therefore, the primary interest is usually on the delta, or magnitude of the position, and how moves in the market will impact their daily profits and losses. The volatility level is of lesser concern.

The second group—hedgers—are primarily concerned with protecting an existing exposure from adverse movements in the currency market. Often, these corporate treasuries are hedging profits from overseas offices or costs from international purchases. Performance is compared with benchmark foreign exchange rates or cost effective levels. In the past, such risks were generally hedged in the forward foreign exchange market, locking in acceptable rates without any potential for profit. Options now provide the protection required while offering opportunities to profit from beneficial movements in the foreign exchange rate.

Third, volatility traders, for example banks and other professional players, have sufficient capital to perform the important task of establishing competitive and liquid markets in currency options for the users mentioned. As such, the options trader may hold hundreds of open options positions. The primary risk being managed is of movements in the price of volatility, and the relationship between the time decay and the gamma positions.

As the market for currency options has expanded, the number of speculators in the volatility markets has also increased. Before computer systems were widely available to manage the complex and dynamic risks of an option portfolio, profits in the market were primarily transaction oriented, with most of the risk eventually falling into the hands of a small number of institutions. However, there are now many market participants who are willing to assume risk positions and there is a broad spectrum of players ranging from a pure market maker with little risk to a pure position taker making use of the available liquidity.

Also, the following risks should be taken note of:

Credit risk. In selling an option to a client, there is no real credit risk if the option expires worthless (that is, it is not exercised). There is a transaction related risk if it is exercised, which is similar to risk on a spot settlement thus requiring a credit line to be in place in advance of the transaction. The client pays an up-front premium.

Market price risk. Because an option buyer enjoys the dual benefits of insurance and upside potential, the option writer is subject to a greater amount of market/price risk when it sells options than when it sells forward contracts. To compensate for this risk, the option writer charges the up-front premium.

Country risk. Similar to that for forwards and swaps.

The currency turmoil seen in recent years, together with increasingly global and competitive markets, have added to the difficulties faced by most participants of the foreign exchange markets in managing foreign exchange risk. Thus, demand for effective risk management instruments has grown dramatically in recent years.

Market participants have found that currency options allow them opportunities to capitalize on favorable exchange rate movements while providing protection from adverse movements. With competitors within the market equally able to neutralize risk without sacrificing the opportunities to be found in favorable markets, today's risk managers are finding that the advantages of currency options cannot be ignored.

Market participants who hedge with options range from the simplest one-person treasury to the "ultra-sophisticated" profit-oriented dealing room. All realize that the foreign exchange market can be too volatile to remain exposed and yet business may be too competitive to sacrifice opportunity. Thus, many financial organizations have responded to this need and have been extremely active in designing option strategies and products to meet various client needs. New and exotic option products are constantly being developed, enabling market providers to tailor option strategies to individual business or investment requirements.

The key advantage of using options for hedging, trading, or investment purposes is the flexibility that they provide. Options allow their users to put a value on risk, which is an important aid in the process of making decisions on risk portfolio management. Flexibility is also a feature in terms of the number of currency pairs and the maturities available in the market today.

The basis principle of an option is a simple one. The holder has the right (but not the obligation) to transact, and the writer has an obligation to transact should the holder wish to exercise. More complex option combinations and exotic options are based on these fundamental principles. The risk/reward implications of different option strategies are clearly definable.

In today's environment, individual risk appetites, market views and hedging objectives differ greatly. At the same time, there is a vast array of option structures and exotic option products available, which could be applied to any risk portfolio situation. In order for options to be integrated effectively, expectations, cost and risk mitigation priorities have to be kept in mind.

As the global market expands, so does the demand for options, not only in the major currency pairs of the world, but also in the more exotic currencies, especially as liquidity comes into those currencies in the spot and forward markets.

Black, E, and Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy 81, 3: 637-654.

DeRosa, D. E (2004). Currency Derivatives: Pricing Theory, Exotic Options, and Hedging Applications. Hobo-ken, NJ: John Wiley & Sons.

Graham, A. (2001). Currency Options. UK: Routledge.

Graham, J., and Lentz, S. (2003). Simple Steps to Option Trading Success. New York: Marketplace Books.

Hicks, A. (1998). Foreign Exchange Options, 2nd edition. UK: Woodhead Publishing.

Merton, R. C. (1973). Theory of rational option pricing. Bell Journal of Economics and Management Science 4, 1: 141-183.

Shamah, S. (2003). A Foreign Exchange Primer. West Essex, UK: John Wiley & Sons.

Shamah S. (2004) A Currency Options Primer. West Essex, UK: John Wiley & Sons.

Taylor, E (2004). Managing Foreign Exchange and Currency Options: A Practical Guide in the New Marketplace, 2nd edition. UK: FT Press.