FRANK J. FABOZZI, PhD, CFA, CPA

Professor in the Practice of Finance, Yale School of Management

STEVEN V. MANN, PhD

Professor of Finance, Moore School of Business, University of South Carolina

Abstract: Interest rate derivatives include interest rate futures, forward rate agreements, interest rate swaps, interest rate options, and interest rate caps and floors. Interest rate derivatives can be used to control the interest rate risk of a portfolio or financial institution, to speculate on the future level of interest rates or the change in the shape of the yield curve, or to hedge future borrowing costs. These instruments can be either exchange traded or traded in the over-the-counter market. Interest rate futures are exchange-traded; options can be exchange traded or traded in the over-the-counter market, so-called dealer options. The other interest rate derivatives are traded in the over-the-counter market. Exchange-traded futures on interest rates are classified by the maturity of the underlying interest rate: short-term contracts (Eurodollar futures, Fed funds futures) and long-term contracts (Treasury bond and note futures, swap futures, and municipal bond futures). A forward rate agreement is an over-the-counter derivative instrument which is essentially a forward-starting loan, but with no exchange of principal, so the cash exchanged between the counterparties depend only on the difference in interest rates.

Keywords: derivatives, notional amount, Eurodollar futures, Fed funds futures, Treasury bond futures, Treasury note futures contract, cheapest-to-deliver issue, delivery options, quality or swap option, timing option, wildcard option, swap futures contract, municipal bond futures, forward rate agreement

Derivatives are used by portfolio managers, traders, and corporate treasurers to manage and control risk. There is an array of interest rate derivatives that are used for managing and controlling interest rate risk. As with other derivatives, the instruments can be traded on an exchange or in the over-the-counter market. In this chapter we describe interest rate futures contracts and forward rate agreements. Interest rate swaps, options, caps, and floors are described elsewhere in other chapters.

We begin by discussing interest rate futures contracts. Interest rate futures contracts can be classified by the maturity of their underlying instrument. Short-term interest rate futures contracts have an underlying instrument that matures in one year or less and we discuss these first. We then discuss long-term interest rate futures, contracts where the underlying instrument exceeds one year. Finally, we describe forward rate agreements.

The more actively traded short-term interest futures contracts in the United States are described below.

A Eurodollar futures contract represents a commitment to pay/receive a quarterly interest payment determined by the level of 3-month LIBOR and a notional principal of $1 million on the settlement date. There are Eurodollar futures contracts available to trade with quarterly settlement dates (March, June, September, December) that extend out 10 years. Accordingly, it is possible for market participants to hedge or speculate on the level of 3-month LIBOR for the next decade. The contracts are settled in cash and trade on the Chicago Mercantile Exchange (CME) as well as the London International Financial Futures Exchange (LIFFE). The price of a Eurodollar futures contract is quoted as 100 minus the annualized futures 3-month LIBOR. For example, a Eurodollar futures price of 95 translates into a futures 3-month LIBOR of 5%.

The minimum price fluctuation (tick) for this contract is 0.005 or 1/2; basis point. This means that the tick value for this contract is $12.50, which is determined as follows:

The Eurodollar CD futures contract is used frequently to trade the short end of the yield curve and many hedgers believe this contract to be the best hedging vehicle for a wide range of hedging situations. Moreover, the markets for Eurodollar futures contracts and the interest rate swaps are tightly connected. In particular, the floating-rate payments of an interest rate swap can be derived from a portfolio of Eurodollar futures contracts whose expiration dates match the swap's floating-rate reset dates.

The 90-day sterling LIBOR (London Interbank Offered Rate) interest rate futures contract trades on the main London futures exchange, LIFFE. The contract is structured similarly to the Eurodollar futures contract described above. Prices are quoted as 100 minus the interest rate and the expiration months are March, June, September, and December. The contract size is £500,000. A tick is 0.01 or one basis point and the tick value is £12.5.

The LIFFE also trades short-term interest rate futures for other major currencies including euros, yen, and Swiss franc. Short-term interest rate futures contracts in other currencies are similar to the 90-day sterling LIBOR contract and trade on exchanges such as Deutsche Termin-bourse in Frankfurt and MATIF (Marché à Terme International de France) in Paris.

Depository institutions are required to hold reserves to meet their reserve requirements. To meet these requirements, depository institutions hold reserves at their district Federal Reserve Bank. These reserves are called federal funds. Because no interest is earned on federal funds, a depository institution that maintains federal funds in excess of the amount required incurs an opportunity cost of the interest forgone on the excess reserves. Conversely, there are also depository institutions whose federal funds are short of the amount required. The federal funds market is where depository institutions buy and sell federal funds to address this imbalance. The interest rate at which federal funds are bought (borrowed) and sold (lent) is called the federal funds rate. Consequently, the federal funds rate is a benchmark short-term interest rate.

When the Federal Reserve formulates and executes monetary policy, the federal funds rate is a primary operating target. The Federal Open Market Committee (FOMC) sets a target level for the federal funds rate. Announcements of changes in monetary policy specify changes in the FOMC's target for this rate. Once the target is set, the Federal Reserve either adds or drains reserves from the banking system using open market operations so that the actual federal funds rate is, on average, equal to the target. The 30-day federal funds futures contract is designed for financial institutions and businesses who want to control their exposure to movements in the federal funds rate.

The federal funds futures contract began trading on the Chicago Board of Trade (CBOT) in October 1988. These contracts have a notional amount of $5 million and the contract can be written for the current month up to 24 months in the future. Underlying this contract is the simple average overnight federal funds rate (that is, the effective rate) for the month. As such, this contract is settled in cash on the last business day of the month. Just as the other short-term interest rate futures contracts discussed above, prices are quoted on the basis of 100 minus the overnight federal funds rate for the expiration month. These contracts are market to market using the effective daily federal funds rate as reported by the Federal Reserve Bank of New York.

The most actively traded long-term (greater than one year) interest rate futures contracts are described below.

The Treasury bond futures contract is traded on the CBOT. The underlying instrument for this contract is $100,000 par value of a hypothetical 20-year coupon bond. This hypothetical bond's coupon rate is called the notional coupon. Currently, this notional coupon is 6%. Treasury futures contracts trade with March, June, September, and December settlement months.

The futures price is quoted in terms of par being 100. Published quotes have two parts namely the number of points (1% of par value) and the number of ticks (1/32 of 1% of par value). Thus, a quote for a Treasury bond futures contract of 97-16 means 97 and 163/2 or 97.50. So, if a buyer and seller agree on a futures price of 97-16, this means simply that the buyer agrees to accept delivery of the hypothetical underlying Treasury bond and pay 97.50% of par value and the seller agrees to accept 97.50% of par value. Since the par value of the bond underlying the futures contract is $100,000, the futures price that the buyer and seller agree to for this hypothetical bond is $97,500 plus accrued interest.

The minimum price fluctuation for the Treasury bond futures contract is 1/32 of 1% as noted previously which is referred to as a 32nd. The dollar value of a 32nd for $100,000 par value (the par value for the underlying Treasury bond) is $31.25. This is true because each point (1% of the par value) is worth $1,000 and each point is comprised of 32 ticks. Thus, the minimum price fluctuation is $31.25 for this contract.

We have been referring to the underlying instrument as a hypothetical Treasury bond. While some interest rate futures contracts can only be settled in cash, the seller (the short) of a Treasury bond futures contract who chooses to make delivery rather than liquidate his/her position by buying back the contract prior to the settlement date must deliver some Treasury bond. This begs the question "which Treasury bond?" The CBOT allows the seller to deliver one of several Treasury bonds that the CBOT specifies are acceptable for delivery. These contracts have multiple deliverables to avoid having a single issue squeezed and to allow for varying schedules of new issues. The term "squeeze" is used to describe a shortage of the supply of a particular security relative to the demand. A trader who is short a particular security is always concerned with the risk of being unable to obtain sufficient securities to cover their position.

The set of all bonds that meet the delivery requirements for a particular contract is called the deliverable basket. The CBOT makes its determination of the Treasury issues that are acceptable for delivery from all outstanding Treasury issues that have at least 15 years to maturity from the first day of the delivery month. For settlement purposes, the CBOT specifies that a given issue's term to maturity is calculated in complete three month increments (that is, complete quarters). For example, the actual maturity of the issue is 15 years and 5 months would be rounded down to a maturity of 15 years and 1 quarter (three months). Moreover, all bonds delivered by the seller must be of the same issue.

It is important to keep in mind that while the underlying Treasury bond for this contract is a hypothetical issue and therefore cannot itself be delivered into the futures contract, the bond futures contract is not a cash settlement contract. The only way to close out a Treasury bond futures contract is to either initiate an offsetting futures position or to deliver a Treasury issue from the deliverable basket.

Conversion Factors

The delivery process for the Treasury bond futures contract is innovative and has served as a model for government bond futures contracts traded on various exchanges throughout the world. On the settlement date, the seller of the futures contract (the short) is required to deliver the buyer (the long) $100,000 par value of a 6% 20-year Treasury bond. As noted, no such bond exists, so the seller must choose a bond from the deliverable basket to deliver to the long. Suppose the seller selects a 5% coupon, 20-year Treasury bond to settle the futures contract. Since the coupon of this bond is less than the notional coupon of 6%, this would be unacceptable to the buyer who contracted to receive a 6% coupon, 20-year bond with a par value of $100,000. Alternatively, suppose the seller is compelled to deliver a 7% coupon, 20-year bond. Since the coupon of this bond is greater than the notional coupon of 6%, the seller would find this unacceptable. In summary, how do we adjust for the fact that bonds in the deliverable basket have coupons and maturities that differ from the notional coupon of 6%?

To make delivery equitable to both parties, the CBOT uses conversion factors for adjusting the price of each Treasury issue that can be delivered to satisfy the Treasury bond futures contract. Within the deliverable basket, conversion factors are designed to make each bond approximately equally cheap to deliver if the yield curve were flat at 6%. The conversion factor is determined by the CBOT before a contract with a specific settlement date begins trading using the following formula:

where

| CF = conversion factor |

| N = complete years to maturity as of the settlement month |

| C = annual coupon rate (in decimal form) |

| K = number of months that the maturity exceeds N (rounded down to complete quarters) |

For example, if the maturity of a Treasury bond from the deliverable basket is 24 years and 4.5 months, K is 3 since the 4.5 months is rounded down to complete quarters, or 3 months. Further, if the maturity is 24 years and 11 months, K is 9.

The convention of rounding down to the nearest complete quarter adds a slight distortion into the calculation of the conversion factors. To see this, recall Treasury futures contracts have expiration months of March, June, September, and December. Also note that all Treasury bonds mature on February 15, May 15, August 15, or November 15. Since conversion factors are computed as of the first day of the delivery month, bonds that mature on say, August 15 are treated as if they mature on June 1 (the first delivery day of the June contract.) The Treasury's maturity is artificially shortened by 21/2 months so that there is 21/2 months of "pull to par" built into the conversion factors. As a result, for Treasury bonds with coupon rates below 6%, the conversion factors will be slightly higher than they should be. Conversely, for issues with coupon rates above 6%, the conversion factors will be slightly lower than they should be.

Table 39.1. Deliverable Basket for the December 2006 Treasury Bond Futures Contract

Coupon Rate | Maturity Date | Price | Conv. Factor | Implied Repo Rate |

|---|---|---|---|---|

The implied repo rates are obtained from Bloomberg | ||||

7.625 | 11/15/22 | 129-20 | 1.1640 | 5.09 |

7.25 | 8/15/22 | 125-08 | 1.1250 | 5.06 |

7.125 | 2/15/23 | 124-07+ | 1.1147 | 4.68 |

6.25 | 8/15/23 | 114-23+ | 1.0260 | 3.35 |

7.5 | 11/15/24 | 130-11 | 1.1623 | 2.80 |

7.625 | 2/15/25 | 132-02+ | 1.1774 | 2.70 |

6.875 | 8/15/25 | 123-15+ | 1.0970 | 1.44 |

6.75 | 8/15/26 | 122-21 | 1.0855 | 0.20 |

6.0 | 2/15/26 | 113-00+ | 1.0000 | −0.04 |

6.5 | 11/15/26 | 119-22 | 1.0573 | −0.39 |

6.625 | 2/15/27 | 121-15+ | 1.0722 | −0.68 |

6.375 | 8/15/27 | 118-18+ | 1.0439 | −1.53 |

6.125 | 11/15/27 | 115-15+ | 1.0146 | −2.18 |

5.5 | 8/15/28 | 107-17+ | 0.9400 | −3.98 |

6.125 | 8/15/29 | 116-10+ | 1.0153 | −4.26 |

5.25 | 11/15/28 | 104-10 | 0.9095 | −4.75 |

5.25 | 2/15/29 | 104-10+ | 0.9090 | −5.01 |

6.25 | 5/15/30 | 118-16+ | 1.0310 | −5.20 |

5.375 | 2/15/31 | 106-15 | 0.9210 | −7.16 |

4.5 | 2/15/36 | 94-06+ | 0.7950 | −14.76 |

Table 39.1 displays the conversion factors for each Treasury bond in the deliverable basket for the December 2006 Treasury bond futures contract. This information was obtained from Bloomberg. The conversion factors are reported in column 4. Note those bonds with coupon rates with coupon rates greater than 6% have conversion factors greater than one and those with coupon rates less than 6% have conversion factors less than one.

Given the conversion factor for an issue and the futures price, the adjusted price is found by multiplying the conversion factor by the futures price. The adjusted price is called the converted price.

The price that the buyer must pay the seller when a Treasury bond is delivered is called the invoice price. Intuitively, the invoice price should be the futures settlement price plus accrued interest. However, as just noted, the seller can choose any Treasury issue from the deliverable basket. To make delivery fair to both parties, the invoice price must be adjusted using the conversion factor of the actual Treasury issue delivered. The invoice price is:

Suppose the settlement price of the 111-04 Treasury bond futures contract is 11/15/22 and the issue selected by short to deliver is the coupon bond that matures on 111-04. The futures contract settlement price of 1.1640 means 111.125% of par value or times par value. The conversion factor for this issue is 1.11125. Since the contract size is $100,000, the invoice price the buyer pays the seller is:

Cheapest-to-Deliver Issue

In selecting the issue to be delivered, the short will select from all the deliverable issues the one that will give the largest rate of return from a cash-and-carry trade. A cash-and-carry-trade is one in which a cash bond that is acceptable for delivery is purchased with borrowed funds and simultaneously the Treasury bond futures contract is sold. The bond purchased can be delivered to satisfy the short futures position. Thus, by buying the Treasury issue that is acceptable for delivery and selling the futures, an investor has effectively sold the bond at the delivery price (that is, the converted price).

A rate of return can be calculated for this trade. This rate of return is referred to as the implied repo rate and is determined by:

The price plus accrued interest at which the Treasury issue could be purchased.

The converted price plus the accrued interest that will be received upon delivery of that Treasury bond issue to satisfy the short futures position.

The coupon payments that will be received between today and the date the issue is delivered to satisfy the futures contract.

The reinvestment income that will be realized on the coupon payments between the time the interim coupon payment is received and the date that the issue is delivered to satisfy the Treasury bond futures contract.

The first three elements are known. The last element will depend on the reinvestment rate that can be earned. While the reinvestment rate is unknown, typically this is a small part of the rate of return and not much is lost by assuming that the implied repo rate can be predicted with certainty.

The general formula for the implied repo rate is as follows:

where Days1 is equal to the number of days until settlement of the futures contract. Below we will explain the other components in the formula for the implied repo rate.

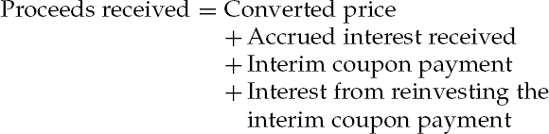

Let's begin with the dollar return. The dollar return for an issue is the difference between the proceeds received and the cost of the investment. The proceeds received are equal to the proceeds received at the settlement date of the futures contract and any interim coupon payment plus interest from reinvesting the interim coupon payment. The proceeds received at the settlement date include the converted price (that is, futures settlement price multiplied by the conversion factor for the issue) and the accrued interest received from delivery of the issue. That is,

As noted earlier, all of the elements are known except the interest from reinvesting the interim coupon payment. This amount is estimated by assuming that the coupon payment can be reinvested at the term repo rate. The repo rate is not only a borrowing rate for an investor who wants to borrow in the repo market but also the rate at which an investor can invest proceeds on a short-term basis. For how long is the reinvestment of the interim coupon payment? It is the number of days from when the interim coupon payment is received and the actual delivery date to satisfy the futures contract. The reinvestment income is then computed as follows:

where Days2 is the number of days between when the interim coupon payment is received and the actual delivery date of the futures contract.

The reason for dividing Days2 by 360 is that the ratio represents the number of days the interim coupon is reinvested as a percentage of the number of days in a year as measured in the money market.

The cost of the investment is the amount paid to purchase the issue. This cost is equal to the purchase price plus accrued interest paid. That is,

Thus, the dollar return for the numerator of the formula for the implied repo rate is equal to

Note that in practice, the cost of the investment should be adjusted because the amount that the investor ties up in the investment is reduced if there is an interim coupon payment. We ignore this adjustment here.

The dollar return is then divided by the cost of the investment.

So, now we know how to compute the numerator and the denominator in the formula for the implied repo rate. The second ratio in the formula for the implied repo rate simply involves annualizing the return using a convention in the money market for the number of days. (The money market convention is to use a 360-day year.) Since the investment resulting from the cash-and-carry trade is a synthetic money market instrument, 360 days are used.

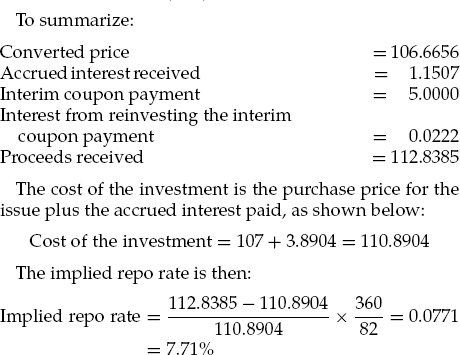

Let's compute the implied repo rate for a hypothetical issue that may be delivered to satisfy a hypothetical Treasury bond futures contract. Assume the following for the deliverable issue and the futures contract:

Futures contract:

| Futures price = 96 |

| Days to futures delivery date (Daysi) = 82 days |

Deliverable issue:

| Price of issue = 107 |

| Accrued interest paid = $3.8904 |

| Coupon rate = 10% |

| Days remaining before interim coupon paid = 40 days |

| Interim coupon = $5 |

| Number of days between when the interim coupon payment is received and the actual delivery date of the futures contract (days2) = 42 |

| Conversion factor = 1.1111 |

| Accrued interest received at futures settlement date = 1.1507 |

Other information:

82-day term repo rate = 3.8%

Let's begin with the proceeds received. We need to compute the converted price and the interest from reinvesting the interim coupon payment. The converted price is:

The interest from reinvesting the interim coupon payment depends on the term repo rate. The term repo rate is assumed to be 3.8%. Therefore,

Interest from reinvesting the interim coupon payment

Once the implied repo rate is calculated for each bond in the deliverable basket, the issue selected will be the one that has the highest implied repo rate (that is, the issue that gives the maximum return in a cash-and-carry trade). The issue with the highest return is referred to as the cheapest-to-deliver issue. This issue plays a key role in the pricing of a Treasury futures contract.

While a particular Treasury bond may be the cheapest to deliver today, changes in interest rates, for example, may cause some other issue to be the cheapest to deliver at a future date. A sensitivity analysis can be performed to determine how a change in yield affects the cheapest to deliver bond. In particular, the sensitivity analysis identifies which bond in the deliverable basket is cheapest to deliver following various shocks to the yield curve.

Other Delivery Options

In addition to the choice of which acceptable Treasury issue to deliver—sometimes referred to as the quality option or swap option—the short has at least two more options granted under CBOT delivery guidelines. The short is permitted to decide when in the delivery month, delivery actually will take place. This is called the timing option. The other option is the right of the short to give notice of intent to deliver up to 8:00 P.M. Chicago time after the closing of the exchange (3:15 P.M. Chicago time) on the date when the futures settlement price has been fixed. This option is referred to as the wildcard option. The quality option, the timing option, and the wildcard option (in sum referred to as the delivery options), mean that the long position can never be sure which Treasury bond issue will be delivered or when it will be delivered. These three delivery options are summarized below:

Delivery Option | Description |

|---|---|

Quality or swap option | Choice of which acceptable Treasury issue to deliver |

Timing option | Choice of when in delivery month to deliver |

Wild card option | Choice to deliver after the closing price of the futures contract is determined |

Delivery Procedure

For a short who wants to deliver, the delivery procedure involves three days. The first day is the position day. On this day, the short notifies the CBOT that it intends to deliver. The short has until 8:00 P.M. central standard time to do so. The second day is the notice day. On this day, the short specifies which particular issue will be delivered. The short has until 2:00 P.M. central standard time to make this declaration. (On the last possible notice day in the delivery month, the short has until 3:00 P.M.) The CBOT then selects the long to whom delivery will be made. This is the long position that has been outstanding for the longest period of time. The long is then notified by 4:00 P.M. that delivery will be made. The third day is the delivery day. By 10:00 A.M. on this day the short must have in its account the Treasury issue that it specified on the notice day and by 1:00 P.M. must deliver that bond to the long that was assigned by the CBOT to accept delivery. The long pays the short the invoice price upon receipt of the bond.

Treasury Note Futures

There are three Treasury note futures contracts: 10-year, 5-year, and 2-year. All three contracts are modeled after the Treasury bond futures contract and are traded on the CBOT. The underlying instrument for the 10-year Treasury note contract is $100,000 par value of a hypothetical 10-year 6% Treasury note. There are several acceptable issues that may be delivered by the short. An issue is acceptable if the maturity is not less than 6.5 years and not greater than 10 years from the first day of the delivery month. The delivery options granted to the short position and the minimum price fluctuation are the same as for the Treasury bond futures contract.

For the 5-year Treasury note futures contract, the underlying instrument is $100,000 par value of a 6% notional coupon Treasury note. An issue in the deliverable basket must satisfy the following conditions: (1) an original maturity of not more than five years and three months; (2) a remaining maturity of not more than five years and three months; and (3) a remaining maturity not less than four years and two months. The minimum price fluctuation for this contract is 1/64 of 1% of par. The dollar value of a 64th for a $100,000 par value is $15,625 ($100,000/6,400) and is therefore the minimum price fluctuation.

The underlying instrument for the 2-year Treasury note futures contract is $200,000 par value of a 6% notional coupon Treasury note. Issues acceptable for delivery must have a remaining maturity of not more than two years and not less than one year and nine months. Moreover, the original maturity of the note in the deliverable basket cannot be more than five years and three months. The minimum price fluctuation for this contract is 1/128 of 1% of par value. The dollar value of a 128th for a $200,000 par value is $15,625 ($100,000/12,800) and is therefore the minimum price fluctuation.

An interest rate swap contract is an instrument used by market participants to transform the nature of cash flows and the interest rate exposure of a portfolio or balance sheet. The contract is an agreement between two counterparties to exchange periodic interest payments. In the most common and simplest form, one party agrees to pay the other party fixed interest payments at designated dates for the life of the contract. The other party in return agrees to make interest rate payments that float with some reference rate. When quoting swaps levels in the market, the convention is for the dealer to set the floating rate equal to the reference rate (usually LIBOR) and then quote the fixed rate (called the swap rate) that will apply.

The CBOT introduced a swap futures contract in late October 2001. The underlying instrument is the notional price of the fixed-rate side of a 10-year interest rate swap that has a notional principal equal to $100,000 and that exchanges semiannual interest payments at a fixed annual rate of 6% for floating interest rate payments based on 3-month LIBOR. Interest rate swaps are discussed in Chapter 40 of Volume I. This swap futures contract is cash-settled with a settlement price determined by the ISDA benchmark 10-year swap rate on the last day of trading before the contract expires. This benchmark rate is published with a one-day lag in the Federal Reserve Board's statistical release H.15. Contracts have settlement months of March, June, September, and December just like the other CBOT interest rate futures contracts that we have discussed.

The LIFFE introduced the first swap futures contract called Swapnote®, which is referenced to the euro interest rate swap curve. Swapnotes are available in 2-, 5-, and 10-year maturities. The CME also lists a swap futures contract with maturities of 2,5, and 10 years that is similar to those listed on the CBOT.

A 10-year municipal note index futures contract is traded on the CBOT. The underlying for this contract is an index. The index includes between 100 and 250 high-grade tax-exempt securities. For an issue to be eligible for inclusion in the index, the issuer

must have a triple A credit rating assigned by both S&P and Moody's

must have a principal size of at least $50 million

must be a component (that is, tranche) of a municipal issue with a total deal size of at least $200 million

must have a remaining maturity of between 10 and 40 years from the first calendar day of the corresponding futures contract expiration

must at issuance have a price of at least 90

must pay semiannual interest at a fixed coupon rate that ranges from 3% to 9%

An issue can be callable or noncallable. However, if an issue is callable, it must have a first call date at least seven years from the first calendar day of the corresponding futures contract expiration. The issues comprising the index insured and uninsured bonds.

In constructing the index, there are three further restrictions: (1) no more than 5% of the bond in the index can be from any one issuer, (2) no more than 15% can be from any one state or U.S. territory, and (3) no more than 40% of the issues can be insured by any one issuer.

To assure that the index continues to accurately mirror the overall tax-exempt market, it is revised quarterly on the first business day of each February, May, August, and November. When the index is revised, issues that no longer meet the selection criteria explained above will are eliminated from the index.

Each day the index is priced. Because the issues comprising the index do not typically trade each day, an independent pricing service, FT Interactive Data Corporation, provides prices for the individual issues and then calculates computes the closing value of the index. At the settlement date, the parties settle in cash. Settlement is based on the final settlement value based on the value of the index as determined by FT Interactive Data Corporation. The final settlement price is calculated as follows:

where r is equal to the simple average yield-to-worst of the component bonds in the index for the last day of trading, expressed in percent terms and calculated to the nearest 1/10 of a basis point (e.g., 4.85%).

A forward rate agreement (FRA) is an over-the-counter derivative instrument that trades as part of the money market. In essence, an FRA is a forward-starting loan, but with no exchange of principal, so the cash exchanged between the counterparties depend only on the difference in interest rates. While the FRA market is truly global, most business is transacted in London. Trading in FRAs began in the early 1980s and the market now is large and liquid.

In effect an FRA is a forward dated loan, transacted at a fixed rate, but with no exchange of principal—only the interest applicable on the notional amount between the rate agreed to when the contract is established and the actual rate prevailing at the time of settlement changes hands. For this reason, FRAs are off-balance sheet instruments. By trading today at an interest rate that is effective at some point in the future, FRAs enable banks and corporations to hedge forward interest rate exposure.

An FRA is an agreement to borrow or lend a notional cash sum for a period of time lasting up to 12 months, starting at any point over the next 12 months, at an agreed rate of interest (the FRA rate). The "buyer" of a FRA is borrowing a notional sum of money while the "seller" is lending this cash sum. Note how this differs from all other money market instruments. In the cash market, the party buying a CD, Treasury bill, or bidding for bond in the repo market, is the lender of funds. In the FRA market, to "buy" is to "borrow." Of course, we use the term "notional" because with an FRA no borrowing or lending of cash actually takes place. The notional sum is simply the amount on which the interest payment is calculated (that is, a scale factor).

Accordingly, when a FRA is traded, the buyer is borrowing (and the seller is lending) a specified notional sum at a fixed rate of interest for a specified period, the "loan" to commence at an agreed date in the future. The buyer is the notional borrower, and so if there is a rise in interest rates between the date that the FRA is traded and the date that the FRA comes into effect, she will be protected. If there is a fall in interest rates, the buyer must pay the difference between the rate at which the FRA was traded and the actual rate, as a percentage of the notional sum.

The buyer may be using the FRA to hedge an actual exposure, that is an actual borrowing of money, or simply speculating on a rise in interest rates. The counterparty to the transaction, the seller of the FRA, is the notional lender of funds, and has fixed the rate for lending funds. If there is a fall in interest rates, the seller will gain, and if there is a rise in rates, the seller will pay. Again, the seller may have an actual loan of cash to hedge or is acting as a speculator.

In FRA trading, only the payment that arises because of the difference in interest rates changes hands. There is no exchange of cash at the time of the trade. The cash payment that does arise is the difference in interest rates between that at which the FRA was traded and the actual rate prevailing when the FRA matures, as a percentage of the notional amount. FRAs are traded by both banks and corporations. The FRA market is liquid in all major currencies and rates are readily quoted on screens by both banks and brokers.

The terminology quoting FRAs refers to the borrowing time period and the time at which the FRA comes into effect (or matures). Hence, if a buyer of a FRA wished to hedge against a rise in rates to cover a 3-month loan starting in three months' time, she would transact a "3-against-6 month" FRA, or more usually denoted as a 3×6 or 3v6 FRA. This is referred to in the market as a "three-sixes" FRA, and means a 3-month loan beginning in three months' time. So correspondingly, a "ones-fours" FRA (lv4) is a 3-month loan in one month's time, and a "three-nines" FRA (3v9) is a 6-month loan in three months' time.

As an illustration, suppose a corporation anticipates it will need to borrow in 6 months time for a 6-month period. It can borrow today at 6-month LIBOR plus 50 basis points. Assume that 6-month LIBOR rates are 4.0425% but the corporation's treasurer expects rates to go up to about 4.50% over the next several weeks. If the treasurer's suspicion is correct, the corporation will be forced to borrow at higher rates unless some sort of hedge is put in place to protect the borrowing requirement. The treasurer elects to buy a 6vl2 FRA to cover the 6-month period beginning six months from now. A bank quotes 4.3105% for the FRA, which the corporation buys for a £1,000,000 notional principal. Suppose that 6 months from now, 6-month LIBOR has indeed backed-up to 4.50%, so the treasurer must borrow funds at 5% (LIBOR plus the 50-basis-point spread). However, offsetting this rise in rates, the corporation will receive a settlement amount which will be the difference between the rate at which the FRA was bought (4.3105%) and today's 6-month LIBOR rate (4.50%) as a percentage of the notional principal of £1 million. This payment will compensate for some of the increased borrowing costs.

In virtually every market, FRAs trade under a set of terms and conventions that are identical. The British Bankers Association (BBA) has compiled standard legal documentation to cover FRA trading. The following standard terms are used in the market:

Notional sum: The amount for which the FRA is traded.

Trade date: The date on which the FRA is transacted.

Settlement date: The date on which the notional loan or deposit of funds becomes effective, that is, is said to begin. This date is used, in conjunction with the notional sum, for calculation purposes only as no actual loan or deposit takes place.

Fixing date: This is the date on which the reference rate is determined, that is, the rate to which the FRA rate is compared.

Maturity date: The date on which the notional loan or deposit expires.

Contract period: The time between the settlement date and maturity date.

FRA rate: The interest rate at which the FRA is traded.

Reference rate: This is the rate used as part of the calculation of the settlement amount, usually the LIBOR rate on the fixing date for the contract period in question.

Settlement sum: The amount calculated as the difference between the FRA rate and the reference rate as a percentage of the notional sum, paid by one party to the other on the settlement date.

These key dates are illustrated in Figure 39.1.

The spot date is usually two business days after the trade date, however it can by agreement be sooner or later than this. The settlement date will be the time period after the spot date referred to by the FRA terms: for example, a 1 × 4 FRA will have a settlement date one calendar month after the spot date. The fixing date is usually two business days before the settlement date. The settlement sum is paid on the settlement date, and as it refers to an amount over a period of time that is paid up front (that is, at the start of the contract period), the calculated sum is a discounted present value. This is because a normal payment of interest on a loan/deposit is paid at the end of the time period to which it relates; because an FRA makes this payment at the start of the relevant period, the settlement amount is a discounted present value sum. With most FRA trades, the reference rate is the level of LIBOR on the fixing date.

The settlement sum is calculated after the fixing date, for payment on the settlement date. We can illustrate this with a hypothetical example. Consider a case where a corporation has bought £1 million notional sum of a 1×4 FRA, and transacted at 5.75%, and that the market rate is 6.50% on the fixing date. The contract period is 90 days. In the cash market the extra interest charge that the corporate would pay is a simple interest calculation, and is:

Note that in the U.S. money market, a 360-day year is assumed rather than the 365 day year used in the U.K. money market.

This extra interest that the corporation is facing would be payable with the interest payment for the loan, which (as it is a money market loan) is paid when the loan matures. Under a FRA then, the settlement sum payable should, if it was paid on the same day as the cash market interest charge, be exactly equal to this. This would make it a perfect hedge. As we noted above though, FRA settlement value is paid at the start of the contract period, that is, the beginning of the underlying loan and not the end. Therefore, the settlement sum has to be adjusted to account for this, and the amount of the adjustment is the value of the interest that would be earned if the unadjusted cash value were invested for the contract period in the money market. The settlement value is given by the following expression:

where

| rref =the reference interest fixing rate |

| rFRA =the FRA rate or contract rate |

| M=the notional value sum |

| n=the number of days in the contract period |

| B=the day-count basis (360 or 365) |

The expression for the settlement value above simply calculates the extra interest payable in the cash market, resulting from the difference between the two interest rates, and then discounts the amount because it is payable at the start of the period and not, as would happen in the cash market, at the end of the period.

In our hypothetical illustration, as the fixing rate is higher than the contract rate, the buyer of the FRA receives the settlement sum from the seller. This payment compensates the buyer for the higher borrowing costs that they would have to pay in the cash market. If the fixing rate had been lower than 5.75%, the buyer would pay the difference to the seller, because the cash market rates will mean that they are subject to a lower interest rate in the cash market. What the FRA has done is hedge the interest rate exposure, so that whatever happens in the market, the buyer will pay 5.75% on its borrowing.

A market maker in FRAs is trading short-term interest rates. The settlement sum is the value of the FRA. The concept is exactly as with trading short-term interest-rate futures; a trader who buys a FRA is running a long position, so that if on the fixing date the reference rate is greater than the contract rate then the settlement sum is positive and the trader realizes a profit. What has happened is that the trader, by buying the FRA, "borrowed" money at the FRA rate, which subsequently rose. This is a gain, exactly like a short position in an interest rate futures contract, where if the price goes down (that is, interest rates go up), the trader realizes a gain. Conversely, a "short" position in an FRA that is accomplished by selling a FRA realizes a gain if on the fixing date the reference rate is less than the FRA rate.

Interest rate derivatives are employed by market participants to manage and control interest rate risk. This chapter included a discussion of interest rate futures and forward rate agreements. Short-term interest rate futures are used to manage and control interest rate risk due to movements in short-term (less than one year) interest rates. Eurodollar futures contracts are among the most heavily traded contracts in the world. It is a cash settlement contract with an underlying instrument of three-month LIBOR. The federal funds futures contract allows users to control their exposure the federal funds rate.

Actively traded long-term (longer than one year) interest futures contracts include Treasury bond/note futures contract, swap futures contracts of various maturities, and the 10-year municipal note index futures contract. The underlying instrument of the Treasury bond futures contract is a notional 6% coupon, 20-year bond. Conversion factors are used to adjust the invoice price of a Treasury bond futures contract to delivery equitable to both parties. The short position has several embedded delivery options which include the following: quality, timing and wild card options. Treasury note futures contracts of 2-, 5-, and 10-years are modeled after the Treasury note futures contract.

The underlying instrument for a swap futures contract is the notional price of the fixed-rate side of a 10-year interest rate swap that has a notional principal equal to $100,000 and that exchanges semi-annual interest payments at a fixed annual rate of 6% for floating interest rate payments based on 3-month LIBOR.

The underlying for the 10-year municipal note index futures contract are 100 to 250 high-grade tax-exempt securities. The contract is a cash settlement contract.

A forward rate agreement is an over-the-counter derivative instrument which is essentially a forward-starting loan, but with no exchange of principal, so the cash exchanged between the counterparties depend only on the difference in interest rates.

The elements of an FRA are the FRA rate, reference rate, notional amount, contract period, and settlement date. The buyer of an FRA is agreeing to pay the FRA rate and the seller of the FRA is agreeing to receive the FRA rate. The amount that must be exchanged at the settlement date is the present value of the interest differential. In contrast to an interest rate futures contract, the buyer of an FRA benefits if the reference rate increases and the seller benefits if the reference rate decreases.

Chance, D. M., and Brooks, R. (2007). Introduction to Derivatives and Risk Management, 7th edition. Mason, OH: Thomson South-Western.

Fabozzi, F. J., Mann, S. V., and Choudhry, M. (2003). Measuring and Controlling Interest Rate and Credit Risk, 2nd edition. Hoboken, NJ: John Wiley & Sons.

Hull, J. (1997). Introduction to Futures and Options Markets, 3rd edition. Englewood Cliffs, NJ: Prentice Hall.

Hull, J. (2006). Options, Futures, and Other Derivative Securities. Upper Saddle River, NJ: Prentice Hall.

Kolb, W, and Overdahl, J. A. (2006). Understanding Futures Markets. New York: Blackwell.

Pitts, M., and Fabozzi, F. J. (1990). Interest Rate Futures and Options, Chicago: Probus Publishing.