REBECCA J. MANNING

Vice President, Harbor Asset Management

DOUGLAS J. LUCAS

Executive Director and Head of CDO Research, UBS

LAURIE S. GOODMAN, PhD

Co-head of Global Fixed Income Research Manager of U.S. Securitized Products Research, UBS

FRANK J. FABOZZI PhD, CFA, CPA

Professor in the Practice of Finance, Yale School of Management

Abstract: Commercial real estate is a cyclical industry, subject to local, regional, and national economic conditions. It is also a capital intensive business, requiring funding for initial development as well ongoing maintenance and improvements. Consequently, commercial real estate finance has traditionally been dominated by banks, life insurance companies and private investors with the long-term investment horizons and the access to capital required by the industry. However, commercial real estate finance has evolved into a public market with more liquidity and transparency, which has attracted a broader range of investors. In addition, commercial real estate-related investments have become more complex, bringing new opportunities and new risks to investors.

Keywords: commercial real estate loans, whole loans, A-notes, B-notes, mezzanine loans, commercial mortgage-backed securities (CMBS), REIT securities, loan origination, master servicer, special servicer, call protection mechanisms, prepayment risk, extension risk, interest shortfalls

A commercial real estate loan is secured by a commercial real estate property, such as an office building or by an interest in the entity that owns the property. The principal and interest on the loan are generally paid from cash flows generated by the property. Real estate borrowers, or sponsors, will take out loans to purchase properties, refinance existing debt, or add on to an existing loan.

Over the years, commercial real estate finance has evolved from simple first-lien mortgage loans on commercial real estate properties to a variety of different types of loans and real estate-related securities. The most common real estate loans and securities in the market today include:

Commercial real estate loans

Whole loans and A-notes

B-notes

Mezzanine loans

Preferred equity

Commercial mortgage-backed securities

REIT securities

While all of these investments are on some level supported by real estate properties, their risks are considerably different, depending not only on the type of loan or security, but also on the underlying property type, geographic location, and tenant concentration, to name a few differences.

In this chapter, we explain different types of commercial real estate (CRE) loans and securities, analyzing the structures, investment considerations, and the risks of CRE loans and CMBS and REIT securities. (For a discussion of the historical performance of commercial real estate loans and CMBS, see Chapter 9 in Lucas, Goodman, Fabozzi, and Manning [2007].)

To obtain a loan on a commercial property, a sponsor typically turns to a commercial loan originator. Originators include commercial banks, insurance companies, real estate investment trusts (REITs), commercial mortgage-backed security (CMBS) conduits, and CRE collateralized debt obligations (CDOs). Originators may keep the loans for their own portfolios, or sell the loans in the secondary market. Others, particularly CMBS conduits, may also serve as warehouses, collecting a pool of loans, often referred to as "conduit loans," to later be securitized as CMBS.

Loan originators underwrite loans and determine the appropriate loan structure and terms based on the results of their due diligence. The performance of the loan is often related to the quality of the underwriting done by the originator. In fact, rating agencies will look at the performance history of the loans underwritten by the originator when assigning a rating to a new loan.

Many of the loans originated today are pooled to create CMBS. CMBS issuers perform their own due diligence on each loan in the pool. In addition, they look at the pool on an aggregate basis, assessing portfolio risks such as concentrations of property type, geography, and loans. The pool of loans is then tranched into individual securities and sold to third-party investors. We discuss CMBS later in this chapter.

An originator's due diligence includes verifying a property's value, cash flow, and credit quality. Originators typically require and review:

Current property appraisals.

Current leases and rent rolls.

Tax filings and bank statements.

Tenant credit quality.

Site inspections.

Environmental and engineering reports from reputable firms.

Title insurance and other legal property documents.

Lockbox provisions requiring that all revenues generated by the property be collected by a trustee, who first pays all operating expenses, debt service, and any other expenses. Excess cash flow is then distributed to the sponsor.

Escrow accounts holding cash reserves to meet unexpected cash shortfalls. The amount typically equals one month's debt service, real estate taxes, property insurance, and sometimes re-leasing costs.

Reserve accounts holding cash reserves for property maintenance and pending repairs.

A lender, particularly the most senior lender in the property's capital structure, often requires cash management provisions, such as lockboxes and escrow/reserve accounts on highly leveraged properties. Higher leverage increases the stress on a property's cash flows, ultimately increasing the risk and severity of losses. Cash management provisions are important controls to ensure that the sponsor and property managers operate and maintain the property efficiently.

Most CRE loans are nonrecourse. That is, in the event of default, the lender's claim is to the property only; the sponsor is not personally responsible to cover any losses. However, originators usually require nonrecourse carve-outs, holding sponsors personally liable for fraud, misrepresentation, misappropriation, and environmental issues. Most loans also require environmental indemnifications protecting lenders from third-party claims related to property environmental conditions.

Typically, a good originator has expertise not only in real estate, but also in the particular type of property (office, industrial, etc.), the local real estate market, and the type of financing desired. Good originators also perform thorough due diligence on every property underwritten. The performance of loans previously underwritten by an originator can provide insight into the quality of that originator's underwriting practices.

The continued strength of the real estate market and the resulting demand for CRE loans have made the loan origination business much more competitive. As a result, some originators have relaxed their underwriting standards, for example, taking on loans with higher leverage, making more aggressive property performance assumptions, or waiving reserve requirements. Given this trend, the quality and motivation of the originator are increasingly important. For instance, originators looking for market share may be more willing to relax their underwriting. While relaxed standards alone may not spell disaster, the terms of the loan, that is, the interest rate and covenants, should be appropriate for the higher levels of risk.

At origination, a master servicer and a special servicer are appointed. In the event of a short-term cash shortfall, the master servicer advances principal and interest payments to the lender and pays real estate taxes and insurance premiums up to the amount the servicer is likely to recover. The master servicer also monitors documents required by the loan, such as annual property performance reports. For performing these ongoing services, the master servicer earns a fee based on a percentage of the outstanding principal balance of the loan.

The special servicer is appointed to resolve issues relating to a delinquent or defaulted loan. Usually, the master servicer hands over a loan to the special servicer when the loan is more than 60 days delinquent. The special servicer's role is to maximize the amount recovered from a defaulted loan and minimize loan losses. The special servicer is compensated by a fee on the principal balance of the assets it is monitoring (often twice the master servicer's fee), an additional workout fee for loans in default, as well as a percentage of the loan's principal and interest recovered through workout. Typically, the special servicer also has an equity interest in the property, increasing the motivation for successfully working out and remedying the defaulted loan.

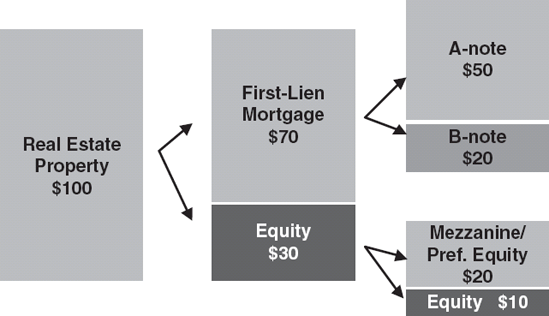

The most basic commercial real estate loan is a first-lien mortgage loan. The first-lien mortgage loan (also known as the "mortgage" or "whole loan") is the senior-most loan secured by the property. At origination, a mortgage's principal balance is typically 65% to 80% of a property's appraised value, commonly referred to as the LTV, or loan-to-value. The mortgage can be split into a senior and a subordinate piece, the A-note and the B-note.

The remaining 20% to 35% is the sponsor's equity interest in the property. However, a sponsor typically targets a 0% to 15% equity interest, depending on the sponsor's motivation. To increase the leverage on a property, a sponsor can take out a mezzanine loan. A mezzanine loan is a senior participation in the equity in the property. The loan is not secured by the property itself, but by an interest in the entity that owns the property (the sponsor). A mezzanine loan essentially reduces the sponsor's equity interest in the property. The loan can raise total leverage on the property to 85% to 100% LTV. In other words, the sum of the mortgage(s) plus the mezzanine loan can equal 85% to 100% of the property's appraised value. As a result, the sponsor's equity interest in the property can be reduced to 0% to 15% of the property's value.

A sponsor may also take out a second-lien mortgage on a property to reduce the equity contribution. Similar to a mezzanine loan, a second-lien mortgage is junior to the first-lien mortgage. However, unlike a mezzanine loan, a second-lien mortgage is secured by the property directly, rather than by an interest in the property's equity. As such, a second-lien mortgage increases the senior debt's risk of default and loss more so than a mezzanine loan. Therefore, first-lien mortgage lenders rarely allow sponsors to take out second-lien mortgages.

Some mortgages also prevent a sponsor from taking out a mezzanine loan. In such cases, the sponsor can instead issue preferred equity. Preferred equity in a property is essentially the same as an equity interest, but has a senior claim on the excess cash flow available after servicing the loans on the property.

Figure 50.1 illustrates a single property's capital structure. Each type of property loan, from A-note through mezzanine, has distinct terms, structure, and risks that we will discuss in the next few sections.

First-lien commercial mortgage loans range from $300,000 to $1 billion. They are typically 10-year balloon loans with 30-year amortization schedules, although there is an increasing number of interest-only loans. Most commercial mortgage loans are fixed rate. Generally, interest rates are 75 to 150 basis points above the 10-year Treasury, but they vary depending on leverage and other property-specific factors.

Prepayment Risk and Extension Risk

Unlike residential mortgages, commercial mortgages have low prepayment risk, thanks to the numerous call protection mechanisms built into the loan terms. Call protection mechanisms include the following:

Lockout. Prepayments are prohibited during a 2- to 5-year lockout period.

Yield maintenance. Equivalent to a "make-whole" premium in corporate bonds. To prepay a loan, the sponsor must make the lender whole. The yield maintenance cost is equivalent to the present value of all the future cash flows due on the loan, discounted at the then-prevailing yield of a comparable maturity U.S. Treasury.

Defeasance. To defease a loan, the sponsor must pledge to the lender U.S. Treasury securities that generate cash flows equal to the cash flows due to the lender under the terms of the loan. From the lender's viewpoint, cash flows are the same, but the underlying collateral will be upgraded to U.S. Treasury securities.

Prepayment penalty points. In prepaying a loan, a sponsor pays the lender a fee equal to a set percentage of 1% to 5% of the outstanding loan balance. Penalty points usually decrease as the remaining life of the loan decreases, e.g., 5% in Year 6, 4% in Year 7, 3% in Year 8, and so on.

For a more detailed discussion of these mechanisms, see Cheng, Cooper, and Huang 1999.

The most common call protection mechanism is a combination of lockout for the first five years, followed by defeasance, which remains in effect until approximately six months before maturity. The sponsor then has a six-month window to refinance the loan without penalty.

Call protection mechanisms lessen the economic incentive to refinance a commercial mortgage. Essentially, a sponsor is likely to prepay a commercial mortgage only if the property is being sold and the gain on the property exceeds the cost of prepaying the mortgage.

Although there is little prepayment risk in commercial mortgages, there is refinancing risk. The 10-year balloon structure of mortgage loans makes extending the loan past the 10-year maturity unlikely, which is a plus for many investors. If the mortgage is not paid off or refinanced at maturity, the loan is in default.

The ability to refinance at maturity, however, depends on several factors that are often out of the sponsor's and the lender's control, such as prevailing interest rates, the strictness of current underwriting requirements, credit conditions, and property occupancy at the time of refinancing. Some loan originators allow short-term extensions, but historically there are significant disincentives for extending. However, in strong markets, originators may relax these disincentives, thereby introducing greater extension risk into commercial mortgages.

Some commercial mortgages are partially or fully interest-only loans, which contribute to extension risk. An interest-only loan faces more extension risk because its principal has not amortized, therefore leaving a larger outstanding loan balance to refinance.

The A/B Structure

A mortgage is often split into a senior and junior participation, the A-note and the B-note. In the A/B structure, as it is called, the A-note has a senior claim on cash flows generated by a property, while the B-note has a subordinate claim on cash flows. (The first lien mortgage can also have an A/B/C structure. This is similar to the A/B structure, but the C-note becomes the most junior note in the structure. Since the concept is very similar, and less common, than the A/B structure, we focus our attention in this chapter on the A/B structure.)

Payment of principal and interest can either be pro rata or sequential. The desired rating on the A-note determines the size of each piece. Typically, the A-note is sized for a BBB or BBB- rating, while the B-note is below investment grade or unrated. The B-note provides credit enhancement and essentially reduces the leverage of the A-note. For example, while the LTV of the entire mortgage may be 80%, the LTV of the A-note would only be 65%, assuming an 80/20 split between the A-note and B-note.

The A-note is usually placed in a trust for securitization. The B-note, on the other hand, is held by a third party, often an experienced real estate investor. In the worst-case scenario, the B-note holder could essentially become the equity owner of the property. Therefore, the B-note holder is usually experienced in underwriting, monitoring, and, if need be, remedying property performance. The B-note holder is compensated for that increased risk position, though returns depend on the underlying property's characteristics, most notably its leverage. Spreads on B-notes can range from as low as 75 basis points to more than 1,000 basis points above Treasuries.

If a sponsor defaults on a mortgage loan, the A-note holder has the right to foreclose and take possession of the property. In this case, the B-note holder loses all collateral securing the note, and is essentially left with an equity interest in the property. This process can take 6 to 18 months, during which time the value of the property may deteriorate, thus increasing the B-note holder's risk of losses. To avoid this scenario, the B-note holder is granted specific rights, which are outlined in the participation agreement and the pooling and servicing agreement.

For instance, in the event of a mortgage default, the B-note holder has the right to cure the default. The B-note holder would thus pay the principal and interest due to the A-note holder, plus any accrued interest, legal fees, and advances. B-note holders are likely to exercise this right if there is sufficient property value above the principal of the A-note and the B-note, or if the property is a transitional property.

A transitional property is a poorly performing property, where performance and value can be increased by an improvement in the overall real estate market, improving the property through capital expenditures or new leases, or by replacing the existing property manager. In such cases, the B-note holder typically has experience in turning around properties. The B-note holder has 3 to 6 months to exercise her right to cure the mortgage.

The B-note holder also has the right, if the mortgage is in default, to buy out the A-note holder. In this case, the B-note holder becomes the senior mortgage lender and gains full control over the entire debt structure of the property, and can foreclose on the property at any time. To exercise this right, the B-note holder must pay the A-note holder the value of the A-note plus accrued interest, legal fees, and advances. A B-note holder with workout experience is likely to choose this option if the economics make sense.

If the B-note holder chooses not to exercise either the right to cure the defaulted mortgage or the right to buy out the A-note holder, she still has the right to approve the special servicer and the terms of the workout plan for the defaulted loan. This allows the B-note holder some control over the workout process, which directly impacts the level of potential losses the B-note holder may realize.

In addition to rights in the event of default, the B-note holder has predefault rights. For instance, the B-note holder typically has the right to approve:

Annual property budgets.

Key tenant leases.

Property management and leasing agents.

Transfer of the property by the equity holders.

Escrow/reserve disbursements.

Approval rights over the budget, leases, property management, leasing agents, and property transfer give the B-note holder some control over the property's performance. Rights over escrow/reserve disbursements provide the B-note holder with protection over improper cash flow distributions to equity holders. B-note holders can also institute an excess cash flow trap to redirect cash flows from equity holders if the property's cash flows trip a specified trigger. The excess cash trigger is typically set at a minimum debt service coverage ratio, a measure we discuss later in this chapter.

Mezzanine loans are the junior-most loans in a property's capital structure. They enable a sponsor to increase a property's leverage, raising total loan-to-value ratio (LTV) to 85% to 100%. These loans typically have a minimum size of $3 million.

Mezzanine loan terms depend on the sponsor's motivation. If current rates are high, the sponsor may opt for a first lien mortgage with a low LTV, then supplement it with a short-term mezzanine loan to reduce her equity contribution. This arrangement allows the sponsor to refinance the mezzanine loan (or the entire mortgage, if the economics work) at a later date when rates are lower, or when the property is performing better. Alternatively, a sponsor may choose a mezzanine loan coterminus with the mortgage to take maximum advantage of an arbitrage opportunity. Therefore, maturities on mezzanine loans range from 18 months to 10 years; some are amortizing, some interest-only, depending on the property and the sponsor's preferences.

As mentioned earlier, a mezzanine loan is not secured by the property itself, but by an interest in the entity that owns the property. It is the first loan to absorb any losses or cash flow shortfalls. Therefore, mezzanine lenders demand a higher interest rate than A-note holders, sometimes significantly higher (upwards of 1,000 basis points) depending on the property and its leverage. Historically, mezzanine loans are held by experienced third-party real estate investors.

Similar to B-note holders, a mezzanine lender has specific rights to protect her investment and minimize losses. These rights are outlined in the intercreditor agreement between the mortgage lenders and the mezzanine lender. For example, if a sponsor defaults on the mezzanine loan, while the first lien mortgage is still current, the mezzanine lender has the option of foreclosing on the sponsor and taking control of the property (subject to the terms of the property's existing mortgage).

Foreclosing on the sponsor is generally quick, taking 60 to 90 days rather than the 6 to 18 months it would take an A- or B-note holder to foreclose on the property. Therefore, the mezzanine lender can gain control of the property more quickly than a B-note holder if property performance goes south. The quicker a lender can take control of a property in default, the sooner she can take actions to remedy or turn around the property, thus minimizing potential losses.

In the event the sponsor defaults on both the mortgage and the mezzanine loan, either the A-note or B-note mortgage lender can foreclose on the property. In this case, the sponsor no longer owns the property; the foreclosing lender does. The sponsor therefore has no collateral, and since the mezzanine lender is secured by an interest in the sponsor, the value of the mezzanine loan goes to zero.

To protect the mezzanine lender in the event of default on the mortgage, the mezzanine lender has rights similar to those of a B-note holder. First, the mezzanine lender has the right to cure the mortgage. This is identical to the right of the B-note holder, but the mezzanine lender has an unlimited amount of time to exercise this right, whereas the B-note holder has to exercise within three to six months. The mezzanine lender also has the option to buy out the mortgage from the mortgage lenders and take control of the property's entire capital structure, with the right to foreclose at any time. Which right the mezzanine lender exercises depends on her real estate expertise.

A mezzanine lender also has predefault rights, similar, though junior to the B-note holder's predefault rights as outlined above. The mezzanine lender also has the right to approve any refinancing of the mortgage. Furthermore, the mortgage lender is not allowed to make any changes to the mortgage loan documents that would be detrimental to the mezzanine lender, such as raising the mortgage rate.

The strong performance of real estate assets over the past decade has increased demand for alternative types of CRE loans. The most common include construction loans, condo- and co-op conversion loans, and land loans. Each carries distinct risks that require additional consideration over the more traditional mortgage and mezzanine loans.

Construction loans, for example, are secured by properties that are under construction. These properties are therefore non-cash flowing, or are generating very little cash. The sponsor usually sets up a reserve account at loan origination which pays the loan's interest. Loan repayment is contingent on construction completion, at which point permanent financing (or temporary bridge financing if the property is not yet leased at completion) is put in place.

These loans tend to be floating rate with maturities of 12 to 36 months and are funded in stages as construction costs are incurred. The loan amount is determined by the construction budget plus a 10% to 20% contingency. Loan performance depends on the sponsor's credit quality and her expertise in managing and monitoring the construction process.

Rating agencies generally consider alternative loans to be riskier than first lien mortgages, so more careful underwriting and monitoring is required. Inclusion of these types of loans in CRE and CMBS CDOs often results in higher subordination requirements.

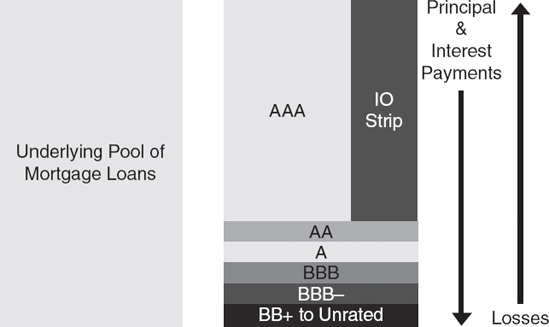

Commercial mortgage-backed securities (CMBS) are backed by a static pool of commercial mortgage loans, the vast majority of which are A-notes. The pool of loans is tranched into a number of rated tranches, and principal and interest payments received from the underlying loans are used to pay principal and interest to the tranches sequentially by seniority. Any losses experienced by the underlying loan pool are absorbed, in order, by the most junior tranches.

Figure 50.2 illustrates the typical structure of a CMBS transaction. The AAA-rated tranche makes up a large portion of the debt structure, generally around 90%, and can be time-tranched into 5- and 10-year securities. Interest-only securities are often included in the structure as well.

CMBS deals appoint a master servicer to monitor the cash flows coming from the underlying loans and going out to the tranches. In the event there is insufficient cash to make all scheduled payments, the master servicer will advance principal and interest. Advancing will continue as long as these amounts are deemed recoverable. A special servicer is also appointed to handle any loans that are more than 60 days delinquent.

Property-type diversification is one of the principal benefits of securitization, since the performance of each property type is impacted by different sets of risks. Properties securing commercial real estate loans include office buildings, industrial buildings or warehouses, apartment buildings, hotels, and retail properties such as strip malls. The concentrations of different property types vary slightly over time, depending on collateral performance. In general, office, retail, and multifamily properties tend to dominate most CMBS, historically accounting for two thirds of the collateral in CMBS deals.

CMBS investors as a whole are a diverse group, but particular types of investors are drawn to different tranches of CMBS deals. Real money investors, financial institutions, insurance companies, etc., tend to buy investment-grade tranches. Traditional real estate investors, hedge funds, and CRE CDOs enter the mix further down the capital structure. Buyers of tranches rated BB+ and below, collectively referred to as the "B-piece," are typically real estate investors, with expertise to underwrite the loan portfolio and accurately assess the risks of the B-piece's first loss position. Top B-piece buyers include LNR Partners, American Capital Strategies, ARCap, J. E. Roberts, and CWCapital.

The prepayment stability offered by CMBS attracts investors looking for real estate exposure without the negative convexity found in residential mortgage-backed securities. Unless interest rates drop dramatically or property values soar, refinancing of the underlying loans is uncommon, due to the call protection mechanisms on the loans.

However, in a robust commercial real estate market, prepayments in the form of defeasance increase, as sponsors look to cash in on property price appreciation. Defeasance, however, is actually a plus for CMBS, as cash flows to the tranches remain the same, with their source becoming Treasury securities, thus raising the credit quality of the tranche's underlying collateral.

The sequential pay structure of CMBS itself provides additional prepayment protection to the junior tranches of the deal. The AA-rated tranche cannot be paid down before the AAA tranche is completely paid. And the A tranche cannot be paid down before the AA tranche, and so on. Therefore, the A tranche is guaranteed to remain outstanding in full at least until the AA tranche is completely paid down. However, principal losses from loan defaults impact the bottom of the CMBS structure upward, so the principal balance of the more junior tranches may be reduced due to principal writedowns.

Unfortunately, CMBS have extension risk, due to the 10-year balloon maturities of the underlying loans. If a loan cannot be refinanced and it defaults, the loan enters a workout period that can extend principal recovery for months, even years. The most subordinate tranches of a CMBS transaction bear the most extension risk, as they are the last to receive principal payment.

Interest shortfalls can be a concern to CMBS tranches, especially to the below investment grade and unrated tranches. Interest shortfalls occur when the CMBS transaction has insufficient funds to pay interest due tranches. Shortfalls are more common in CMBS transactions than other asset-backed transactions, yet they are usually less serious occurrences.

In other asset-backed securities, basis mismatch is the chief factor in interest shortfalls. Basis mismatch frequently occurs in rising interest rate environments when the coupons payable to the tranches reset at higher rates before the coupons on the underlying collateral reset, thus causing an interest shortfall. This type of interest shortfall is not a concern in CMBS, because CMBS have little, if any, inherent basis risk, since both the underlying loans and the coupons payable on the tranches are typically fixed rate.

Most interest shortfalls in CMBS are due to loan delinquencies and defaults. Except when the default is severe enough to cause a loss on the loan, interest will be recovered in part or in full when the sponsor cures the loan or when the property is liquidated. The CMBS master servicer advances funds to cover interest shortfalls that are likely to be recovered. Due to high collateral concentrations and long workout periods for defaulted loans, CMBS tranches can experience interest shortfalls for long periods of time, yet retain high likelihood of recovery.

Most CMBS interest shortfalls are recoverable, but some are not. For instance, the master servicer will not cover shortfalls resulting from delinquent loans where the underlying property has been reappraised to a negative LTV. In this case, the CMBS tranches, particularly the lowest rated, will absorb the shortfall as a loss. The master servicer does not cover shortfalls due to nonreimbursable costs such as litigation expenses or workout fees, either. Unrecoverable interest shortfalls are concerns for CMBS investors. Recent high-profile interest shortfalls in a few CMBS transactions have caused tranche downgrades and principal losses, with a few tranches losing 100% of their principal, thus increasing investor concerns over interest shortfalls.

CMBS deals with interest shortfall issues include: Asset Securitization Corp. 1996-D2 due to delinquent properties being re-appraised at lower values; Morgan Stanley Capital I 1998-CF1, JP Morgan Chase Commercial Mortgage Securities Corp. 2003-FL1, LB Commercial Mortgage Trust Series 1998-C4, and Bear Steams Commercial Mortgage Securities Series 2001-TOP2, all due to unrecoverable fees.

CMBS provide investors with exposure to a diversified pool of commercial real estate loans. Variations in loan size, sponsor, property type, geographic location, leverage levels, and the like, all contribute to the diversification benefits of CMBS. These characteristics underlie the performance of the collateral and as a result impact the CMBS tranche ratings and subordination levels.

CMBS deals are often categorized into four groups, depending on the type of loans underlying the deal, as shown in Table 50.1. Conduit loans are mortgage loans originated by conduit lenders for the sole purpose of securitizing them. These loans tend to be small in size, generally less than $10 million, but they can be larger. Almost all conduit CMBS deals are fusion deals which consist of a diverse pool of small loans as well as a small number of larger loans. Conduit CMBS deals have historically dominated the CMBS market.

Table 50.1. CMBS Deal Categories

Deal Categories | Description |

|---|---|

Conduit loans Traditional | Pool of loans where no loan is greater than 10% of the total principal of the deal. |

Fusion | Pool of loans where a few of the loans are greater than 10% of the total principal of the deal. |

Large loan | Pool of loans where several loans are greater than 10% of the total principal of the deal. |

Credit tenant leases | Pool of loans secured by property leases. |

Single asset/Single borrower | One loan secured by a single property or a pool of loans from the same borrower. |

Large loans are property loans that are greater than $35 million in size. Credit tenant leases (CTLs) are often the result of sale-leaseback transactions. The tenant sells corporate-owned real estate and enters into a long-term lease on the property or properties. The leases are structured such that the default risk of the lease is tied to the credit rating of the tenant. The tenant's default risk is fundamentally different than the default risk of a traditional commercial real estate loan, and can often gain a higher credit rating. Single-asset CMBS deals contain just one, large loan on a single property, such as, a large high-rise office building. Single-borrower CMBS deals contain a pool of loans on properties with the same borrower or sponsor. Often pool loans are cross-collateralized, so that if one loan defaults, the lender has recourse to any or all of the pool's properties.

Real estate investment trusts (REITs) are entities that buy, develop, manage, and sell real estate assets. A special feature of REITs is that they qualify as pass-through entities which are exempt from corporate level taxes. To qualify as a REIT, the entity must pay out dividends equal to 90% of its taxable income and more than 75% of its total assets must be in real estate. A REIT generates income through the operation and management of real estate assets. Sales of asset held less than four years cannot exceed 30% of the REIT's net income. Therefore, a REIT is clearly a "buy and hold" entity, not an asset flipper or a trader.

REITs fall into three broad categories: equity REITs, mortgage REITs, and hybrid REITs. Equity REITs own and operate a portfolio of real estate properties, usually focusing on a particular type of property such as office buildings. Mortgage REITs invest in, and in some cases originate, mortgage loans and mortgage-backed securities. Hybrid REITs combine the investment strategies of equity and mortgage REITs by investing in both properties and mortgages. Equity REITs dominate the REIT market, accounting for about 95% of total REIT market capitalization.

The REIT capital structure consists of secured bank loans, unsecured debt, preferred stock, and equity. Some REITs have also issued trust preferred securities (TruPS). (For more information on the mechanics of TruPS, see Chapter 8 in Lucas, Goodman, Fabozzi, and Manning 2007.) Unsecured REIT debt and TruPS have significant covenants to protect investors. A typical covenant package includes the following:

Total debt cannot exceed 60% of total assets.

Unencumbered assets must be at least 150% of unsecured debt.

Secured debt cannot exceed 40% of total assets.

Interest coverage must be greater than 1.5 ×.

Given these covenants, BBB-rated unsecured REIT debt is comparable to single-A-rated CMBS debt given the similar leverage and interest coverage levels. However, a REIT's asset portfolio, and therefore its financial ratios, can change over time, unlike the static pool of assets securing CMBS debt. Also, the REIT's debt is unsecured, while CMBS debt is secured by a pool of first mortgages. Therefore, unsecured REIT debt will likely be rated below CMBS debt that has similar leverage and interest coverage levels.

REIT securities are purchased by a variety of investors, from insurance companies, mutual funds, and CDOs to individual retail investors. REIT securities provide investors with exposure to a diversified pool of real estate-related assets with little to no negative convexity, as opposed to investments in residential mortgage-backed securities (RMBS). In addition, REITs resemble corporates more than CMBS or RMBS, which opens them up to a large investor base.

Analysis of commercial real estate investments, whether investments in B-notes or CMBS tranches, begins with an analysis of the underlying property, followed by an analysis of the loan terms. For CMBS investments, additional analysis is needed at the bond or equity level. We discuss these three types of analysis next.

The first step in analyzing real estate investments is a property-level analysis. Understanding the property, from the credit quality of the third-floor tenant to the conditions of the local and general economies, is fundamental in assessing the financial condition of the property. Property-level analysis includes many of the elements of underwriting a loan on a property, such as property appraisals, tenant and lease review, comparable property analysis, and the like. These components are used to estimate the stabilized cash flow of the property.

A property's value can be derived from its stabilized cash flow by applying a capitalization rate appropriate for the property. A capitalization rate, or cap rate, is essentially an idealized unlevered risk-adjusted return. Embedded in the cap rate are assumptions about the relative quality of the property, the cash-flow volatility common to that type of property, comparable property yields, yields on other types of investments, and so on. The value of the property is its stabilized cash flow divided by the appropriate cap rate. The lower the cap rate, the higher the resulting property value.

Analyzing a CRE loan centers on two key metrics: debt service coverage ratio (DSCR) and loan-to-value (LTV). DSCR is the property's cash flow, less tenant improvements, leasing commissions, and necessary capital expenditures; divided by the debt service on the property's loans. DSCR is considered by the rating agencies to be the best indicator of default probability. The higher the DSCR, or the more cash flow a property has to cover debt service, the greater the property's ability to withstand adverse conditions before defaulting on any loan. S&P reports that the average DSCR on existing commercial mortgage loans is around 1.5 x, although many loans originated today are sized at 1.2 × (see Thompson, Kay, and Ramkhelawan, 2006). For the second quarter of 2006, 21% of the loans in Moody's rated conduit CMBS were sized at 1.2 × or less DSCR, up from just 6.3% a year earlier (see Philipp, Obias, Dent, and Rubock, 2006).

LTV is calculated as the principal loan balance divided by the estimated value of the property. Rating agencies consider the LTV to be the best indicator of loss severity in the event of default. The lower the LTV, or the lower the amount of the loan as a percentage of the property's value, the lower the odds that the loan will suffer losses in the event of default. LTVs can range from 65% to 90%+. S&P reports that the average LTV on securitized first-lien commercial mortgage loans is 69%, although many loans are originated at 80% LTV (see Thompson, Kay, and Ramkhelawan, 2006).

A loan's default probability and loss severity are used to determine expected losses on the loan. When rating agencies calculate expected loss, they often apply qualitative adjustments to the metrics. For example, Fitch may adjust a property's default probability upward if the property's cash flows tend to be volatile. The default probability may also be adjusted upward if the loan is floating rate, as floating-rate loans introduce more variability into the debt service costs. A property's loss severity may be adjusted either upwards or downwards based on the type of loan, be it a whole loan or a mezzanine loan, the strength of the loan covenants, loan amortization, additional debt, and so on. Another consideration is the thickness of the debt. A small piece of debt at the bottom of the capital structure is more likely to be wiped out, even if overall losses are small. Finally, Fitch will adjust the resulting expected losses for reserves, the quality and underwriting practices of the loan originator, potential environmental issues, and so on.

For B-notes, mezzanine loans, and whole loans that have not been securitized, prepayment risk becomes an issue. The financial condition of the property at origination plays an important role in the likelihood of loan prepayment. Most B-notes, mezzanine loans, and whole loans that end up in CRE CDOs are secured by interests in transitional properties or highly leveraged properties. The cash flows on these types of properties tend to be more volatile, and therefore the financing costs tend to be higher. Upon stabilization, the loans can be refinanced on more favorable terms. In such cases, the loan terms tend to provide more prepayment flexibility than do the loan terms on stabilized properties.

Ideally, investors in CMBS and CRE CDOs, especially noninvestment grade and equity investors, will perform both property-level and loan-level analysis on every loan underlying the CMBS or the CDO. However, this type of in-depth analysis is not always possible, and in the case of a CDO, this is partially why investors pay management fees. Nonetheless, prudent investors will do substantial homework on the underlying properties and loans. Analysis on properties, or sponsors, that make up a large percentage of the pool backing the CMBS or CDO will give investment-grade tranche investors some confidence in the performance of the overall pool, while analysis of the entire pool is best for non-investment-grade and equity investors.

For CMBS investments, additional bond-level analysis is required. This includes looking at the pool of loans in a CMBS trust as a whole and assessing the collateral concentrations. Property-type, geographic, and loan-type concentrations are all important pool characteristics that impact the likelihood and correlation of defaults as well as losses. The ratings of the underlying collateral and the pool's weighted average rating are important pool characteristics, as well. In addition, the rating agencies calculate a CMBS pool's Herfindahl score, which is a measure of the effective number of assets in the pool, and accounts for concentrations due to loan size. The Herfindahl score, per Moody's, is calculated as follows for a pool consisting of N assets:

Rating agencies determine required credit enhancement using these pool metrics, as well as the pool's overall DSCR and LTV.

In addition to analyzing the underlying pool, bond-level analysis requires cash flow modeling. Cash-flow modeling incorporates the specific structure of the CMBS, including the protective effects of overcollateralization and cash flow diversion mechanisms. With an accurate model of the CMBS tranche, cash flows can be tested for their response to various levels of default, recovery, prepayment, and other factors.

As the commercial real estate market has evolved, so have CRE investments. In this chapter, we have reviewed the different types of CRE investments from first-lien mortgages to CMBS. We looked at different structures and showed how CRE loans and securities provide investors with levered exposure to price appreciating assets with the ability to customize that real estate exposure via credit enhancement and diversification. Then we discussed several factors to consider when investing in CRE, including property-level analysis, loan-level analysis, and bond-level analysis.

Cheng, D., Cooper, A. R., and Huang, J. (1999). Understanding prepayments in CMBS deals. In E J. Fabozzi and D. R Jacob (eds.), The Handbook of Commercial Mortgage-Backed Securities (pp. 147-158). Hoboken, NJ: John Wiley & Sons.

Esaki, H., and Goldman, M. (2005). Commercial mortgage defaults: 30 years of history. CMBS World 6, 4: 1 21-29.

Fabozzi, F. J. (ed.) (2001). Investing in Commercial Mortgage-Backed Securities. Hoboken, NJ: John Wiley & Sons.

Lucas, D. J., Goodman, L. S., Fabozzi, F. J., and Manning, R. J. (2007). Developments in the Collateralized Debt Obligations Markets: New Products and Insights. Hoboken, NJ: John Wiley & Sons.

Philipp, T., Obias, P., Dent, P., and Rubock, D. (2006). US CMBS and CRE CDO 2Q 2006 review: Credit metrics and spreads send conflicting signals. Moody's Investors Service, July 31.

Snyderman, M. (1991). Commercial mortgages: Default occurrence and estimated yield impact. Journal of Portfolio Management 18,1: 82-87.

Thompson, E., Kay, L., and Ramkhelawan, G. (2006). Defaults and losses of U.S. commercial mortgage loans: Year-end 2005 update reveals improved credit performance. Standard & Poor's, June 8.