SHANI SHAMAH

Consultant, E J Consultants

Abstract: Not surprisingly, over the past few years the financial markets have responded to increasing price volatility and there are now a range of financial instruments and strategies that can be used to manage the resulting exposures to financial price risk. At one level, there are now financial instruments that permit the direct transfer of financial price risk to a third party, who is more willing to accept that risk. At another level, the financial markets have evolved to the point whereby financial instruments can be combined with other instruments to unbundled financial price risk from the other risks inherent in the process, for example, raising capital.

Keywords: forward contracts, interest rate differentials, short-dated contracts, long-dated contracts, broken-dated contracts, nondeliverable forward (NDF), foreign exchange swaps, currency swaps, foreign exchange futures, exchange for physical (EFP), currency options, forward points, forward pips or swap points, premium, discount, bids, offers

In today's business world, unpredictable movements in exchange rates, interest rates and commodity prices cannot only affect a company's performance but may even determine whether a firm survives. Over the past couple of decades, companies have been increasingly challenged by financial price risks. It is no longer enough to be the company with the most advanced production technology, the cheapest labor supply, or the best marketing team. Price volatility can put even well-run companies out of business and changes in exchange rates can create strong new competitors. Similarly, fluctuations in commodity prices can drive input prices to the point that substitute products (or products made from different inputs) become more affordable to end users. Changes in interest rates can put pressure on the company's costs, as higher interest rates may hurt sales and thus the company could find themselves in financial distress as sales plummet and borrowing costs skyrocket. Hence, it is not surprising that the financial markets have responded to increasing price volatility with a range of financial instruments and strategies that can be used to manage the resulting exposures to financial price risk. Such financial instruments are covered in this chapter and includes FX forward contracts, nondeliverable forwards (NDFs), FX swaps, currency swaps, FX futures, and exchange for physical (EFP).

Forward contracts are a common hedging product and are used by importers, exporters, investors, and borrowers. They are valuable to those with existing assets or liabilities in foreign currencies and to those wanting to lock in a specific foreign exchange rate in the future. For example, corporations that must receive or pay foreign currencies in the future because of their normal business activities usually prefer to transfer the risk that the values of these currencies will change during the intervening period. They can use the bank forward market to establish today, the exchange rate between two currencies for a value date in the future. Generally, when corporations contract to pay to or receive from a bank foreign currency in the future, no money is exchanged until the settlement on the value date.

While forwards may be used to hedge payables and receivables, corporations will also hedge other assets and liabilities on a company's balance sheet. The value dates of forward contracts are often constructed to match up with the expected dates of receipts for a foreign payment, or payment of a foreign currency obligation. A forward contract can be tailored to meet a client's specific needs in terms of delivery dates and amount. In addition to transacting with clients, banks actively trade forward currency commitments among themselves, as well.

In essence, forwards provide certainty in the uncertain world of currency movements by locking in a specific rate, and as the forward markets are quite liquid, the bid/offer spreads are relatively low for the major currencies.

By way of definition, a forward contract (or forward outright) is a transaction executed today in which one currency is bought or sold against another for delivery on a specified date that is not the spot date, for example, three months from now. In addition, forward points are relative interest rate differentials expressed as units of currency, or fractions of the spot value of that currency.

Forwards work much like spots, but the value date is different from the spot date and usually extends further into the future, for example, six months from the commencement date. At first sight there would seem to be no reason why the spot and the forward rate are not the same. However, one of the factors influencing a currency's forward exchange rate is the level of interest rates for that currency relative to interest rates in the other currency. There are many theories on how a forward exchange rate can be calculated, but market participants adopt the interest rate differential between two currencies and the current market spot rate, as the basis of their calculations. The forward price is often referred to as forward points, forward pips or swap points (pips).

For example, assume the spot and forward rates between dollars and sterling are the same, but the interest rates in sterling are 4% per annum for a three-month deposit, while in dollars they are 2%. Investors would sell their dollars and buy sterling spot for the higher yield. They would simultaneously sell sterling and buy dollars forward for delivery at the end of the investment period. In this way, the investor would end up with more dollars than if the investment had been kept in dollars.

Market makers regularly trade forward contracts for periods of 1, 2, 3, 6, and 12 months from the spot value date value date. A broken date or odd date forward deal is a contract with maturity other than a normal market quote of complete months. An example would be to ask for the forward pips for 24 days.

Forward contract prices are determined by two main factors: the current spot price between the two currencies and the interest rate prevailing in each of the two currencies. The forward price is calculated as the spot rate plus or minus the forward pips. To decide whether to add or subtract the forward pips, firstly determine whether the currency to be bought or sold is trading at a premium or is trading at a discount. As all exchange rates have a fixed and a variable component, if the interest rates in the variable currency are greater than those of the fixed currency, the variable currency is trading at a discount relative to the fixed currency and forward pips are added to the spot rate to obtain the forward rate. If the interest rates in the variable currency are less than those of the fixed currency, the variable currency is trading at a premium and forward pips are subtracted from the spot rate to obtain the forward rate.

There are two simple rules of thumb to decide if a currency is at a premium or a discount, and what to do with the forward points. Remember, exchange rates are quoted as units of that currency, which equal $1 (except for sterling, euro, and a few other currencies like the Australian and New Zealand dollar).

If the forward points are ascending, for instance, if the offer is numerically higher than the bid (20/25), that is, if the forward points rise from left to right, the currency is at a discount to the dollar and, hence, the forward points are added to the spot rate. (The major exception is sterling and the euro, where they are at a premium to the dollar.) If the bid is numerically higher than the offer, that is, the points are descending (25/20), that is, the forward points decline from left to right, the currency is at a premium to the dollar and the forward points are deducted from the spot rate. (The major exception is the quotation for the euro and sterling against the dollar, where if the forward points decline from left to right, the points are deducted, but the dollar is at a premium to the euro and sterling).

Forward rates are not determined by where the market expects the currency to be in the future, but rather by the interest rate differential. Also, the forward exchange rate is fixed at the time of the transaction, but no accounts are credited or debited until the maturity date.

The forward pips are calculated in the following way. If we assume that the spot and forward rates between dollars and sterling are the same, say 1.4400/10, but the interest rates in sterling are 4% per annum for a three-month deposit, while in dollars they are 2% per annum for the same deposit, investors would sell their dollars and buy sterling spot for the higher yield. They would simultaneously sell sterling and buy dollars forward for delivery at the end of the investment period. In this way, the investor would end up with more dollars than if the money had been kept in dollars. For example, if Mr. Jones has $5 million to invest for three months, at 2%, the interest earned at the end of the period will be:

Thus, the total principal and interest earned at the end of the period will be $5,025,555.56 ($5,000,000 + $25,555.56).

However, if Mr. Jones buys sterling at 1.4410 and sells his dollars, he will receive £3,469,812.63, which can be invested at 4% for the same period. The interest earned at the end of the period will be:

Thus, the total principal and interest earned at the end of the period will be £3,504,795.95 (£3,469,812.63 + £34,983.32).

This can then be converted back into dollars at 1.4400, which would give an amount of $5,046,906.17 (£3,504,795.95 × 1.4400). The total gain, at the end of the period will be $21,350.61 ($5,046,906.17 - $5,025,555.56).

In a free market, however, the advantage of the higher sterling interest rate is usually neutralized by the lower value of sterling in the forward foreign exchange market and any yield pickup will be small, or nonexistent.

In calculating the forward points, users adopt a simple arithmetic formula which takes the interest rate differential per annum, converts it into a differential for the required period, and then expresses the spot rate as a percentage of the differential for the period. However, it cannot be used entirely in isolation, for it assumes knowledge of relative interest rate levels by the interested party. It is, in essence, a variation on the old banking formula:

where the principal is the spot rate, the rate is the interest rate differential and time is the maturity in days. Thus:

In other words, the formula for dollars against currency forwards is:

which equals the number of forward points of spot currency, with 360 day basis, where

| A = spot exchange rate |

| B = currency interest rate |

| C = dollar interest rate |

| D = maturity in days |

| E = day basis |

It has to be noted that, in the money market, all calculations are based on the actual number of days elapsed divided by 360, except for calculations involving sterling and some other currencies when 365 days are used. The formula is adjusted when the two currencies involved have a different day base. Also, when the value date is the last business day of a month, the corresponding date in any future month is also the last business day. For example, if the spot value date were February 28, the value date in a one-month forward transaction would be March 31. If the spot value date were May 31, the six-month forward transaction date would be November 30. If the last day of the month is not a business day, then the value date is the next preceding business day.

Just as there is a bid and offer in the spot market, there is a bid and offer rate in the forward market as well. This means that the forward points for both sides of the exchange rate must be quoted. A typical example of how forward rates are quoted is:

Currency | 1 month | 3 month |

|---|---|---|

USD/JPY | 19.55/19.30 | 62.7/61.7 |

USD/CHF | 0.1/1.1 | 1.7/1.9 |

EUR/USD | 9.07/8.99 | 29.5/27.8 |

As already has been mentioned, the simple rule to arrive at the forward rate is if the forward pips decline from left to right, the currency is at a premium to the dollar and the forward pips are deducted from the spot rate. For example, if spot $/JPY is 117.06/117.09, the one-month forward price is:

| 117.06 − 0.1955 and 117.09 − 0.1930 = 116.8645/116.897 |

If the forward pips rise from left to right, the currency is at a discount to the dollar and the forward points are added to the spot. For example, if spot $/CHF is 1.2507/10, the three-month forward price is:

| 1.2507 + 0.00017 and 1.2510 + 0.00019 = 1.25087/1.25119 |

The major exception is the quotation for sterling against the dollar, where if the forward pips decline from left to right, the pips are deducted but the dollar is at a premium to sterling. Occasionally, it is possible to have forward pips that have a negative number for one side of the quote and a positive number for the other. An example would be −0.7/+1.3. The rules for adding or subtracting are still the same. This type of forward pips behavior occurs when the interest rates of the two currencies are so close, that the offer side of one crosses the bid side of the other.

When a market maker quotes a forward price, the trader is likely to say:

| "Three-month dollar/yen 62.7 at 61.7" |

Where the market maker will buy and sell JPY at −62.7 pips (sell and buy dollars) and will sell and buy JPY at –61.7 pips (buy and sell dollars). Of course, for currencies quoted in American terms, that is, euro, the market maker will quote a one-month forward price as:

| "One-month euro/dollar 9.07 at 8.99" |

where the market maker will buy and sell dollars at —9.07 pips (sell and buy euro) and will sell and buy dollars at —8.99 pips (buy and sell euro). Some examples of forward quotations are:

Forward cross rates are worked out in the same manner as for spot rates. First, work out the forward rate from the spot rate and the forward points. Then, decide what currency is being bought and which one sold. Finally, decide if the rates should be divided or multiplied by one another, as appropriate.

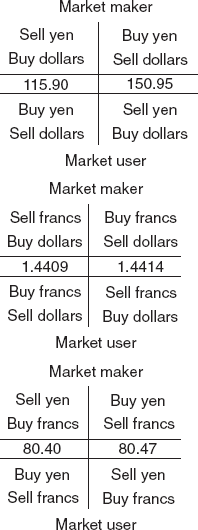

For example, by using the forward points in the table below,

USD/JPY | USD/CHF | CHF/JPY | |

|---|---|---|---|

Spot: | 115.90/95 | 1.4409/14 | 80.41/80.47 |

3-month pips: | 53.9 − 53.6 | 27 − 26 | 23 − 22 |

CHF/JPY three-month forward can be worked out as:

3 months USD/JPY | 3 months USD/CHF | 3 months CHF/JPY |

|---|---|---|

115.90 − 115.95 | 1.4409 − 1.4414 | 80.41 − 80.47 |

−53.9 −53.6 | −27 −26 | −23 −22 |

115.361 to 115.414 | 1.4382 to 1.4388 | 80.18 to 80.25 |

As described in Chapter 64 of Volume I where spot pricing and calculations are covered, the bid for spot Swiss francs against Japanese yen is derived by taking 115.90 (bid) and dividing it by 1.4414 (offer), in order to reach the spot price of 80.41. Likewise, in order to obtain the offer spot price of Swiss francs against Japanese yen, take the offer of dollar yen, 150.95 and divide it by the bid of dollar Swiss franc 1.4409, which gives 80.47. In other words:

Because of the time span involved in forward contracts, there can be significant risks, just like with a spot deal. Credit risk, market/price risk and country risk are all potential problems. In fact, country risk is more significant than for spot trades as unexpected events in a foreign country are more likely given the longer period of exposure.

As has been stated, most foreign exchange deals are executed for value two business days forward, or longer. However, some participants could have a need for currency the same day, the next day or the day after spot. For some currencies, like sterling and euro, it is possible to trade for the same day value, but for the majority of currencies, the earliest execution would be tomorrow. The terminology for these differing time periods is:

Value same day | Overnight | o/n |

Value tomorrow | Tom next | t/n |

SPOT | ||

Value day after | Spot next | s/n |

The rates quoted for value dates occurring before spot are treated in a different way to those occurring after spot. The rules applying to a value date after spot is that if the forward pips go from high to low (20-18), they are subtracted and if the forward pips go from low to high (18-20), they are added to the spot rate. But, if the value date is before spot, the points are switched and then the normal rule is followed. The pips for "overnight" and "torn next" represent only one day each. If, therefore, a rate is calculated for value today, the pips for "overnight" and "torn next" have to be added together.

With any forward transaction, the quotation is based on the relationship between the prevailing interest rates of the two currencies concerned. However, when considering forwards beyond one year, it is necessary to account for the annual interest compounding effect.

The short method for calculating a forward rate beyond one year is to use the normal formula for calculating forward points from interest rate differentials. However, this formula has to be modified to take in to account the effect of the compounding effect of the interest.

Note: The principle for short- or long-dated contracts is the same as with forward rates and is made on the basis of interest rate gain or loss. The exception to the rule is that prices normally added on are deducted and prices normally deducted are added. This, actually, is not as odd as it sounds. If prices are normally quoted for spot delivery and a value tomorrow quote means the market-maker will have to surrender that currency earlier than normal, there has to be some compensation.

A broken-dated contract is a forward contract with maturity other than the normal market quote of complete months and in order to price a broken dated contract, it is necessary to interpolate between the two standard date quotations on either side of the desired maturity. For example, to work out the forward pips for USD/JPY for one and half months (45 days), assume the following rates:

$/JPY spot | 117.06/117.09 |

1 month forward pips | 21/18 |

2 month forward pips | 44/41 |

The pips for buying JPY and selling USD would be calculated according to the following:

Work out the number of days in the period between the one and two month forward quotes, because the delivery date falls within this period. The answer is 45 days.

Subtract the bid one-month forward pips from the bid two-month forward pips, which will then show what the two-month pips are worth over the one-month pips. The answer is 23 forward pips.

Divide the difference in forward pips (23) by the number of days in the period between the two standard quotes (45) and multiply the answer (0.5111) by the difference in the number of days between the required date and the last day of the two month quote (15). Hence, the total of those days is worth 7.7 forward pips.

Subtract this answer (7.7) from the two-month forward pips, giving us the forward pips for the broken date of 36.3.

The interpolated rate is the basis for the market maker's quote, but the actual rate quoted will also probably reflect the market maker's position.

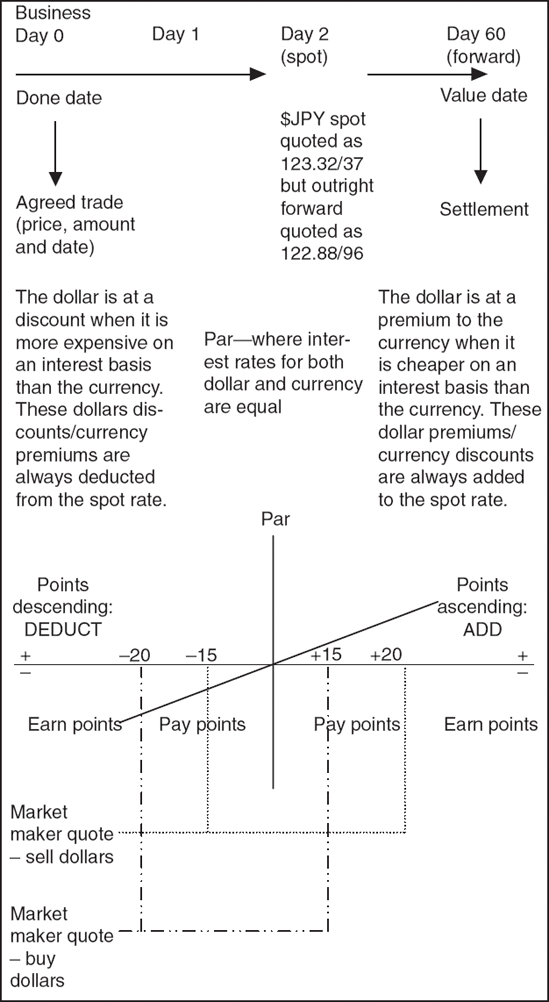

An outright forward contract is the purchase or sale of a currency for delivery on any date other than spot and not forming part of a swap operation. For example, an importer might want to fix the rate today, for the delivery of a shipment in two months' time. The process for the rate on an outright is to use the spot rate and the two-month forward pips. If spot dollar yen is 123.32/37 and the two-month forward pips are 44/41, the outright price for two months time is 122.88/96 (123.32 − 44 and 123.37 − 41). An outright forward transaction is shown in Figure 65.1.

A nondeliverable forward (NDF) is a short-term committed forward "cash settlement" currency derivative instrument. It is essentially an outright (forward) foreign exchange contract whereby on the contracted settlement date, profit or loss is adjusted between the two counterparties based on the difference between the contracted NDF rate and the prevailing spot foreign exchange rates on an agreed notional amount.

When an NDF deal is contracted, a fixing methodology is agreed. It specifies how a fixing spot rate is determined on the fixing date, which is normally two working days before settlement, to reflect the spot value. Generally, the fixing spot rate is based on a reference page on either Reuters or Telerate with a backup of calling between three and five market banks. Settlement is made in the major currency, paid to or by the client and reflects the differential between the agreed-upon NDF rate and the fixing spot rate.

The NDF is quoted using foreign exchange forward market convention, with two way prices quoted as bid/offer pips, at a premium or discount to the prevailing spot market. The spreads are more than likely wider than would be expected in the normal forward market. As with a normal forward transaction, the market user either buys or sells the NDF, depending on the position to be hedged or according to the view of the underlying currency or interest rates.

NDFs are a risk management tool used to hedge the risk of forward currency inconvertibility, which can result from a number of factors, including credit risk, sovereign risk, regulatory restrictions, or lack of settlement procedures. NDFs are typically utilized by banks, multinational cor-porates, investment managers and proprietary traders to hedge currency risk. In addition, NDFs can be used for currency arbitrage, to trade currencies where formal transaction documentation does not exist (as an off-balance sheet product, documentation is not required) or as a tool to facilitate locking in the enhance yields of emerging market currencies. Volatile currencies can bring greater yields when compared to current short-term interest rates in America and Europe.

NDFs are available in several "exotic" currencies, and for most NDF products, prices are quoted for up to one year. It is not unusual to have the spot price being fully convertible, but forwards past spot being quoted only on a NDF basis. Today, most South American countries and some Far East countries operate NDFs.

For example, to hedge against currency depreciation, if the fixing rate is greater than the outright price at maturity, the purchaser of the NDF would receive from the seller the difference between the fixing rate and the outright rate in cash terms. This amount can be calculated by using the following formula:

where

| F = fixing rate |

| O = outright price |

| N = notional amount |

Obviously, if the fixing rate is less than the outright price at maturity, the opposite will apply.

To hedge against currency appreciation, if the fixing rate is greater than the outright price at maturity, the seller of the NDF pays the buyer the difference between the fixing rate and the outright rate in cash terms, calculated as above. As with a purchase, if the fixing rate is less than the outright, the opposite will apply. An example of the above would be:

Notional amount: | $10,000,000 |

Maturity: | 90 days |

Spot: | 2.0000 fx/$ |

90 day NDF: | 0.0100 |

Outright: | 2.0100 fx/$ |

Fixing rate: | 2.0200 fx/$ |

At maturity, the purchaser of the NDF will receive from the seller:

Another example is where, say, an investor has invested $2,000,000 in stock on the Korean stock market for one year. The investor expects the stock market to rise, but is worried about potential Korean won (KRW) depreciation. The investor wishes to hedge the foreign exchange exposure using an NDF. A nondeliverable forward rate of KRW 1310 per dollar is agreed between the bank and the client. The principal amount is $2,000,000. There are three possible outcomes in one year's time:

The KRW has reached the forward rate.

It has depreciated further.

It has appreciated relative to the forward rate.

Examples of the three scenarios are shown below:

Outcome A | Outcome B | Outcome C | |

|---|---|---|---|

USD/KRW | Depreciated | - | Appreciated |

Fixing spot rate | 1330 | 1310 | 1290 |

Equivalent amount | $1,969,925 | $2,000,000 | $2,031,008 |

Settlement | Bank pays client $30,075 | No net payment | Client pays bank $31,008 |

In all outcomes, the client has achieved the objective of hedging the KRW exposure at 1310.

In outcome A, the exchange rate loss that the client would suffer if the investor sells the investment and exchange the KRW proceeds in the spot market, is compensated by the proceeds of the NDF. In outcome C, the client's exchange gain on realization of the investment is countered by the payment the investor makes on the NDF.

For a corporate, an example would be where the corporate is due to receive Philippine pesos (PHP) 102,000,000 in three month's time. They are concerned about potential depreciation and wish to hedge this exposure using an NDF. Assume the agreed NDF rate is PHP 51 per dollar. The principal amount of PHP 102 million is equivalent to $2 million. Again, there are three possible outcomes in three months' time and the consequences provided in the following table:

Outcome A | Outcome B | Outcome C | |

|---|---|---|---|

PHP/USD | Depreciated | - | Appreciated |

Fixing spot rate | 51.5 | 51.0 | 50.5 |

Equivalent amount | $1,980,583 | $2,000,000 | $2,019,802 |

Settlement | Bank pays client $19,417 | No net payment | Client pays bank $19,802 |

Contingent risk—exists when the dollar value of anticipated but not yet committed cash flows is subject to changes in exchange rates.

Sovereign risk—the risk that the government of a country may interfere with the repayment of a debt. For example, a borrower in a foreign country may be economically sound and capable of replaying a loan in local currency. However, his country's government may not permit him to repay a loan to a foreign bank because of a lack of foreign exchange or for political reasons. The bank making the loan in the first place must take this sovereign risk into account and reflect it in the interest rate.

Transaction exposure—arises whenever any company unit commits to pay or receive funds in a currency other than its national currency.

Translation exposure—the risk that financial statements of overseas subsidiaries of a company will gain or lose value because of exchange rate movements when translated into the currency of the parent company upon consolidation.

Characteristics of Emerging Markets

Limited currency convertibility

Central bank regulations

Illiquid markets

Limited hedging vehicles

Event/sovereign risk

Greater volatility

Cross-border risk

Withholding taxes

An index-linked deposit is basically a restructured NDE It is a deposit held in a major currency with its return linked to the exchange rate of an NDF and earning an enhanced coupon. The coupon reflects the implied local interest rates derived from the NDF market, which may be significantly higher than the major currency interest rates. The index-linked deposit is particular suitable for asset managers who need to hold a physical asset, but at the same time, wish to gain access and exposure to higher yielding markets.

Index-linked deposits are available in two types, namely, those linked to principal and interest and those purely linked to principal. The former offers a higher coupon but exposes both principal and interest to exchange rate fluctuations; where as the latter exposes only the principal. Both types of deposit are not principal protected. These deposits not only have many of the same advantages as NDFs, but they also often allow depositors to assume a lower credit risk or to earn more interest than depositing onshore. Moreover, they can be used as a form of collateral for NDFs.

An NDF is a short-term committed forward cash settlement currency derivative instrument. It is essentially an outright (forward) foreign exchange contract whereby on the contracted settlement date, profit or loss is adjusted between the two counterparties basing on the difference between the contracted NDF rate and the prevailing spot foreign exchange rates on an agreed notional amount.

The NDF rate is the rate agreed between the two counterparties on the transaction date. This is essentially the outright (or forward) rate of the currencies dealt. The notional amount is the "face value" of the NDF, which is agreed between the two counterparties. It should again be noted that there is never any intention to exchange the two currencies principal sums—the only movement is the difference between the NDF rate and the prevailing spot market rate and this amount is settled on the settlement date.

Every NDF has a fixing date and a settlement (delivery) date. The fixing date is the day and time whereby the comparison between the NDF rate and the prevailing spot rate is made. The settlement date is the day whereby the difference is paid or received.

As it is a "cash settlement" instrument, there is no movement of the principal amounts of the two currencies contracted. The only movement is the settlement amount representing the difference between the contracted NDF rates and prevailing spot rate. Hence, NDFs are "non-cash" products, which are off the balance sheet and as the principal sums do not move, possess very much lower counterparty risks.

NDFs are committed short-term instruments. Both the counterparties are committed and are obliged to honor the deal. Of course, the user can cancel an existing contract by entering into another offsetting deal at the prevailing market rate.

The more active banks will quote NDFs from between one month to one year, although some will quote up to two years upon request. Odd-dated NDFs can also be requested. It should also be noted, that NDFs are quoted with the dollar as the reference currency, that is they are quoted in terms of dollars against other third currencies and the settlement is also in dollars.

Without an NDF, an investor who wanted to take advantage of the type of enhanced yields available in the emerging markets would have to do the following:

Buy the spot currency and sell dollars.

Invest in a local risk-free asset (that is, government bond).

Fund the dollars at the London Interbank Offered Rate (LIBOR).

At maturity, the investor receives the capital plus interest.

Sell the currency on the spot market and purchase dollars.

A foreign exchange swap is the simultaneous purchase and sale of one currency against another for two different value dates. Usually, one of the value dates is the spot date and the other is a date in the future. In a typical swap transaction, one currency amount is held constant for both dates of the transaction. Most foreign exchange swaps have a maturity less than one year. In addition, a forward/forward is a swap where both the near date and the end date are forward dates.

In fact, a swap may be most easily understood as simply the combination of a spot and a forward, or the combination of two forwards. It can be the combination of a purchase with a simultaneous forward sale or a sale with a simultaneous forward purchase. Like forward contracts, swaps are regularly for periods of 1,2,3, 6, and 12 months from the spot value date. Frequently, however, the date is customized to meet a client's needs.

Forward contract prices are determined, as before, by the current spot price between the two currencies and the interest rates prevailing in each of the two countries. For example, a company could sell dollars and buy Swiss francs spot, and buy dollars and sell Swiss francs 3 months forward. The cash flows in such an exercise are similar to borrowing one currency (Swiss francs) and investing in another (dollars). The exposure to the company is one of interest rate risk rather than currency risk. Consequently, banks will only charge, or pay, the interest differential.

Swaps are used primarily by investors and borrowers, and for cash management purposes. They are valuable to those who have liquidity in one currency but need liquidity in another currency. Typically, a client will buy spot and sell forward to generate liquidity in the currency purchased at spot. That is, if a client exchanges dollars for francs at spot and simultaneously exchanges francs forward for dollars, the client has created liquidity in francs (that is, has them to spend) until the forward date. A foreign exchange swap is an alternative to straight borrowing in a foreign currency.

A swap allows the two parties involved to use a currency for a period in exchange for another currency not needed at that time. For example, companies can access foreign currency to finance foreign currency denominated assets, such as those of a foreign subsidiary. Hence, foreign exchange swaps can help clients to diversify their investments, to fund intracompany loans, to fund a position rather than use the money markets, to potentially improve the yield with no exchange risk in conjunction with a foreign currency investment, and to minimize borrowing costs in certain cases by using a swap rather than straight borrowing in a foreign currency. In such a contract, the exposure is therefore one of interest rate risk rather than currency risk. Consequently, market makers will only charge, or pay, the interest differential. In the swap market, this interest differential is expressed, again, in points or pips.

The formula for determining the interest rate differential underlying the swap pips is:

where:

| C = currency interest rate |

| T = period in number of days |

| S = swap pips as a decimal added or deducted |

| B = outright forward rate |

Consider the following quotation:

Spot USD/CHF | 1.4791 | 1.4796 |

3-month forward points | 25.5 | 24.5 |

3-month dollar deposit | 1.72% | 1.82% |

3-month Swiss franc deposit | 1.09% | 1.17% |

In order to choose the number of points to be applied in the swap, analyse the cash at maturity. Assume, the company is buying dollars and selling Swiss francs, which are the right hand side of a foreign exchange quote, so the number of points is 24.5. The number of points represents the interest differential when borrowing Swiss francs and investing dollars. Similarly, 25.5 points represents the interest differential when borrowing dollars and investing Swiss francs.

There are two points to note about swaps. First, as the swap pips determine the price of the swap, the spot rate used is less important. In practice, market makers tend to use the middle rate when actually processing the swap transaction. The key point to note is that whichever spot rate is chosen, the forward rate is determined by adjusting that spot rate by the swap pips. Second, the amount of one currency in a swap is kept constant. Typically, this is the dollar, thus the same amount of dollars is sold and bought in the transaction.

As mentioned before, swaps are undertaken together with a money market operation to take advantage of imperfect exchange rate and interest rate differentials. This is particularly of use to companies, which have a borrowing advantage in one currency or type of facility over another (that is, acceptance facility).

Swaps are also used where the domestic money market may not offer the necessary investment possibilities. For example, the smaller Swiss companies and wealthy private clients place short-term Swiss franc deposits with the Swiss banks domestically. Since there is a shortage of domestic money market instruments in which to invest these deposits, the Swiss banks may place them abroad, mainly in dollars, through swaps.

Finally, a swap can be used to hedge exposure. For example, a client wishes to buy Japanese yen against dollars three months forward. The bank can cover the obligation to provide the JPY by purchasing spot and undertaking a three-month dollar against JPY swap, giving up the use of JPY, but getting the use of dollars for the period. At maturity, the bank uses the Japanese yen received under the swap to meet the obligation to the client, and the dollars received from the client to meet the dollar obligation under the swap. Alternatively, a client can use a swap to roll a hedge forward. For example, the client may have entered into a contract to buy Swiss francs against dollars forward. If, in three-months time, the dollars do not materialize, the hedge would be extended. This can be achieved using a swap, whereby the original forward is closed out by the spot transaction and the exposure is covered by the forward transaction.

A swap is an agreement between two counterparties to exchange future cash flows. There are two fundamental types of swap; the cross-currency, which involves the exchange of cash flows in one currency for those in another with an agreement to reverse that transaction at a future date and the interest rate (single-currency) swap, which changes the basis on which income streams or liabilities are received or paid on a specified principal amount.

From a foreign exchange point of view, the cross-currency swap is much more relevant, as they allow companies to borrow in the most efficient market, usually in one in which the company have not borrowed too heavily in the past. The major difference between cross-currency swaps and currency forwards is that there is only one contract in the case of swaps, whereas forwards require separate contracts for each payment of interest and principal.

An interest rate swap is exclusively concerned with the exchange of cash flows relating to the interest payments on the designated notional amount. However, there is no exchange of notional at the inception of the contract. The notional amount is the same for both sides of the currency and it is delineated in the same currency, that is, principal exchange is redundant.

In the case of a currency swap, however, principal exchange is not redundant. The exchange of principal on the notional amounts is done at market rates, often using the same rate for the transfer at inception as is employed at maturity.

For example, consider an American-based company that has raised money by issuing a Swiss franc denominated Eurobond with fixed semiannual coupon payments of 6% on CHF 100 million. Up front the company receives CHF 100 million from the proceeds of the Eurobond issue. In essence, they are using the Swiss francs to fund their American operations. Because this issue is funding American based operations, the company is going to have to convert the CHF 100 million into dollars. This can be done by entering into a currency swap whereby the Swiss franc debt can be converted into a dollar like debt.

The American company can agree to exchange the CHF 100 million at inception into dollars, receive the Swiss franc coupon payments on the same dates as the coupon payments are due to the company's Eurobond investors, pay dollar coupon payments tied to a preset index and re-exchange the dollar notional into Swiss francs at maturity.

Thus, lays the fundamental difference between a currency swap and the classic foreign exchange swap. During the life of the transaction, each currency bears an agreed rate of interest, which is usually paid or received at intervals.

Under a foreign exchange swap, no interest is payable on either currency. Rather, the price at which the currencies will be exchanged at maturity takes account of the interest differential between the two. Thus, if sterling rates for one year are at 5% and the dollar rates are at 2%, the theoretical forward exchange rate between the two currencies is 3% less than the spot rate prevailing. Under a one-year currency swap between the two, the rate for the reexchange at the end of one year will be the same as that used at the start, but interest will be payable or receivable on each currency. In the simple case of a one-year swap between two currencies at a fixed rate of interest the two techniques are little different. Consider, however, a five-year traditional foreign exchange swap between dollars and Swiss francs. The forward foreign exchange rate will represent the compounded interest rate differential between the two currencies and only two cash flows will occur, namely the spot transaction and the forward leg in five years, at a radically different exchange rate.

Under a currency swap between dollars and Swiss francs for five years, an amount of each currency would be exchanged at the start (determined by the spot rate prevailing), the party receiving the francs would pay an agreed interest rate periodically, as would the party receiving the dollars. At the end of five years, the same amount of each currency would be reexchanged. There is no need for the rate of interest applicable to each currency to be on a fixed basis, it can be a floating rate tied to LIBOR, for example. Indeed, the vast majority of currency swaps currently transacted are between dollars at six months LIBOR and another currency at a fixed rate of interest, payable either biannually or annually as agreed between the two parties.

Currency swaps give companies extra flexibility to exploit their comparative advantage in their respective borrowing markets. Also, currency swaps allow companies to exploit advantages across a matrix of currencies and maturities.

The currency swap market has become a liquid and cost-effective market for corporate treasurers to achieve long-term currency hedges for their liabilities. Today, one of the most common transactions in the currency swap market is that related to a capital market debt issue, which is then swapped in its entirety to another currency that the borrower requires. Also, an interesting application of the currency swap has been to generate foreign exchange prices by combining two or more zero-coupon swaps against floating-rate dollars, which cancel out the floating-rate flows and leave one with an exchange of a given amount of one currency against another at a future date, which is precisely similar to a long-term foreign exchange transaction. Under a zero-coupon swap, the fixed rate interest payable/receivable is not paid until maturity and is compounded at the same time as it is paid.

Because of the exchange and reexchange of notional principal amounts, the currency swap generates a larger credit exposure than an interest rate swap.

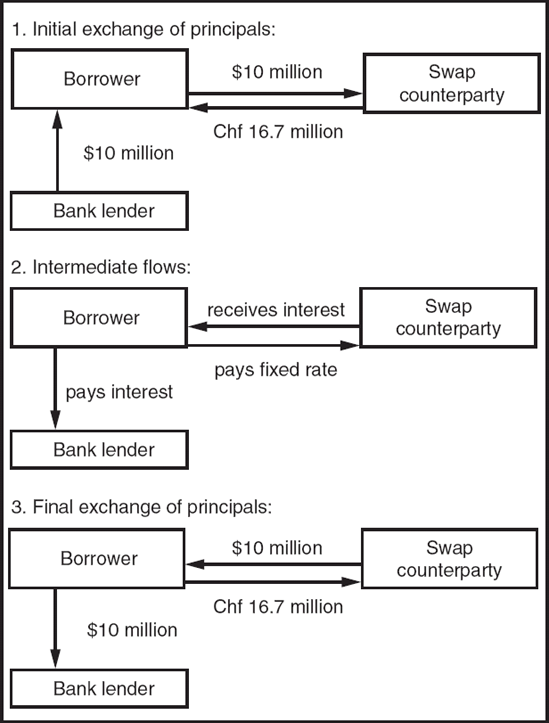

Graphically, a currency swap can be shown by the three stages in Figure 65.2.

Although futures contracts on commodities have been traded on organized exchanges since the 1860's, financial futures are relatively new, dating from the introduction of foreign currency futures in 1972. The basic form of the futures contract is identical to that of the forward contract, whereby a futures contract obligates its owner to purchase a specified asset at a specified exercise price on the contract maturity date. Likewise, currency futures are defined as a standardized contract/agreement to sell or buy a specific amount of a currency at a particular price on a stipulated future date.

In fact, futures developed in response to the substantial volatility for currency trading that occurred following the 1971 shift from fixed to flexible currency exchange rates.

In brief, buyers and sellers of foreign exchange futures are required to post initial margin or security deposits for each contract. Participants also have to pay brokerage commissions that can be fixed or negotiated depending on the size of the trade. Foreign exchange futures are only traded on regulated exchanges. In general, futures are used by banks, commodity trading advisors and arbitrage houses, that is, by "professional" traders rather than by corporations.

Like a forward contract, the futures contract has two-sided risk. However, in marked contrast to forwards, credit or default risk can be virtually eliminated in a futures market. Firstly, instead of conveying the value of a contract through a single payment at maturity, any change in the value of a futures contract is conveyed at the end of the day in which it is realized. For example, suppose that, on the day after origination, the financial price rises and, consequently, the financial instrument has a positive value. In the case of a forward foreign exchange contract, this value change would not be received until maturity. With a futures contract, this change in value is received at the end of the day. In the language of the futures markets, the futures contract is cash-settled or marked-to-market daily.

Since the value of the futures contract is paid or received at the end of each day, a futures contract can be likened to a series of forward contracts. That is, a futures contract is like a sequence of forwards in which the forward contract written on day 0 is settled on day 1 and is replaced, in effect, with a new "forward" contract reflecting the new day 1 expectations. This new contract is itself settled on day 2 and replaced, and so on until the day the contract ends. In other words, a futures contract can be thought of as "rolling over" a forward contract on a daily basis. Strictly speaking, the futures price and the forward price are not quite the same but as a practical matter they are so close that little accuracy is lost in viewing them as identical. Therefore, analogous to forward contracts, the futures price is that contract price which results in the futures contract having zero value to both the buyer and the seller each day the contract is settled and refix.

All market participants, sellers and buyers alike, post a performance bond (that is, margin). If a futures contract increases in value during the trading day, this gain is added to the margin account at the end of the day. Conversely, if the contract loses value, this loss is deducted from the margin account. If the margin account balance falls below some agreed-upon minimum, the holder will be required to post additional bond. Hence, the margin account must be replenished or the holder's position will be closed out.

There are two types of exchange members who can trade any futures contract. First, there are commission brokers, or floor brokers, who execute orders for nonmembers. These orders from nonmembers will originate through futures commission merchants, which are organizations, for example, brokers and commercial banks. These types of organizations will solicit orders for futures trading. Futures commission merchants also hold their clients margin monies and handle all margin accounting. The floor broker executing the order may or may not be affiliated with the futures commission merchant, which originated the order.

The other type of exchange member who will be trading the futures contract is called a "local" who is simply an individual trading for his or her own account. Essentially, locals are willing to hold positions, inter- or intraday, acting much like a market maker who hopes to profit from the bid/offer spread or market moves.

An important feature of an organized futures exchange is the Clearing Corporation. Essentially, the Clearing Corporation interposes itself as the seller to every buyer and the buyer to every seller. In other words, the Clearing Corporation becomes the counterparty to every trade, guaranteeing the opposite side of every transaction. This has several attractive features:

The buyer of a futures contract need not be concerned with the creditworthiness of the seller. If the buyer's position is doing well, that is, the futures price is rising, then the buyer is guaranteed the daily receipt of the variation margin by the Clearing Corporation, independent of whether the original seller was able to pay that same variation margin. In this example, the Clearing Corporation looks to the member firm, who originated the futures sale, for the timely payment of the daily variation margin independent of whether the original seller has paid in sufficient margin into the account.

The other major advantage of the Clearing Corporation from the viewpoint of the member firms is that the margin accounting problem is significantly simplified. There is now only one entity with which the member firm must deal in settling margin calls, as opposed to having to exchange monies with all other member firms.

In addition, the Clearing Corporation will net out all margin calls and receipts for a single member firm across all of their positions, such that only one net amount of funds must be transferred at the end of each trading day.

The major exchanges for financial futures include the Chicago Board of Trade (CBT), the Chicago Mercantile Exchange (CME), the International Monetary Market (IMM), the London International Financial Futures Exchange (LIFFE), the New York Futures Exchange (NYFE), and the Kansas City Board of Trade (KC).

Generally, in the foreign exchange market, currencies are quoted against the American dollar. For example, a rate of 1.67 Swiss francs per dollar means that it takes 1.67 francs to buy/sell 1 dollar. Of course, there are the exceptions to this rule, for example sterling. However, currency futures are priced in American terms, in that it quotes how many dollars it takes to buy one unit of foreign currency. They are the reciprocal of those used in the cash market. Thus, a rate of 1.67 francs per dollar would be quoted in the futures market as 0.5988 dollars per franc (1 divided by 1.67), which means it costs 60 cents to buy one franc. For each contract, there is a specific contract size, for example, one Swiss franc contract is worth 125,000 francs, the Japanese yen is worth 12,500,000 yen, and sterling is worth 62,500 pounds, while the euro is worth 125,000 euros.

The minimum price movement of a currency futures contract is called a tick. The value of a tick is determined by multiplying the minimum tick size by the size of the contract. For example, using the Swiss franc against the dollar, one point is $.0001 per Swiss franc, which equals $12.50 per contract, while one-point sterling is worth $.0001 per pound, which equals $6.25 per contract. The contract trading months are on the same quarterly cycle as other financial instruments: March, June, September, and December. They are also known as the delivery months, because the seller of a contract must be prepared to deliver the specified amount of foreign currency to the buyer if the seller has not cancelled the obligation with an offsetting purchase. It must be said that the vast majority of market participants close out their positions before delivery.

Table 65.1. Summary of Contract Specifications for Currencies against the Dollar Futures

Product | Trading Unit | Point Description |

|---|---|---|

Australian dollar | 100,000 dollars-physically delivered | 1 point = $0.0001 per dollar = $10.00 per contract |

Brazilian real | 100,000 real-cash settled | 1/2 point = $0.0005 per real = $5.00 per contract |

British pounds | 62,500 pounds-physically delivered | 1 point = $0.0001 per pound = $6.25 per contract |

Canadian dollars | 100,000 dollars-physically delivered | 1 point = $0.0001 per dollar = $10.00 per contract |

Euro | 125,000 euro-physically delivered | 1 point = $0.0001 per euro = $12.50 per contract |

Japanese yen | 12,500,000 yen-physically delivered | 1 point = $0.000001 per yen = $12.50 per contract |

Mexican peso | 500,000 peso-physically delivered | 1 point = $0.00001 per peso = $5.00 per contract |

New Zealand dollars | 100,000 dollars-physically delivered | 1 point = $0.0001 per dollar = $10.00 per contract |

"New" Russian rouble | 2,500,000 rouble-cash settled | 1 point = $0.00001 per rouble = $25.00 per contract |

South African rand | 500,000 rand-physically settled | 1 point = $0.00001 per rand = $5.00 per contract |

Swiss franc | 125,000 franc-physically delivered | 1 point = $0.0001 per franc = $12.50 per contract |

Swedish krona | 2,000,000 krona-physically delivered | 1 point = 0.00001 dollar/krona = $20.00 per contract |

Norwegian krone | 2,000,000 krone-physically delivered | 1 point = 0.00001 dollar/krone = $20.00 per contract |

The contract specifications for currencies against the dollar futures are shown in Table 65.1. There are, of course, contracts for crosses as well.

An exchange for physical (EFP) refers to exchanging a physical (cash) position for a futures position. This is where a spot interbank transaction can be converted into a futures position via an exchange for physical. Consequently, when a cash position is exchanged for a future position, the EFP is simply a mechanism by which the cash position is converted to its IMM or Finex equivalent. The EFP represents the current spot (cash) price plus or minus the interest rate differential (cost of carry) between the two currencies, expressed in the futures price and it is essentially an ex-pit transaction.

The mechanics of an EFP transaction would be where on, say December 13, the interbank spot price for francs for value December 15 is 1.6700 bid-offer 1.6705. The market user sells 25 million francs at 1.6705 for value December 15 and then decides to convert the short cash position of 25 million francs to the IMM equivalent for short contracts for March. Assume the forward pips for three months $/CHF is 1.7/1.9. The resulting transaction can be viewed as:

| Buys 25 million CHF at 1.6705 value December 15 |

| Sells 200 March IMM contracts at 0.5986 |

| (1.6705 plus 1.9 = 1.67069 and then 1 divided by 1.67069 giving 0.5986) |

The result for the cash position is:

| Short 25 million CHF at 1.6705 value December 15 |

| Long 25 million CHF at 1.6705 value December 15 |

so that the net cash position is flat and the market user is left with an open IMM futures position of being short 200 March IMM futures contracts at 0.5986.

On December 13, the interbank spot price for British pounds for value December 15 was 1.5000 bid-offer 1.5005. The trader sells 10 million pounds (equivalent of 160 IMM contracts) at 1.5000 value December 15. The trader decides to convert the short cash position of 10 million pounds to the IMM equivalent of short 160 contracts for March. The resulting transaction can be viewed as:

| Dealer interbank swap price for March 16 is 70-67, thus |

| the trader executes a simultaneous swap transaction. |

| Buys 10 million pounds at 1.5000 value December 15. |

| Sells 160 March IMM contracts at 1.4930 (1.5000 − 0.0070). |

Hence, the result is:

| Short 10 million pounds at 1.5000 value December 15 |

| Long 10 million pounds at 1.5000 value December 15 |

This results in a net cash position which is flat (square) and the trader is short 160 March IMM futures contracts at 1.4930.

In brief, the main points are that with the EFP execution, the client's spot cash position is flat. No profit or loss will be generated. The client will have a futures position at only one average price for the full amount traded. With the execution of the EFP, the futures price will be posted (reported) to the exchange and the client will receive a confirmation as they would an IMM or Finex transaction. Additionally, fees and commissions will be recorded in exactly the same manner as if the transaction was executed on any of the exchanges. Also, there are no commissions or fees charged on the cash side of the transaction.

Table 65.2. Differences Between Interbank Spot and Futures

Interbank Spot | IMM Futures |

|---|---|

Single counterparty risk | Counterparty risk with |

Unregulated market | exchange |

Tailored maturity dates | Regulated market |

Tailored currency amounts | Limited delivery months |

Greater liquidity | Specific contract specifications |

Single average price | Lower average volume |

No exchange fees | Multiple price fills |

No reporting levels | |

Unrealized gains can only be withdrawn upon maturity date |

A summary of the differences between interbank spot and futures is provided in Table 65.2.

There are now financial instruments that permit the direct transfer of financial price risk to a third party, who is more willing to accept that risk. At another level, the financial markets have evolved to the point whereby financial instruments can be combined with other instruments to unbundled financial price risk from the other risks inherent in the process, for example, raising capital.

Forwards provide certainty in the uncertain world of currency movements by locking in a specific rate, and as the forward markets are quite liquid, the bid/offer spreads are low. The interest rate differential between the dollar and another currency is expressed in points, which are fractions of that currency's exchange value against one dollar. In terms of short- and long-dated contracts, the principal is the same as with regular forward rates and is again made on the basis of interest rate gain or loss. The exception to the rule, in the case of short-dated contracts, is that prices normally added on are deducted and prices normally deducted are added. This, actually, is not as odd as it sounds. If prices are normally quoted for spot delivery and a value tomorrow quote means the market maker will have to surrender dollars earlier than normal, there has to be some compensation for it.

An NDF is a short-term committed forward "cash settlement" currency derivative instrument. It is essentially an outright (forward) foreign exchange contract whereby on the contracted settlement date, profit or loss is adjusted between the two counterparties basing on the difference between the contracted NDF rate and the prevailing spot foreign exchange rates on an agreed notional amount. The NDF rate is the rate agreed between the two counterparties on the transaction date. This is essentially the outright (or forward) rate of the currencies dealt. The notional amount is the face value of the NDF, which is agreed between the two counterparties. It should again be noted that there is never any intention to exchange the two currencies principal sums—the only movement is the difference between the NDF rate and the prevailing spot market rate and this amount is settled on the settlement date.

Every NDF has a fixing date and a settlement (delivery) date. The fixing date is the day and time whereby the comparison between the NDF rate and the prevailing spot rate is made. The settlement date is the day whereby the difference is paid or received. As it is a cash settlement instrument, there is no movement of the principal amounts of the two currencies contracted. The only movement is the settlement amount representing the difference between the contracted NDF rates and prevailing spot rate. Hence, NDFs are noncash products, which are off the balance sheet and as the principal sums do not move, possess very much lower counterparty risks.

NDFs are committed short-term instruments. Both the counterparties are committed and are obliged to honor the deal. Of course, the user can cancel an existing contract by entering into another offsetting deal at the prevailing market rate.

The more active banks will quote NDFs from between one month to one year, although some will quote up to two years upon request. Odd-dated NDFs can also be requested. NDFs are quoted with the dollar as the reference currency, that is they are quoted in terms of dollar against other third currencies and the settlement is also in dollars.

Without an NDF, an investor who wanted to take advantage of the type of enhanced yields available in the emerging markets would have to buy the spot currency and sell dollars; invest in a local risk free asset (that is, government bond); fund the dollars at LIBOR; at maturity, receive the capital plus interest; and sell the currency on the spot market and purchase dollars.

Swap risks are almost identical to those for forwards. A swap effectively becomes a forward once the near date has settled. The difference between a forward and a swap is that to do a swap there must be two transactions in opposite directions at different times. The currency swap market has become a liquid and cost-effective market for corporate treasurers to achieve long-term currency hedged for their liabilities. Today, one of the most common transactions in the currency swap market is that related to a capital market debt issue, which is then swapped in its entirety to another currency that the borrower requires. Also, an interesting application of the currency swap has been to generate foreign exchange process by combining two or more zero-coupon swaps against floating-rate dollars, which cancel out the floating-rate flows and leave one with an exchange of a given amount of one currency against another at a future date, which is precisely similar to a long-term foreign exchange transaction. Under a zero-coupon swap, the fixed rate interest payable/receivable is not paid until maturity and is compounded at the same time as it is paid. Because of the exchange and reexchange of notional principal amounts, the currency swap generates a larger credit exposure than an interest rate swap.

A foreign exchange futures contract is a forward contract for standardized currency amounts and for standard value dates. Buyers and sellers of foreign exchange futures are required to post initial margin or security deposits for each contract. Participants also have to pay brokerage commissions that can be fixed or negotiated depending on the size of the trade. Foreign exchange futures are only traded on regulated exchanges. In general, futures are used by banks, commodity trading advisors and arbitrage houses, that is, by professional traders rather than by corporations.

The main point to remember with the EFP execution is that the client's spot cash position is flat. No profit or loss will be generated. The client, however, will have a futures position at only one average price for the full amount traded. The EFP transaction is posted on the required exchange. Also, there are no commissions or fees charged on the cash side of the transaction.

Henderson, H. (2002). Currency Strategy: The Practitioner's Guide to Currency Investing, Hedging and Forecasting. West Essex, UK: John Wiley & Sons.

Horner, R. (2006). 30 Days ofForex Trading—Trades, Tactics and Technique. Hoboken, NJ: John Wiley & Sons.

Martinez, J. (2007). The 10 Essentials ofForex Trading. New York: McGraw Hill.

Oberlechner, T. (2004). The Psychology of the Foreign Exchange Market. West Essex, England: John Wiley & Sons.

Rosenstreich, P. (2005). Forex Revolution: An Insider's Guide to the Real World of Foreign Exchange Trading. Upper Saddle River, NJ: Financial Times Prentice Hall.

Shamah, S. (2003). A Foreign Exchange Primer. London: Wiley Finance.

Steiner, R. (2002). The Foreign Exchange and Money Markets: Theory, Practice and Risk Management. Oxford: Butterworth-Heinemann.

Taylor, F. (2004). Mastering Foreign Exchange and Currency Options: A Practical Guide to the New Marketplace-Second Edition. Upper Saddle River, NJ: Financial Times Prentice Hall.

Walmsley, J. (2000). The Foreign Exchange and Money Markets Guide. Hoboken, NJ: John Wiley & Sons.

Weithers, T. (2006). Foreign Exchange: A Practical Guide to the FX Markets. Hoboken, NJ: John Wiley & Sons.