MOORAD CHOUDHRY, PhD

Head of Treasury, KBC Financial Products, London

Abstract: The excess of demand over supply for specific tranches of structured finance transactions such as asset-backed securities and mortgage-backed securities has led to investors' accessing these assets via the credit default swap market. A credit default swap written on an asset-backed security possesses different contract mechanics to a standard credit default swap written on a corporate reference name. The main differences relate to the list of occurrences that constitute a credit event and the settlement mechanics whenever the underlying tranches of an asset-backed security or mortgage-backed security experience a paydown or other prepayment.

Keywords: asset-backed security (ABS), mortgage-backed securities (MBSs), cash settlement, credit default swaps (CDSs), credit event, pay-as-you-go, physical settlement, structured finance securities

Credit derivatives were first introduced during the 1990s, initially as a risk management tool for banks seeking to manage and transfer the credit exposure of their loan books. They have since developed into an asset class in their own right, in synthetic form, and in some cases are preferred to the cash version of an asset where the latter is in short supply or otherwise illiquid. The advent of a liquid and transparent market in credit derivatives has meant that investors are now looking at synthetic access to the asset-backed security (ABS) market. In this chapter we describe the form of credit default swaps (CDSs) written on structured finance securities such as ABSs and mortgage-backed securities (MBSs), and their trading and settlement mechanics, which differ from CDSs written on plain vanilla bonds.

Credit derivatives markets have expanded rapidly since the first instruments were introduced in 1994. They have now been extended into the asset-backed and mortgage-backed markets, mainly due to the shortage of paper in the cash market. The standardization of CDS contracts and trading terminology also facilitated the expansion of credit derivatives into structured finance markets.

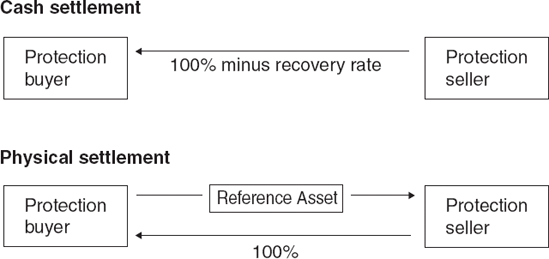

There are a number of detail differences between ABS credit risk and corporate credit risk. A single-name corporate CDS transacted under the standard 2003 International Swaps and Derivatives Association (ISDA) Credit Derivatives definitions (www.isda.org) will be based on clearly defined trigger events ("credit events") and a transparent process of settlement, either physical or cash settlement. The settlement process for standard CDSs is shown as Figure 36.1. A CDS written on an ABS can present problematic issues with regard to both of these items. Corporate CDS trigger events are, following some initial problems with definitions, straightforward to describe. They include bankruptcy, failure to pay, debt restructuring, and, in some cases, ratings downgrade. Such occurrences can be identified easily in most cases. Also, the outstanding debt of a corporate entity can be expected to trade at roughly the same level in the event of issuer default, irrespective of coupon or maturity.

Structured finance securities such as ABSs and MBSs differ in both these respects. The key difference is that, unlike corporate bonds, most ABSs are issued by special purposes vehicles (SPVs), bankruptcy-remote legal entities created solely for the purpose of facilitating the bond issue. Bankruptcy and restructuring rarely if ever, apply to SPVs. Also, it may be less clear in the case of an SPV that there has been a failure to pay. Unlike corporate entities, credit ratings of SPVs are based essentially on the quality of the underlying assets. The repayment of these assets is not known with certainty, which is why ABS bonds are given long legal final maturities. Other issues that complicate the matter of CDSs on ABSs include the following:

ABS structures with an element of uncertain cash flow patterns include the provision for the write-down of principal in the event of losses. This does not always constitute a "default" as the write-down can be reversed and made good later.

Many ABS structures allow for a delay in interest payment, for example, during a time when the excess spread in the vehicle has been reduced. Again, this may not constitute default and may not necessarily lead instantly to a ratings downgrade, as the interest coverage may be expected to become sufficient again.

The structure represents a distinct pool of assets, ring-fenced within the SPV. This contrasts with the general pool of assets represented in a corporate entity.

It is quite possible for the more junior tranches of an ABS issue to be in default while the senior tranches are not, again representing the way the asset pool is performing.

The significant difference, therefore, between an ABS CDS and a single-name corporate CDS is that the former is written against a specific security, while the latter is written at an entity level on a corporate name. However, writing a contract on a specific security means that physical settlement on occurrence of a credit event is impractical. For this reason, physical settlement is not used. Cash settlement may also be problematic because of the difficulty with ascertaining the market value of the ABS tranche. A different type of CDS, the pay-as-you-go CDS (PAUG CDS) has been developed for this market.

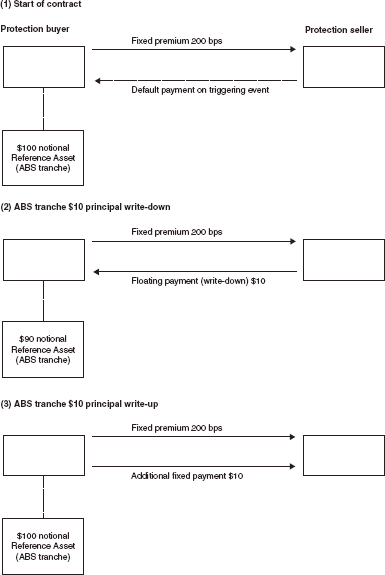

PAUG CDSs have been developed to meet the distinct requirements of synthetic investment in ABS issues. A PAUG CDS acts like a standard CDS, with provision for termination on occurrence of specified credit events. The protection buyer pays a fixed-basis-point fee to the protection seller, which is also standard. However, the PAUG contract also permits the following:

Payment of an additional floating payment from protection seller to protection buyer in the event of principal write-down.

Payment of a fixed payment from protection buyer to protection seller in the event of write-up.

Provision of altering cash flows in the event of interest shortfall of ABS vehicle.

To illustrate, consider the case where the performance of the underlying asset pool in an ABS, due to under-performance or default, means that the principal amount of one or more of the overlying note tranches must be reduced. This action would normally be undertaken by the Trustee or servicer to the transaction. The protection seller would make a floating payment to the protection buyer to cover this written-down amount. The CDS itself would not terminate. If at a later date the principal balance is reinstated, for example, because the portfolio performance has improved, the protection buyer would then make a fixed payment to the seller. Figure 36.2 illustrates the mechanics of a PAUG CDS in the event of write-down.

A standard CDS would generally cover the following credit events:

Failure to pay

Credit rating downgrade to sub-investment grade

Permanent write-down

A PAUG CDS would also cover the following without being terminated:

Principal write-down

Interest shortfall

Failure to pay principal

By incorporating this flexibility, investors are better able to gain a realistic exposure to the ABS market, albeit synthetically.

Generally, the protection sellers in the ABS CDS market include investors who would normally hold cash ABS bonds. This is marked when there is a shortage of paper in the cash market. The ability to short ABS tranches means that investors can also take a view on ABS credit; previously, this would not necessarily have been straightforward because of the illiquid nature of the ABS repo market. The differences between the corporate and ABS markets are mirrored in the synthetic market. Investors will be aware that corporate entities are dynamic corporations that are proactively able to avoid credit events, which is not the case with SPVs.

Synthetic ABS investors must therefore still be concerned primarily with the quality of the underlying collateral and the specific risk/return profile of the individual ABS tranche. Also, there is the issue of prepayment uncertainty. Most corporate bonds have a bullet maturity or fixed redemption date. Nonredemption would constitute a credit event. ABS securities, however, amortize over time, with the redemption date not known with certainty. (For analysis purposes, the "average life" of the ABS note is used; this figure is an estimated repayment term based on an assumed level of prepayments). However, the nonredemption of a tranche in accordance with an average life estimate would not be deemed a credit event.

ABS tranches experience a declining notional balance over time as principal is repaid in stages in the underlying asset pool, due to prepayments and other factors. The outstanding notional value of ABS tranches therefore reduces over time; investors would observe this also occurring with ABS CDS contract notionals, as they mirror the behavior of the cash bond.

In theory, the basis between a PAUG CDS and its reference cash bond should be small because the contract mirrors the profile and behavior of the cash bond closely. (See Choudhry [2004b] for more detail on the CDS basis.)

In practice, a number of market and structural factors cause the cash and synthetic markets to trade at a negative or positive basis. These include the following:

In the synthetic market, the investor is exposed additionally to counterparty risk, as it is the counterparty that is paying the coupon (CDS premium). The cash investor is exposed to the quality of the reference collateral only.

The ABS CDS is an unfunded instrument and so carries no funding cost; this is an additional factor in relative value analysis.

Supply-and-demand factors may be more prevalent in the synthetic market, as the availability of protection buyers may be limited. (Unlike ABS transaction originators in the cash market, there is no natural market for protection buyers in the ABS CDS market outside market makers.)

As a relatively new market as of this writing, the depth and transparency of the ABS CDS market may be limited for certain sectors. This should not be a problem once the market develops.

The liquidity and transparency of the credit derivatives market, together with the adoption of standard terms and contractual documentation, has resulted in the market's being straightforward for investors to access. Where there is a shortage of required assets in the cash bond market, investors are able to access the same name in the credit derivative market. One asset class where this manifests itself is in the structured finance market, where specific tranches of ABS and MBS transactions are often in short supply or illiquid. Investors can access these tranches via a CDS written on the specific tranche. Such contracts differ in certain technical aspects from CDSs written on conventional bullet bonds. This includes the events that form a credit event, and the way that contract notionals are adjusted after a pay-down on the underlying reference tranche.

Choudhry, M. (2004a). Structured Credit Products: Credit Derivatives and Synthetic Securitisation. Singapore: John Wiley & Sons

Choudhry, M. (2004b). The credit default swap basis: Analysing the relationship between cash and synthetic markets. Journal of Derivatives Use, Trading and Regulation 10,1: 8-26

Das, S. (2006). Credit Derivatives, CDOs, and Structured Credit Products, 3rd edition. Singapore: John Wiley & Sons.

Deacon, J. (2004). Global Securitisation and CDOs. Chichester, UK: John Wiley & Sons.

Fabozzi, F. J., and Choudhry, M. (eds.) (2004). The Handbook of European Structured Financial Products. Chichester, UK: John Wiley & Sons.