WILLIAM L. MESSMORE

Vice President, Lehman Brothers

BETH STARR

Managing Director, Lehman Brothers

SUNITA GANAPATI

MARK RETIK

PAUL PULEO

Abstract: Catastrophe bonds represent a growing class of structured insurance risk products that offer returns that are linked to the occurrence of catastrophic events such as earthquakes and hurricanes. These securities can provide investors with diversification from corporate and asset-backed securities at comparable or wider spreads. Issued through special purpose vehicles, these bondlike securities are usually rated and offer an opportunity to participate directly in catastrophe risk with the benefit of an active secondary market. Investing in catastrophe risk can also improve the risk-return profile of a diversified portfolio of assets because this risk is generally uncorrelated with general credit and interest rate risk present in other securities markets.

Keywords: catastrophe bonds (cat bonds), sidecars, attachment point, trigger, extreme mortality securities, collateralized debt obligation (CDO), synthetics, industry loss warranties (ILWs), shelf issuance programs

The need for additional reinsurance capacity following Hurricane Andrew (1992) and the Northridge earthquake (1994), which in combination produced $27 billion in industry-wide insured losses, encouraged insurers to seek a new form of reinsurance protection. Driven by a particularly catastrophic 2005 U.S. wind season with Hurricanes Katrina, Rita, and Wilma, insurance companies faced capacity and pricing constraints in the broader reinsurance market and further turned to the capital markets to transfer risk. In exchange for a reinsurance premium (that is, interest on the securities), investors in catastrophe bonds (cat bonds) assume financial exposure to the risk that a catastrophe will strike and will be severe enough to exceed a certain trigger level. If such a catastrophe occurs, cat bond investors would receive a reduced yield and lose part or all of their principal; the insurer would receive a reinsurance claim payment. By transferring catastrophe risks to the capital markets in this manner, insurance companies are supplementing their use of traditional reinsurance and internal loss management mechanisms to reduce volatility in their financial statements and preserve overall liquidity.

In this chapter, we discuss catastrophes and the role that reinsurance has traditionally played in mitigating catastrophic losses. We describe developments in the capital markets that have led to catastrophe risk securitization and outline typical cat bond structures. We consider the third-party modeling analyses that accompany each cat bond and the related rating agency approaches. Finally, we discuss new risk-transfer products and market developments.

Reinsurance gives an insurer the ability to transfer risk with the primary purpose of either smoothing its income stream or protecting its balance sheet. Catastrophe management is an essential component of a reinsurance program for large property insurers. Insurance companies structure their reinsurance coverage according to their internal risk tolerance, corporate ratings targets, and cost considerations. Traditional reinsurance market coverage comes on an unsecured basis and became particularly costly after the 2005 U.S. wind season due to reduced amounts of capital available. Rating agencies instituted more stringent ratings criteria (particularly for extreme or "tail" risks), and the third-party risk-modeling firms reassessed U.S. hurricane risk, resulting in more conservative risk quantifications. Some of the largest reinsurance companies, most notably Swiss Re and Hannover Re, have turned to the capital markets to buy protection on their underlying books of business.

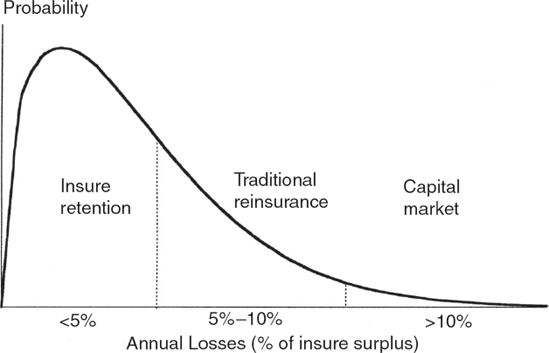

Catastrophe risk can be viewed as composed of layers of risk from events with decreasing probability of occurrence and increasing magnitude of losses. Historical and sophisticated modeling analyses indicate that catastrophic events occur at mostly unpredictable intervals and that less severe catastrophes occur with greater frequency. Risk management of catastrophe losses varies from one insurer to another. Figure 37.1 shows a probability distribution of insured losses and the sources of risk capital that an insurer may use to manage its catastrophe exposure.

Catastrophes resulting in gross insured losses of less than 5% of a major property insurer's statutory surplus occur frequently and are assumed to be part of the normal course of business. Losses from these events are absorbed by an insurer's operating cash flow, policyholders' surplus, or "working layer" reinsurance program. Events that cause losses between 5% and 10% of surplus are generally covered by purchasing traditional reinsurance contracts.

As insurers have increased their use of advanced catastrophe modeling to predict losses, they have tended to purchase coverage equal to their probable loss under various severe loss scenarios or, at a minimum, for losses in excess of 10% of their capital. However, large insurers find that protecting their balance sheet against an infrequent but large catastrophe is often too expensive due to the concentration of risk and lack of capacity in the reinsurance industry for covering this type of risk. Reinsurers face the same constraints with respect to the overall exposure in retrocession market, which offers reinsurance to reinsurers. Therefore, insurers and reinsurers are seeking capital market solutions to bridge this gap in capacity and to create a more efficient risk transfer mechanism.

As insurers explore alternative solutions for gaining additional reinsurance coverage, they have participated in several creative capital market-related developments, including government initiatives, cat bonds, sidecars, industry loss warranties, and synthetic cat bonds.

In response to reduced property insurance availability after Hurricane Andrew and the Northridge earthquake, the U.S. and state governments created various funds to provide additional insurance capacity. These include the Florida Hurricane Catastrophe Fund and the California Earthquake Authority, among others. These funds are set up to access the capital markets immediately after an event to provide additional funding either directly to homeowners or to insurance companies.

The Florida Hurricane Catastrophe Fund was designed to provide additional reinsurance capacity to primary insurers writing homeowner policies in Florida. The fund has expanded its risk capacity to cover $32 billion in losses, which would be funded largely by assessments on future Florida insurance premiums in the event of a major hurricane. Critics maintain that the fund artificially depresses policyholder premiums, and in the event of a particularly catastrophic event, could ultimately put the burden of claims repayment on Florida taxpayers instead of distributing the risk among the worldwide insurance industry. Several primary insurers have curtailed their participation in the Florida market.

The California Earthquake Authority (CEA) has over $8 billion of claims-paying capacity in California. The program was designed to include a combination of letter-of-credit facilities, reinsurance policies directly from reinsurers, assessments from participating insurance carriers, tax-exempt earnings on its reserves, and the capital markets. CEA policies are written by participating primary insurance companies as an add-on to a customer's existing residential policy.

These special funds are expected to provide incremental capacity to the property-casualty industry and potentially bridge part of the gap in reinsurance supply.

Insurance risk securitization is the transfer or sale, in the form of an investment security, of part of the underwriting risks associated with a group of insurance policies. Insurance companies expect that insurance risk securitization will play a significant role in meeting the shortage in reinsurance capacity. Investing in cat bonds is akin to issuing a reinsurance contract where the investor covers the insurer for a fixed amount of losses over a specified value (the attachment point or trigger).

As with any capital market product, structures are still evolving. The cat bond universe covers a number of different peril types with customized loss trigger types. Dealers have been distributing securities that reference portfolios of insurance and reinsurance risks, known as sidecars, and managed collateralized debt obligation (CDO) technology has been utilized as well. In concert with the explosive popularity of derivative contracts in the credit markets, the cat market has seen several investors participate in synthetic catastrophe risk, using existing cat bonds as reference obligations, or writing derivative contracts that are linked to third-party estimates of a catastrophe's insured industry losses.

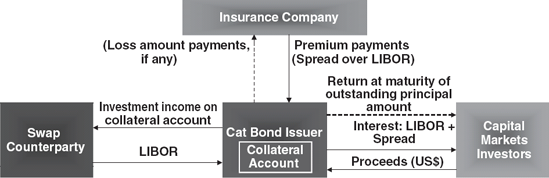

Cat bonds are issued for an expected maturity with the payment of coupon and retirement of principal dependent on the nonoccurrence of a catastrophic event with losses greater than a specified trigger during a defined risk or loss-occurrence period. As in other asset-backed transactions, the sponsor sets up a special purpose vehicle (SPV) that is bankruptcy remote. The vehicle is generally set up offshore for regulatory and tax reasons and issues securities that carry the risk of catastrophe losses over a specified level. It then issues a back-to-back reinsurance or derivative contract to the insurer, thus providing the loss protection.

The SPV invests cash raised from the issue in high-quality, liquid, fixed income instruments (typically AAA-rated securities). This portfolio is used to cover losses from events or to repay investors on maturity of the bond, and to provide a minimum rate of return (e.g., the London Interbank Offered Rate [LIBOR]). The return on the collateral account is guaranteed by a swap counterparty in the form of a total return swap on the assets. The catastrophe risk is transferred via a cash-collateralized reinsurance or derivative contract and, unlike traditional reinsurance contracts, does not carry any credit risk of the reinsurer. The coupon on the cat bond includes a spread over the minimum rate earned by the collateral account. The insurer pays the spread to the SPV, which passes through the total coupon payment to investors (see Figure 37.2).

The maturity of the security is based on the period during which a loss event can occur, called the risk period (or the loss occurrence period), and the time for computation of losses, called the development period. The development period may be up to two years, during which time the company works with a calculation agent to aggregate the final data surrounding the event, and inputs that data to determine whether a trigger event has taken place. The cat bond is usually structured to have a scheduled maturity date that can be extended for a maximum period equal to the development period (with reduced interest payments), thus exposing investors to some extension risk.

Cat bonds utilize a trigger structure that generally falls into one of four categories:

Parametric

Industry loss

Indemnity

Modeled loss

Parametric instruments rely on scientific readings surrounding an event: wind speeds, ground shake acceleration, or even measurements in flood recording stations. Typically, the data collected for the event are plugged into an index formula designed by the sponsor, and to the extent the output from that formula exceeds a certain predefined threshold ("attachment point"), the cat bond will suffer a principal loss. If the output exceeds a second threshold ("exhaustion point"), the cat bond will suffer a full principal loss.

For a cat bond using an industry loss trigger structure, principal losses occur if a third-party reporting agency's estimates of industry-wide insured loss for an event exceed a predetermined attachment point. Several sponsors have attempted to match their underlying books of business in their trigger formulas by applying weighted factors against the loss estimates, which are given on a state-by-state basis. A sponsor with concentrated obligations in the northeastern United States may build only those states into their trigger structure, and may further refine their coverage by making their loss trigger more sensitive to New York and less sensitive to Maryland, for example. Property Claim Services (PCS) is the most widely used third-party loss estimator for catastrophes in the United States.

From a risk perspective, the indemnity structure is less transparent than the parametric and industry loss structures, but it removes the basis risk between the insurer's underlying book of business and the cat bond coverage. In an indemnity structure, the insurance company receives a payout from the cat bond to the extent that the insurance company's book of business suffers losses above a certain attachment point. In a basic arrangement, the insurance company would retain the entire layer of losses up to the attachment point, and then retain a small pro-rata slice of the losses along with the cat bond; this pro-rata slice demonstrates to the cat bond investor that the insurance company retains an interest in its underwriting for the severe end of the risk spectrum. Protection on indemnity losses can be structured based on (1) losses from a single event (which has sensitivity to the severity of events) or (2) the aggregate annual losses from multiple events (which also has sensitivity to event frequency). Insurers may prefer indemnity structures because they are most similar to traditional reinsurance contracts, but the marketability of indemnity cat bonds relies on the insurance company's ability to demonstrate a strong and consistent underwriting history.

A variation on the indemnity trigger is the modeled loss trigger, where the sponsor designs and employs an escrowed loss model that inputs parametric data surrounding an event, and outputs an index value from the collected data. The modeled loss trigger is more transparent to investors than an indemnity structure because it limits the risk that underlying policy losses could occur that were not factored into the risk model used to evaluate an indemnity transaction. Therefore, in a modeled loss structure, the sponsor still retains some basis risk between their underlying book of business and the model output. However, an advantage to a modeled loss trigger is that the sponsor could receive a reinsurance payment immediately after data surrounding an event becomes available, instead of waiting for the underlying policy losses to develop and be aggregated.

The rating agencies have developed criteria for rating catastrophe-linked securities and furnish ratings on most transactions. At present, the methodology used by each agency is similar—though each is being continually refined, reflecting the relative newness and prospect for growth of this asset class. The presentation in this section is based on discussions with analysts at Standard & Poor's (S&P) and Moody's, along with publications on catastrophe-linked security rating approaches promulgated by the agencies.

The agencies rate cat bonds to reflect loss to both principal and interest. Because this approach is also used to rate corporate credits and asset-backed security structures, it is possible to draw conclusions on relative creditworthiness between these securities and catastrophe-linked securities based on ratings.

In analyzing cat bonds, the rating agencies consider structural and insurance risks. The structural analysis is essentially the same as the analysis used to rate any structured security. This analysis focuses on the transaction's legal structure; the quality of collateral; the bankruptcy-remote status of the SPV issuer; the flow of funds; and the market, counterparty, and legal risks inherent in the transaction.

Although structural risk is an important element in the rating methodology, the key risk that the rating agencies analyze is insurance risk. Cat bonds have their principal and interest at risk in that their calculated index value could exceed a predetermined attachment point.

There are several independent modeling firms that specialize in catastrophe modeling, and their models are utilized throughout the property and casualty (P&C) insurance industry for risk management purposes. Typically, each cat bond transaction will have an independent risk analysis that the issuer publishes as a part of the offering materials. Modeling firms EQECAT, AIR, and RMS maintain various models for different perils, including U.S. Hurricane, U.S. Earthquake, European Windstorm, Japanese Typhoon, Japanese Earthquake, and so on. These models rely on historical data, prospective climatological analysis, and topographic information to predict frequency, severity, and location of potential future events. Once the catastrophic events have been simulated, the modeling firms overlay data on insured values in order to estimate the damage applicable to the specific transaction (if applicable) and create a loss exceedance curve. Each structure has an estimated annualized probability of attachment, loss, and exhaustion, which gives investors the ability to assess a deal's risk against its offered yield, as well as against other cat bonds exposed to the same peril or perils.

The rating agencies rely on the results of simulation-driven catastrophe models to assign their ratings. The agencies first validate the analytic integrity of the model and test the quality of the insurance company data used by the model, if any.

These "stress tests" are conducted through a due diligence process. This process typically involves assessing the appropriateness of the probability distributions employed by the model to simulate catastrophe frequency and intensity. Both the underlying density functions and parameters are considered. Occasionally, a rating agency will request a modification of the probability distribution to generate more conservative results (e.g., it might ask to recalculate the insured loss distribution using twice the assumed catastrophe frequency).

In addition, property damage vulnerability relationships are examined. Vulnerability functions are considered for each property characteristic (e.g., construction type, elevation, building usage, etc.) using engineering and actuarial analysis. In all cases, consistency with published industry and academic literature is tested. Some rating agencies retain the services of outside meteorological or seismic experts to assist in evaluating the model.

For indemnity-triggered structures, the insurance company data used by the model are reviewed by the rating agencies for accuracy. These data include both the book of insured properties and the policy provisions in place on each property. Conservative adjustments are made to account for incomplete data.

Finally, certain indirect factors are sometimes also factored into the rating analysis. These include demand surge (the effect of a catastrophe on local prices for building materials and wages), growth and change of mix in the insured book of business over the course of the security's term, and the insurance company's claims handling and loss management/settlement procedures.

Cat bonds offer investors the unique opportunity to invest exclusively in catastrophe risk and may provide potential diversification benefits. Although investors can invest in catastrophe risks by buying insurance and/or reinsurance company equity and debt, these investments are not perfect substitutes for the pure catastrophe exposure inherent in cat bonds. First, cat bonds do not carry the idiosyncratic or nondiversifable risks associated with an investment in securities of an insurance or reinsurance company. Cat bonds also allow investors to avoid principal-agent risks (such as the risk that equity holders may have incentives to restructure the debt or increase the overall riskiness of the company, to the disadvantage of bondholders) inherent in a corporate security.

Second, the occurrence and magnitude of natural hazards are expected to be largely uncorrelated with movements in the stock and bond markets. However, insurance and reinsurance company securities do involve a significant systematic risk. A study by Canter, Cole, and Sandor (1996) show that a portfolio of 10 prominent catastrophe reinsurance companies has a strong positive correlation (beta of 0.83) with stock market movements. As a result, buying reinsurance company equity does not bring significant diversification benefits. In this respect, cat bonds offer better diversification opportunities since they are expected to have near-zero betas.

Modern portfolio theory asserts that an uncorrelated asset would be an attractive addition to a well-diversified portfolio even at the risk-free rate of return. If cat bonds offer returns in excess of the risk-free rate and do not exhibit systematic risk, then investing in these securities can improve overall portfolio performance on a risk-adjusted basis. Investors who purchase cat bonds can potentially receive an attractive expected return and improve the diversification of their current portfolio.

A study by Froot, Murphy, Stern, and Usher (1995) based on pricing and claims on actual catastrophe reinsurance contracts brokered by the reinsurance intermediary, Guy Carpenter & Company Inc., draws three valuable conclusions. First, the correlation of catastrophe risk with stocks and bonds is statistically indistinguishable from zero. Second, assuming that returns on reinsurance contracts provide a reasonable proxy for expected returns on cat bonds, the study shows that investment in such a portfolio of catastrophe reinsurance contracts from 1970 to 1994 would have generated returns 200 basis points above the Treasury bill rate. Third, adding the portfolio of reinsurance contracts improves the efficiency of a diversified portfolio. Using a base portfolio of 70% domestic assets (70% stocks, 30% bonds) and 30% foreign assets (70% stocks, 30% bonds), the study shows that the reward-to-risk ratio (measured as the realized return minus the risk-free return divided by the standard deviation of the portfolio return) grows from 26% to 30% as the addition of catastrophe risk goes from 5% to 25%. Even though the past is no guarantee for future results, historical data provide strong evidence that catastrophe-linked securities offer portfolio opportunities to investors.

Although cat bonds are the most widely issued and traded capital markets product for catastrophe risk transfer, other securities and derivatives have gained some popularity in the marketplace, including the following:

Sidecars. Investor capital is collateralized against an entity writing a portfolio of reinsurance contracts, and the investor participates in the experience of the entity (that is, the investment return is linked to the premium income earned versus the claims paid on the underlying policies). In some sidecar structures, dealers have issued debt layers against the more remote end of the risk spectrum, which has the effect of adding leverage to the equity position in the vehicle. Most sidecars utilize the underwriting expertise of an established reinsurer.

Extreme mortality securities. Similar to a cat bond in structure, an extreme mortality security protects a sponsor against a catastrophic increase in mortality rates over a short period of time. Insurance companies use these securities to transfer mortality risk associated with pandemics or (to some extent) terrorism, and sponsors tailor the trigger structures to match the geographic, age, and gender characteristics of their underlying books of life insurance policies.

Collateralized debt obligation. In a cat CDO, dealers borrow technology from the asset-backed securities (ABS) market to create both actively and passively managed instruments. In an actively managed instrument, a risk manager assembles and manages a portfolio of cat bonds, other catastrophe instruments, and reinsurance contracts according to predetermined guidelines. In the passively managed structure, the basket of risks is fixed for the duration of the transaction. In both structures, the portfolio backs a capital structure that has both rated and unrated classes of securities.

Synthetics. In the broader credit markets, credit default swaps (CDS) have taken enormous leaps in terms of trading volumes and liquidity, and the technology is being utilized increasingly in the cat space. Protection buyers and sellers can use existing cat bonds to get long or short risk, using standard International Swaps and Derivatives Association (ISDA) documentation. Smaller reinsurance companies that want to offload risk but cannot achieve the economies of scale in launching a cat bond program may find benefits in referencing a different issuer's outstanding cat bond. Investors can also get short using synthetics, enabling them to make bearish trades on what they view as overpriced risk.

Industry loss warranties. Industry loss warranties (ILWs) are another family of derivative contract that are increasingly traded by capital markets players. In an ILW, a protection buyer pays a premium to a counterparty in return for a payout to the extent that a catastrophe's estimated industry-wide losses exceed a certain trigger level in predetermined locations. Terms for an ILW are usually one season (e.g., June through November for the U.S. hurricane season). ILWs are useful risk management tools in that protection buyers may want to hedge certain geographies in the context of their entire risk portfolio, or investors may want to add additional risk in certain regions where they are underexposed. ILWs can be governed by standard ISDA documentation, which increases liquidity due to posting arrangements that exist between financial institutions.

Shelf issuance programs. Similar to ABS issuers, many cat bond issuers have adopted shelf documentation technology for their risk-transfer programs. A shelf is an issuance platform that allows issuers to come to market with new securities quickly to take advantage of market conditions.

Participation in the cat bond market has seen a substantial transformation. The combination of a broader repricing of insurance risk after the devastating 2005 U.S. hurricane season and the emergence of multistrategy hedge funds as a large and active source of capital has brought in a number of new market participants. However, the largest and most consistent cat bond players continue to be dedicated catastrophe funds.

Most investors pursue diversification strategies when participating in the cat bond market. Since principal losses on cat bonds would tend to be binary, investors build diversity into their portfolios by adding securities that cover different peril types (e.g., earthquake versus hurricane) and that cover different geographical territories. Even though two cat bonds may have the same annualized loss probabilities in their respective risk analyses, a cat bond covering a less widely issued peril or geography generally will price at a lower spread than a more frequently issued risk profile.

Several noninsurance companies have issued cat bonds into the capital markets, bypassing the traditional primary insurers for their protection needs. Sponsors range from energy companies looking to protect against hurricane damage on their Gulf region oil production assets to entertainment companies protecting against localized earthquake damage. These cat bonds generally utilize customized trigger structures to protect against very specific geographies.

The focus of this chapter is on catastrophe bonds, a financial security designed to transfer risk associated with natural catastrophic events, like hurricanes and earthquakes. Insurance and reinsurance companies issue catastrophe bonds as an alternative to the traditional reinsurance or retrocession markets to protect themselves from losses incurred during extreme events. Catastrophe bonds can offer attractive yields and give investors the opportunity to invest in an asset uncorrelated to the credit or rate markets. Discussion includes deal structure, the rating agencies' approach to this product, new product development, and how these securities can provide diversification benefits to investment portfolios.

This chapter is an update and expansion of "Catastrophe-Linked Securities" by S. Ganapati, M. Retik, P. Puleo, and B. Starr which appears in Investment Management for Insurers (John Wiley & Sons, 1999).

Canter, M. S., Cole, J. B., and Sandor, R. L. (1996). Insurance derivatives: A new asset class for the capital markets and a new hedging tool for the insurance industry. Journal of Derivatives, Winter: 89-104.

Coval, J. D., Jurek, J. W, and Stafford, E. (2007). Economic catastrophe bonds. Harvard Business School working paper, July.

Froot, K. A. (ed.) (1999). The Financing of Catastrophe Risk. Chicago and London: University of Chicago Press.

Froot, K. A. (2001). The market for catastrophe risk: A clinical examination. Journal of Financial Economics 60: 529-571.

Froot, K., Murphy, B., Stern, A., and Usher, S. (1995). The emerging asset class: Insurance risk. Guy Carpenter & Company Inc.'s Review of Catastrophes Exposures and the Capital Markets, July.

Ganapati, S., Retik, M., Puleo, P., and Starr, B. (1999). Catastrophe-linked securities. In D. F. Babbel and F. J. Fabozzi. (eds.), Investment Management for Insurers (pp. 209-234), New York: John Wiley & Sons.

Koutsaftis, V. (2000). The applications of insurance securitization: A new tool for risk managers; A new asset class for the capital markets and a new source of capital for the insurance industry. University of Chicago School of Business working paper.

Lakdawalla, D., and Zanjani, G. (2006). Catastrophe bonds, reinsurance, and the optimal collateralization of risk transfer. Federal Reserve of New York and Rand Corporation working paper.

Nell, M., and Richter, A. (2004). Improving risk allocation through indexed cat bonds. Geneva Papers on Risk and Insurance 29, 2: 183-201.

Woo, G. (2004). A catastrophe bond niche: Multiple event risk. Paper presented at the 2004 meeting of the NBER Insurance Project Group.