MARK C. FAULKNER

Managing Director, Spitalfields Advisors

Abstract: Securities lending—the temporary transfer of securities on a collateralized basis—is a major and growing activity providing significant benefits for issuers, investors, and traders alike. These are likely to include improved market liquidity, more efficient settlement, tighter dealer prices and, perhaps, a reduction in the cost of capital.

Keywords: securities lending, triparty agent, buy/sellbacks, custodian banks, prime brokers, beneficial owners, repos

This chapter describes securities lending, the motivation for lenders and borrowers to participate, the role of intermediaries, market mechanics, and the risks faced by the lenders of securities.

Securities lending is an important and significant business that describes the market practice whereby securities are temporarily transferred by one party (the lender) to another (the borrower). The borrower is obliged to return the securities to the lender, either on demand, or at the end of any agreed term. For the period of the loan the lender is secured by acceptable assets delivered by the borrower to the lender as collateral.

Securities lending today plays a major part in the efficient functioning of the securities markets worldwide. Yet it remains poorly understood by many of those outside the market.

In some ways, the term "securities lending" is misleading and factually incorrect. Under English law and in many other jurisdictions, the transaction commonly referred to as "securities lending" is, in fact...

a disposal (or sale) of securities linked to the subsequent reacquisition of equivalent securities by means of an agreement.

Such transactions are collateralized and the "rental fee" charged, along with all other aspects of the transaction, is dealt with under the terms agreed between the parties. It is entirely possible and very commonplace that securities are borrowed and then sold or on-lent.

There are some consequences arising from this clarification:

Absolute title over both the securities on loan and the collateral received passes between the parties.

The economic benefits associated with ownership— e.g., dividends, coupons, etc.—are "manufactured" back to the lender, meaning that the borrower is entitled to these benefits as owner of the securities but is under a contractual obligation to make equivalent payments to the lender.

A lender of equities surrenders its rights of ownership, e.g., voting. Should the lender wish to vote on securities on loan, it has the contractual right to recall equivalent securities from the borrower.

Appropriately documented securities lending transactions avoid taxes associated with the sale of a transaction or transference fees.

Most securities loans in today's markets are made against collateral in order to protect the lender against the possible default of the borrower. This collateral can be cash or other securities or other assets.

Transactions Collateralized with Other Securities or Assets

Noncash collateral would typically be drawn from the following collateral types:

Government bonds

Issued by G7, G10 or non-G7 governments

Corporate bonds

Various credit ratings

Convertible bonds

Matched or unmatched to the securities being lent

Equities

Of specified indices

Letters of credit

From banks of a specified credit quality

Certificates of deposit

Drawn on institutions of a specified credit quality

Delivery by value (DBV)

Concentrated or unconcentrated

Of a certain asset class

Warrants

Matched or unmatched to the securities being lent

Other money market instruments

Note that delivery by value is a mechanism in some settlement systems whereby a member may borrow or lend cash overnight against collateral. The system automatically selects and delivers collateral securities, meeting predetermined criteria to the value of the cash (plus a margin) from the account of the cash borrower to the account of the cash lender and reverses the transaction the following morning.

The eligible collateral will be agreed upon between the parties, as will other key factors including:

Notional limits

The absolute value of any asset to be accepted as collateral

Initial margin

The margin required at the outset of a transaction

Maintenance margin

The minimum margin level to be maintained throughout the transaction

Concentration limits

The maximum percentage of any issue to be acceptable, for example, less than 5% of daily traded volume

The maximum percentage of collateral pool that can be taken against the same issuer, that is, the cumulative effect where collateral in the form of letters of credit, CD, equity, bond and convertible may be issued by the same firm

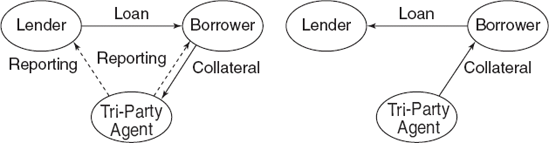

Figure 69.1 shows collateral being held by a triparty agent. This specialist agent (typically a large custodian bank or international central securities depository) receives only eligible collateral from the borrower and hold it in a segregated account to the order of the lender. The triparty agent marks this collateral to market, with information distributed to both lender and borrower (in the diagram, dotted "Reporting" lines). Typically, the borrower pays a fee to the triparty agent.

Table 69.1 provides an illustration of cash flows on a securities against collateral other than cash for a transaction in the United Kingdom.

There is debate within the industry as to whether lenders, which are flexible in the range of noncash collateral that they are willing to receive, are rewarded with correspondingly higher fees. Some argue that they are; others claim that the fees remain largely static, but that borrowers are more prepared to deal with a flexible lender and, therefore, balances and overall revenue rise.

The agreement on a fee is reached between the parties and would typically take into account the following factors:

Demand and supply

The less of a security available, other things being equal, the higher the fee a lender can obtain

Collateral flexibility

The cost to a borrower of giving different types of collateral varies significantly, so that they might be more willing to pay a higher fee if the lender is more flexible

The size of the manufactured dividend required to compensate the lender for the posttax dividend payment that it would have received had it not lent the security

Different lenders have varying tax liabilities on income from securities; the lower the manufactured dividend required by the lender, the higher the fee it can negotiate. (An explanation of how securities lending can be motivated by the different tax status of borrowers and lenders is discussed later in this chapter.)

The term of a transaction

Securities lending transactions can be open to recalls or fixed for a specified term; there is much debate about whether there should be a premium paid or a discount for certainty. If a lender can guarantee a recall-free loan then a premium will be forthcoming. One of the attractions of repo and swaps is the trans-actional certainty on offer from a counterpart

Certainty

As explained later in this chapter, there are trading and arbitrage opportunities, the profitability of which revolves around the making of specific decisions. If a lender can guarantee a certain course of action, this may mean it can negotiate a higher fee

Table 69.1. Table 69.1 Cash Flows on a Securities Loan Against Collateral Other than Cash. The return to a lender of securities against collateral other than cash derives from the fee charged to the borrower. A cash flow of this transaction reads as follows:

Transaction date

June 13, 2007

Settlement date

June 16, 2007

Term

Open

Security

XYZ Limited

Security price

£10.00 per share

Quantity

100,000 shares

Loan value

£1,000,000.00

Lending fee

50 basis points (100ths of 1%)

Collateral

UK FTSE 100 Concentrated DBVs

Margin required

5%

Collateral required

£1,050,000.00 in DBVs

Daily lending income

£1,000,000.00 × 0.005 × (1/365) = €13.70

Should the above transaction remain outstanding for one month and be returned on July 16, 2005 therewill be twoflowsof revenue from the borrower to the lender

On June 30 fees of €191.80 (€13.70 × 14 days)

On July 31 fees of €219.20 (€13.70 × 16 days)

Thus, total revenue is €411.00 against which the cost of settling the transaction (loan and collateral) must be offset.

Note: For purposes of clarity, the example assumes that the value of the security on loan has remained constant, when in reality the price would change daily resulting in a mark to market event, different fees chargeable per day and changes in the value of the collateral required. Open loan transactions can also be rerated or have their fee changed if market circumstances alter. It is assumed that this did not happen either.

Transactions Collateralized with Cash

Cash collateral is, and has been for many years, an integral part of the securities lending business, particularly in the United States. The lines between two distinct activities, securities lending and cash reinvestment, have become blurred and to many U.S. investment institutions securities lending is virtually synonymous with cash reinvestment. This is much less the case outside the United States, but consolidation of the custody business and the important role of U.S. custodian banks in the market means that this practice is becoming more prevalent. The importance of this point lies in the very different risk profiles of these increasingly intertwined activities.

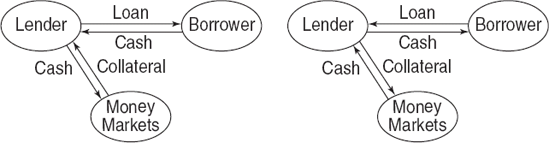

The revenue generated from cash-collateralized securities lending transactions is derived in a different manner from that in a noncash transaction (see Figure 69.2). It is made from the difference or "spread" between interest rates that are paid and received by the lender (see Table 69.2).

Reinvestment guidelines are typically communicated in words by the beneficial owner to their lending agent, and some typical guidelines might be as follows:

Conservative

Overnight G7 government bond repo fund

Maximum effective duration of 1 day

Floating-rate notes and derivatives are not permissible

Restricted to overnight repo agreements Quite

Conservative

AAA-rated government bond repo fund

Maximum average maturity of 90 days

Maximum remaining maturity of any instrument is 13 months

Quite Flexible

Maximum effective duration of 120 days

Maximum remaining effective maturity of 2 years

Floating-rate notes and eligible derivatives are permissible

Credit quality: Short-term ratings: Al/Pl, long-term ratings: A-/A3 or better

Flexible

Maximum effective duration of 120 days

Maximum remaining effective maturity of 5 years

Floating-rate notes and eligible derivatives are permissible

Credit quality: Short-term ratings: Al/Pl, long-term ratings: A-/A3 or better

Some securities lending agents offer customized reinvestment guidelines while others offer reinvestment pools.

Securities lending is part of a larger set of interlinked securities financing markets. These transactions are often used as alternative ways of achieving similar economic outcomes, although the legal form and accounting and tax treatments can differ. The other transactions are described in the following subsections.

Sale and Repurchase Agreements

Sale and repurchase agreements or repos involve one party agreeing to sell securities to another against a transfer of cash, with a simultaneous agreement to repurchase the same securities (or equivalent securities) at a specific price on an agreed date in the future. It is common for the terms "seller" and "buyer" to replace the securities lending terms "lender" and "borrower." Most repos are governed by a master agreement called the TBMA/ISMA Global Master Repurchase Agreement (GMRA) created by the Securities Industry and Financial Markets Association (SIFMA), a U.S. trade association.

Table 69.2. Cash Flows on a Securities Loan Collateralized with Cash

FX Rate assumed of £1.00 = $1.637 If the above transaction remains outstanding for one month and is returned on July 16, 2007, there will be two flows of cash from the lender to the borrower. These are based upon the cash collateral, and the profitability of the lender comes from the 50 basis points spread between the reinvestment rate and the rebate rate $1,718,850 × 0.008 × (1/360)) = $38.20 Payments to the borrower:

The lender's profit will typically be taken as follows:

Thus, total revenue is £437.40 against which the cost of settling the transactions (loan and collateral) must be offset. Note: For purposes of clarity, this example assumes that the value of the security on loan has remained constant for the duration of the above transaction. This is most unlikely; typically the price would change daily resulting in a mark to market and changes to the value of the collateral required. Open loan transactions can also be re-rated or have their rebate changed if market circumstances alter. It is assumed that this did not happen either Themarginal increase in daily profitability associated with the cash transaction at a 50-bps spread compared with the noncash transaction of 50-bps is due to the fact that the cash spread is earned on the collateral which has a 5% margin as well as the fact that the USD interest rate convention is 360 days and not 365 days as in the United Kingdom. | |||||

|---|---|---|---|---|---|

Transaction date | June 13, 2007 | ||||

Settlement date | June 16, 2007 | ||||

Term | Open | ||||

Security | XYZ Limited | ||||

Security price | £10.00 per share | ||||

Quantity | 100,000 shares | ||||

Loan value | £1,000,000.00 | ||||

Rebate rate | 80 basis point | ||||

Collateral | USD cash | ||||

Margin required | 5% | ||||

Collateral required | £1,718,850.00 (€1,050,000.00 × 1.67) | ||||

Reinvestment rate | 130 basis points | ||||

Daily Lending Income | £23.87 or €14.58 (€1,718,850.00 × 0.005 × (1/360)) | ||||

Repos occur for two principal reasons: either to transfer ownership of a particular security between the parties or to facilitate collateralized cash loans or funding transactions.

The bulk of bond lending and bond financing is conducted by repurchase agreements (repos) and there is a growing equity repo market. An annex can be added to the GMRA to facilitate the conduct of equity repo transactions.

Repos are much like securities loans collateralized against cash, in that income is factored into an interest rate that is implicit in the pricing of the two legs of the transaction.

At the beginning of a transaction, securities are valued and sold at the prevailing "dirty" market price (that is, including any coupon that has accrued). At termination, the securities are resold at a predetermined price equal to the original sale price together with interest at a previously agreed rate known as the repo rate.

In securities-driven transactions (that is, where the motivation is not simply financing) the repo rate is typically set at a lower rate than prevailing money market rates to reward the "lender" who invests the funds in the money markets and, thereby, seek a return. The "lender" often receives a margin by pricing the securities above their market level.

In cash-driven transactions, the repurchase price typically is agreed at a level close to current money market yields, as this is a financing rather than a security-specific transaction. The right to substitute repoed securities as collateral is agreed by the parties at the outset. A margin is often provided to the cash "lender" by reducing the value of the transferred securities by an agreed "haircut" or discount.

Buy/Sellbacks

Buy/sellbacks are similar in economic terms to repos but are structured as a sale and simultaneous purchase of securities, with the purchase agreed for a future settlement date. The price of the forward purchase is typically calculated and agreed by reference to market repo rates.

The purchaser of the securities receives absolute title to them and retains any accrued interest and coupon payments during the life of the transaction. However, the price of the forward contract takes account of any coupons received by the purchaser.

Buy/sellback transactions are normally conducted for financing purposes and involve fixed income securities. In general a cash borrower does not have the right to substitute collateral. Until 1996, the bulk of buy/sellback transactions took place outside of a formal legal framework with contract notes being the only form of record. In 1995, the GMRA was amended to incorporate an annex that dealt explicitly with buy/sellbacks. Most buy/sellbacks are now governed by this agreement.

Table 69.3 compares the three main forms of collateralized securities loan transaction.

The securities lending market involves various types of specialist intermediary which take principal and/or agency roles. These intermediaries separate the underlying owners of securities—typically large pension or other funds, and insurance companies—from the eventual borrowers of securities, whose usual motivations are described later in this chapter.

Table 69.3. Summary of Collateralized Loan Transactions

Securities Lending | Repo | ||||

|---|---|---|---|---|---|

Characteristic | Cash Collateral | Securities/Other Noncash Collateral | Specific Securities(securities driven) | General Collateral (cash driven) | Buy/sellback |

Formal method of exchange | Sale with agreement to make subsequent reacquisition of equivalent securities | Sale with agreement to make subsequent reacquisition of equivalent securities | Sale and repurchase under terms of master agreement | Sale and repurchase under terms of master agreement | Sale and repurchase |

Form of exchange | Securities vs. cash | Securities vs. collateral (Note: Often free of payment but sometimes delivery versus delivery) | Securities vs. cash (Note: Often delivery versus payment) | Cash vs. securities (Note: Often delivery versus payment) | Cash vs. securities (Note: Often delivery versus payment) |

Collateral type | Cash | Securities (bonds and equities), letters of Credit, DBVs, CDs | Cash | General collateral(bonds) or acceptable collateral as defined by buyer | Typically bonds |

Return is paid to the supplier of | Cash collateral | Loan securities (not collateral securities) | Cash | Cash | Cash |

Return payable as | Rebate interest (that is, return paid on cash lower than comparable cash market interest rates) | Fee, e.g., standard fees for FTSE 100 stocks are about 6-8 basis points (that is,0.06-0.08% p.a.) | Quoted as repo rate, paid as interest on the cash collateral (lower than general collateral repo rate) | Quoted as repo rate, paid as interest on the cash | Quoted as repo rate, paid through the price differential between sale price and repurchase price |

Initial margin | Yes | Yes | Yes | Yes | Possible |

Variation margin | Yes | Yes | Yes | Yes | No (possible only) through close out and repricing) |

Overcollateralization | Yes (in favor of the securities lender) | Yes (in favor of the securities lender) | No | Possible (if any, in favor of the cash provider) | Possible (if any, in favor of the cash provider) |

Collateral substitution | Yes (determined by borrower) | Yes (determined by borrower) | No | Yes (determined by the original seller) | No (possible only through close out and repricing) |

Dividends and coupons | Manufactured to the lender | Manufactured to the lender | Paid to the original seller | Paid to the original seller | No formal obligation to return income normally factored into the buyback price |

Legal set off in event of default | Yes | Yes | Yes | Yes | No |

Maturity | Open or term | Open or term | Open or term | Open or term | Term only |

Typical asset type | Bonds and equities | Bonds and equities | Mainly bonds, equities possible | Mainly bonds, equities possible | Almost entirely bonds |

Motivation | Security specific dominant | Security specific | Security specific | Financing | Financing dominant |

Payment | Monthly in arrears | Monthly in arrears | At maturity | At maturity | At maturity |

Securities lending is increasingly becoming a volume business and the economies of scale offered by agents that pool together the securities of different clients enable smaller owners of assets to participate in the market. The costs associated with running an efficient securities lending operation are beyond many smaller funds for which this is a peripheral activity. Asset managers and custodian banks have added securities lending to the other services they offer to owners of securities portfolios, while third-party lenders specialize in providing securities lending services.

Owners and agents "split" revenues from securities lending at commercial rates. The split will be determined by many factors including the service level and provision by the agent of any risk mitigation, such as an indemnity.

Securities lending is often part of a much bigger relationship and therefore the split negotiation can become part of a bundled approach to the pricing of a wide range of services.

Asset Managers

It can be argued that securities lending is an asset-management activity—a point that is easily understood in considering the reinvestment of cash collateral. Particularly in Europe, where custodian banks were, perhaps, slower to take up the opportunity to lend than in the United States, many asset managers run significant securities lending operations.

What was once a back-office low profile activity is now a front office growth area for many asset managers. The relationship that the asset managers have with their underlying clients puts them in a strong position to participate.

Custodian Banks

The history of securities lending is inextricably linked with the custodian banks. Once they recognized the potential to act as agent intermediaries and began marketing the service to their customers, they were able to mobilize large pools of securities that were available for lending. This in turn spurred the growth of the market.

Most large custodians have added securities lending to their core custody businesses. Their advantages include: the existing banking relationship with their customers; their investment in technology and global coverage of markets, arising from their custody businesses; the ability to pool assets from many smaller underlying funds, insulating borrowers from the administrative inconvenience of dealing with many small funds and providing borrowers with protection from recalls; and experience in developing as well as developed markets.

Being banks, they also have the capability to provide indemnities and manage cash collateral efficiently—two critical factors for many underlying clients.

Custody is so competitive a business that for many providers it is a loss-making activity. However, it enables the custodians to provide a range of additional services to their client base. These may include foreign exchange, trade execution, securities lending, and fund accounting.

Third-Party Agents

Advances in technology and operational efficiency have made it possible to separate the administration of securities lending from the provision of basic custody services, and a number of specialist third-party agency lenders have established themselves as an alternative to the custodian banks. Their market share is currently growing from a relatively small base. Their focus on securities lending and their ability to deploy new technology without reference to legacy systems can give them flexibility.

There are three broad categories of principal intermediary: broker dealers, specialist intermediaries, and prime brokers. In contrast to the agent intermediaries, principal intermediaries can assume principal risk, offer credit intermediation, and take positions in the securities that they borrow. Distinctions between the three categories are blurred. Many firms would be in all three.

In recent years securities lending markets have been liberalized to a significant extent so that there is little general restriction on who can borrow and who can lend securities. Lending can, in principle, take place directly between beneficial owners and the eventual borrowers. But typically a number of layers of intermediary are involved. What value do the intermediaries add?

A beneficial owner may well be an insurance company or a pension scheme while the ultimate borrower could be a hedge fund. Institutions are often reluctant to take on credit exposures to borrowers that are not well recognized, regulated, or who do not have a good credit rating, which would exclude most hedge funds. In these circumstances, the principal intermediary (often acting as prime broker) performs a credit intermediation service in taking a principal position between the lending institution and the hedge fund.

A further role of the intermediaries is to take on liquidity risk. Typically they will borrow from institutions on an open basis—giving them the option to recall the underlying securities if they want to sell them or for other reasons—while lending to clients on a term basis, giving them certainty that they will be able to cover their short positions.

In many cases, as well as serving the needs of their own propriety traders, principal intermediaries provide a service to the market in matching the supply of beneficial owners that have large stable portfolios with those that have a high borrowing requirement. They also distribute securities to a wider range of borrowers than underlying lenders, which may not have the resources to deal with a large number of counterparts.

These activities leave principal intermediaries exposed to liquidity risk if lenders recall securities that have been on lent to borrowers on a term basis. One way to mitigate this risk is to use in-house inventory where available. For example, proprietary trading positions can be a stable source of lending supply if the long position is associated with a long-term derivatives transaction. Efficient inventory management is seen as critical and many securities lending desks act as central clearers of inventory within their organizations, only borrowing externally when netting of in-house positions is complete. This can require a significant technological investment. Other ways of mitigating "recall risk" include arrangements to borrow securities from affiliated investment management firms, where regulations permit, and bidding for exclusive (and certain) access to securities from other lenders.

On the demand side, intermediaries have historically been dependent upon hedge funds or proprietary traders that make trading decisions. But a growing number of securities lending businesses within investment banks have either developed "trading" capabilities within their lending or financing departments, or entered into joint ventures with other departments or even in some cases their hedge fund customers. The rationale behind this trend is that the financing component of certain trading strategies is so significant that without the loan there is no trade.

Table 69.4. Services Provided by Prime Brokers

Profitable Activities | Part of the Cost of Being in Business |

|---|---|

Securities lending | Clearance |

Leverage of financing provision | Custody |

Trade execution | Reporting |

Broker-Dealers

Broker-dealers borrow securities for a wide range of reasons:

Market making

To support proprietary trading

On behalf of clients

Many broker-dealers combine their securities lending activities with their prime brokerage operation (the business of servicing the broad requirements of hedge funds and other alternative investment managers). This can bring significant efficiency and cost benefits. Typically, within broker-dealers the fixed income and equity divisions duplicate their lending and financing activities.

Prime Brokers

Prime brokers serve the needs of hedge funds and other "alternative" investment managers. The business was once viewed, simply, as the provision of six distinct services, although many others such as capital introduction, risk management, fund accounting, and startup assistance have now been added (see Table 69.4).

Securities lending is one of the central components of a successful prime brokerage operation, with its scale depending on the strategies of the hedge funds for which the prime broker acts. Two strategies that are heavily reliant on securities borrowing are long/short equity and convertible bond arbitrage.

The cost associated with the establishment of a full-service prime broker is steep, and recognized providers have a significant advantage. Some of the newer entrants have been using total return swaps, contracts for difference, and other derivative transaction types to offer what has become known as "synthetic prime brokerage." Again, securities lending remains a key component of the service as the prime broker will still need to borrow securities in order to hedge the derivatives positions it has entered into with the hedge funds, for example, to cover short positions. But it is internalized within the prime broker and less obvious to the client.

Those beneficial owners with securities portfolios of sufficient size to make securities lending worthwhile include pension funds, insurance and assurance companies, mutual funds/unit trusts, and endowments.

Beneficial Owner Considerations

When considering whether and how to lend securities, beneficial owners first need to consider organization characteristics and portfolio characteristics.

Organization characteristics include management motivation, technology investment, and credit risk appetitive. With regards to management motivation, some owners lend securities solely to offset custody and administrative costs, while others are seeking more significant revenue. Lenders vary in their willingness to invest in technological infrastructure to support securities lending. The securities lending market consists of organizations with a wide range of credit quality and collateral capabilities. A cautious approach to counterpart selection (AAA only) and restrictive collateral guidelines (G7 bonds) will limit lending volumes.

Portfolio characteristic include size, holdings size, investment strategy, investment strategy, tax jurisdiction and position, and inventory attractiveness. With respect to size, other things being equal, borrowers prefer large portfolios. Loan transactions generally exceed $250,000. Lesser holdings are of limited appeal to direct borrowers. Holdings of under $250,000 are probably best deployed through an agency programme, where they can be pooled with other inventories. Active investment strategies increase the likelihood of recalls, making them less attractive than passive portfolios. Borrowers want portfolios where they need liquidity. A global portfolio offers the greatest chance of generating a fit. That said, there are markets that are particularly in demand from time to time and there are certain borrowers that have a geographic or asset class focus.

With respect to tax jurisdiction and position, borrowers are responsible for "making good" any benefits of share ownership (excluding voting rights) as if the securities had not been lent. They must "manufacture" (that is, pay) the economic value of dividends to the lender. An institution's tax position compared to that of other possible lenders is therefore an important consideration. If the cost of manufacturing dividends or coupons to a lender is low then its assets will be in greater demand. Finally, regarding inventory attractiveness, "hot" securities are those in high demand while general collateral or general collateral securities are those that are commonly available. Needless to say, the "hotter" the portfolio, the higher the returns to lending.

Routes to the Market

Having examined the organization and portfolio characteristics of the beneficial owner, we must now consider the various possible routes to market. The possible routes to the securities lending market are briefly discussed below. For a more detailed discussion see Faulkner (2003).

Using an Asset Manager as Agent A beneficial owner may find that the asset manager they have chosen, already operates a securities lending programme. This route poses few barriers to getting started quickly.

Using a Custodian as Agent This is the least demanding option for a beneficial owner, especially a new one. They will already have made a major decision in selecting an appropriate custodian. This route also poses few barriers to getting started quickly.

Appointing a Third-Party Specialist as Agent A beneficial owner, who has decided to outsource, may decide it does not want to use the supplier's asset manager(s) or custodian(s), and instead appoint a third-party specialist. This route may mean getting to know and understand a new provider prior to getting started. The opportunity cost of any delay needs to be factored into the decision.

Auctioning a Portfolio to Borrowers Borrowers demand portfolios for which they bid guaranteed returns in exchange for gaining exclusive access to them. There are several different permutations of this auctioning route:

Do-it-yourself auctions

Assisted auctions

Agent assistance

Consultancy assistance

Specialist "auctioneer" assistance

This is not a new phenomenon but one that has gained a higher profile in recent years and discussed in more detail in other chapters in this book. A key issue for the beneficial owner considering this option is the level of operational support that the auctioned portfolio will require and who will provide it. The key issue here is finding the best auctioneer.

Selecting One Principal Borrower Many borrowers effectively act as wholesale intermediaries and have developed global franchises using their expertise and capital to generate spreads between two principals that remain unknown to one another. These principal intermediaries are sometimes separately incorporated organizations, but more frequently, parts of larger banks, broker-dealers or investment banking groups. Acting as principal allows these intermediaries to deal with organizations that the typical beneficial owner may choose to avoid for credit reasons such as, hedge funds.

Lending Directly to Proprietary Principals Normally, after a period of activity in the lending market using one of the above options, a beneficial owner that is large enough in its own right, may wish to explore the possibility of establishing a business "in house," lending directly to a selection of principal borrowers that are the end users of their securities. The proprietary borrowers include broker-dealers, market makers and hedge funds. Some have global borrowing needs while others are more regionally focused.

Choosing Some Combination of the Above Just as there is no single or correct lending method, so the options outlined above are not mutually exclusive. Deciding not to lend one portfolio does not preclude lending to another; similarly, lending in one country does not necessitate lending in all. Choosing a wholesale intermediary that happens to be a custodian in the United States and Canada does not mean that a lender cannot lend Asian assets through a third-party specialist, and European assets directly to a panel of proprietary borrowers.

One of the central questions commonly asked by issuers and investors alike is "Why does the borrower borrow my securities?" Before considering this point, let us examine why issuers might care.

If securities were not issued, they could not be lent. Behind this simple tautology lies an important point. When initial public offerings are frequent and corporate merger and acquisition activity is high, the securities lending business benefits. In the early 2000s, the fall in the level of such activity depressed the demand to borrow securities leading to a depressed equity securities lending market (that is, fewer trading opportunities, less demand, and fewer "specials") and issuer concern about the role of securities lending, such as whether it is linked in any way to the decline in the value of a company's shares or whether securities lending should be discouraged.

How many times does an issuer discussing a specific corporate event stop to consider the impact that the issuance of a convertible bond, or the adoption of a dividend reinvestment plan might have upon lending of their shares? There is a significant amount of information available on the "long" side of the market and correspondingly little on the short side. Securities lending activity is not synonymous with short selling. But it is often, although not always, used to finance short sales (discussed next) and might be a reasonable and practical proxy for the scale of short-selling activity in the absence of full short sale disclosure. It is, therefore, natural that issuers would want to understand how and why their securities are traded.

Borrowers, when acting as principals, have no obligation to tell lenders or their agents why they are borrowing securities. In fact, they may well not know themselves as they may be on-lending the securities to proprietary traders or hedge funds that do not share their trading strategies openly. Some prime brokers are deliberately vague when borrowing securities as they wish to protect their underlying hedge fund customer's trading strategy and motivation.

This section explains some of the more common reasons behind the borrowing of securities. In general, these can be grouped into: (1) borrowing to cover a short position (settlement coverage, naked shorting, market making, arbitrage trading); (2) borrowing as part of a financing transaction motivated by the desire to lend cash; and (3) borrowing to transfer ownership temporarily to the advantage of both lender and borrower (tax arbitrage, dividend reinvestment plan arbitrage).

Historically, settlement coverage has played a significant part in the development of the securities lending market. Going back a decade or so, most securities lending businesses were located in the back offices of their organizations and were not properly recognized as businesses in their own right. Particularly for less liquid securities—such as corporate bonds and equities with a limit free float—settlement coverage remains a large part of the demand to borrow.

The ability to borrow to avoid settlement failure is vital to ensure efficient settlement and has encouraged many securities depositories into the automated lending business. This means that they remunerate customers for making their securities available to be lent by the depository automatically in order to avert any settlement failures.

Naked Shorting

Naked shorting can be defined as borrowing securities in order to sell them in the expectation that they can be bought back at a lower price in order to return them to the lender. Naked shorting is a directional strategy, speculating that prices will fall, rather than a part of a wider trading strategy, usually involving a corresponding long position in a related security.

Naked shorting is a high-risk strategy. Although some funds specialize in taking short positions in the shares of companies they judge to be overvalued, the number of funds relying on naked shorting is relatively small and probably declining.

Market Making

Market makers play a central role in the provision of two-way price liquidity in many securities markets around the world. They need to be able to borrow securities in order to settle "buy orders" from customers and to make tight, two-way prices.

The ability to make markets in illiquid small capitalization securities is sometimes hampered by a lack of access to borrowing, and some of the specialists in these less liquid securities have put in place special arrangements to enable them to gain access to securities. These include guaranteed exclusive bids with securities lenders.

The character of borrowing is typically short term for an unknown period of time. The need to know that a loan is available tends to mean that the level of communication between market makers and the securities lending business has to be highly automated. A market maker that goes short and then finds that there is no loan available would have to buy that security back to flatten its book.

Arbitrage Trading

Securities are often borrowed to cover a short position in one security that has been taken to hedge a long position in another as part of an "arbitrage" strategy. Some of the more common arbitrage transactions that involve securities lending are described in the following subsections.

Convertible Bond Arbitrage

Convertible bond arbitrage involves buying a convertible bond and simultaneously selling the underlying equity short and borrowing the shares to cover the short position. Leverage can be deployed to increase the return in this type of transaction. Prime brokers are particularly keen on hedge funds that engage in convertible bond arbitrage as they offer scope for several revenue sources:

Securities lending revenues

Provision of leverage

Execution of the convertible bond

Execution of the equity

Pairs Trading or Relative Value "Arbitrage" This in an investment strategy that seeks to identify two companies with similar characteristics whose equity securities are currently trading at a price relationship that is out of line with their historical trading range. The strategy entails buying the apparently undervalued security while selling the apparently overvalued security short, borrowing the latter security to cover the short position. Focusing on securities in the same sector or industry should normally reduce the risks in this strategy.

Index Arbitrage In this context, arbitrage refers to the simultaneous purchase and sale of the same commodity or stock in two different markets in order to profit from price discrepancies between the markets.

In the stock market, an arbitrage opportunity arises when the same security trades at different prices in different markets. In such a situation, investors buy the security in one market at a lower price and sell it in another for more, capitalizing on the difference. However, such an opportunity vanishes quickly as investors rush in to take advantage of the price difference.

The same principle can be applied to index futures. Being a derivative product, index futures derive their value from the securities that constitute the index. At the same time, the value of index futures is linked to the stock index value through the opportunity cost of funds (borrowing/lending cost) required to play the market.

Stock index arbitrage involves buying or selling a basket of stocks and, conversely, selling or buying futures when mispricing appears to be taking place.

Financing

As broker dealers build derivative prime brokerage and customer margin business, they hold an increasing inventory of securities that requires financing.

This type of activity is high volume and takes place between two counterparts that have the following coincidence of wants: One has cash that they would like to invest on a secured basis and pickup yield. The other has inventory that needs to be financed.

In the case of bonds, the typical financing transaction is a repo or buy/sellback. But for equities, securities lending and equity, repo transactions are used.

Triparty agents are often involved in this type of financing transaction as they can reduce operational costs for the cash lender and they have the settlement capabilities the cash borrower needs to substitute securities collateral as their inventory changes.

Temporary Transfers of Ownership

Temporary transfers of ownership are driven by tax arbitrage and dividend plan reinvestment arbitrage opportunities.

Tax Arbitrage Tax driven trading is an example of securities lending as a means of exchange. Markets that have historically provided the largest opportunities for tax arbitrage include those with significant tax credits that are not available to all investors—examples include Italy Germany and France.

The different tax positions of investors around the world have opened up opportunities for borrowers to use securities lending transactions, in effect, to exchange assets temporarily for the mutual benefit of purchaser, borrower, and lender. The lender's reward comes in one of two ways: either a higher fee for lending if they require a lower manufactured dividend, or a higher manufactured dividend than the posttax dividend they would normally receive (quoted as an "all-in rate").

For example, an offshore lender that would normally receive 75% of a German dividend and incur 25% withholding tax (with no possibility to reclaim) could lend the security to a borrower that, in turn, could sell it to a German investor who was able to obtain a tax credit rather than incur withholding tax. If the offshore lender claimed the 95% of the dividend that it would otherwise have received, it would be making a significant pick-up (20% of the dividend yield), while the borrower might make a spread of between 95% and whatever the German investor was bidding. The terms of these trades vary widely and rates are calculated accordingly.

Dividend Reinvestment Plan Arbitrage Many issuers of securities create an arbitrage opportunity when they offer shareholders the choice of taking a dividend or reinvesting in additional securities at a discounted level.

Income or index tracking funds that cannot deviate from recognized securities weightings may have to choose to take the cash option and forgo the opportunity to take the discounted reinvestment opportunity.

One way that they can share in the potential profitability of this opportunity is to lend securities to borrowers that then take the following action:

Borrow as many guaranteed cash shares as possible, as cheaply as possible.

Tender the borrowed securities to receive the new discounted shares.

Sell the new shares to realize the "profit" between the discounted share price and the market price.

Return the shares and manufacture the cash dividend to the lender.

This section outlines the processes in the life of a securities. Specifically, the following are discussed:

Negotiation of loan deals

Confirmations

Term of loan

Term trades

Putting securities "on hold"

Settlements, including how loans are settled and settlement concerns

Termination of loans

Redelivery, failed trades, and legal remedies

Corporate actions and voting

There are other issues that are unique to specific countries. These include any tax arrangements and reporting of transactions to an exchange or other authority/regulator.

Traditionally securities loans have been negotiated between counterparts (whose credit departments have approved one another) on the phone, and followed up with written or electronic confirmations. Normally the borrower initiates the call to the lender with a borrowing requirement. However, proactive lenders may also offer out in-demand securities to their approved counterparts. This would happen particularly where one borrower returns a security and the lender is still lending it to others in the market, they will contact them to see if they wish to borrow additional securities.

Today, there is an increasing amount of bilateral and multilateral automated lending whereby securities are broadcast as available at particular rates by email or other electronic means. Where lending terms are agreeable, automatic matching can take place.

An example of an electronic platform for negotiating equity securities loan transactions is EquiLend, which began operations in 2002 and is backed by a consortium of financial institutions. EquiLend's stated objective is to:

Provide the securities lending industry with the technology to streamline and automate transactions between borrowing and lending institutions and ... introduce a set of common protocols. EquiLend will connect borrowers and lenders through a common, standards-based global equity lending platform enabling them to transact with increased efficiency and speed, and reduced cost and risk.

EquiLend is not alone in this market; for example, SecFinex offers similar services in Europe.

Written or electronic confirmations are issued, whenever possible, on the day of the trade so that any queries by the other party can be raised as quickly as possible. Material changes during the life of the transaction are agreed between the parties as they occur and may also be confirmed if either party wishes it. Examples of material changes are collateral adjustments or collateral substitutions. The parties agree who will take responsibility for issuing loan confirmations.

Confirmations would normally include the following information:

Contract and settlement dates

Details of loaned securities

Identities of lender and borrower (and any underlying principal)

Acceptable collateral and margin percentages

Term and rates

Bank and settlement account details of the lender and borrower

Loans may be either for a specified term or open. Open loans are trades with no fixed maturity date. It is more usual for securities loans to be open or "at call," especially for equities, because lenders typically wish to preserve the flexibility for fund managers to be able to sell at any time. Lenders are able to sell securities despite their being on open loan because they can usually be recalled from the borrower within the settlement period of the market concerned. Nevertheless, open loans can remain on loan for a long period.

The general description "term trade" is used to describe differing arrangements in the securities lending market. The parties have to agree whether the term of a loan is "fixed" for a definite period or whether the duration is merely "indicative" and, therefore, the securities are callable. If fixed, the lender is not obliged to accept the earlier return of the securities; nor does the borrower need to return the securities early if the lender requests it. Accordingly, securities subject to a fixed loan should not be sold while on loan.

Where the term discussed is intended to be "indicative," it usually means that the borrower has a long-term need for the securities but the lender is unable to fix for term and retains the right to recall the securities if necessary.

Putting securities "on hold" (referred to in the market as "icing" securities) is the practice whereby the lender will reserve securities at the request of a borrower on the borrower's expected need to borrow those securities at a future date. This occurs where the borrower must be sure that the securities will be available before committing to a trade that will require them.

While some details can be agreed between the parties, it is normal for any price quoted to be purely indicative and for securities to be held to the following business day. The borrower can "roll over" the arrangement (that is, continue to "ice" the securities) by contacting the holder before 9 A.M.; otherwise, it terminates.

Key aspects of icing are that the lender does not receive a fee for reserving the securities and they are generally open to challenge by another borrower making a firm bid. In this case the first borrower would have 30 minutes to decide whether to take the securities at that time or to release them.

"Pay-to-Hold" Arrangements

A variation of icing is "pay-to-hold," where the lender does receive a fee for putting the securities on hold. As such, they constitute a contractual agreement and are not open to challenge by other borrowers.

Securities lenders need to settle transactions on a shorter timeframe than the customary settlement period for that market. Settlement will normally be through the lender's custodian bank and this is likely to apply regardless of whether the lender is conducting the operation or delegating to an agent. The lender will usually have agreed a schedule of guaranteed settlement times for its securities lending activity with its custodians. Prompt settlement information is crucial to the efficient monitoring and control of a lending program, with reports needed for both loans and collateral.

In most settlement systems securities loans are settled as "free-of-payment" deliveries and the collateral is taken quite separately, possibly in a different payment or settlement system and maybe a different country and time zone. For example, U.K. equities might be lent against collateral provided in a European International Central Securities Depository or U.S. dollar cash collateral paid in New York. This can give rise to what is known in the market as "daylight exposure," a period during which the loan is not covered as the lent securities have been delivered but the collateral securities have not yet been received. To avoid this exposure some lenders insist on precollateralization, thereby transferring the exposure to the borrower.

The CREST system for settling U.K. and Irish securities is an exception to the normal practice as collateral is available within the system. This enables loans to be settled against cash intraday and for the cash to be exchanged, if desired, at the end of the settlement day for a package of DBV securities overnight. The process can be reversed and repeated the next day.

Open loans may be terminated by the borrower returning securities or by the lender recalling them. The borrower will normally return borrowed securities when it has filled its short position. A borrower will sometimes refinance its loan positions by borrowing more cheaply elsewhere and returning securities to the original lender. The borrower may, however, give the original lender the opportunity to reduce the rate being charged on the loan before borrowing elsewhere.

When deciding which markets and what size to lend in, securities lenders consider how certain they can be of having their securities returned in a timely manner when called, and what remedies are available under the legal agreement (discussed later) in the event of a failed return.

Procedures to be followed in the event of a failed redelivery are usually covered in legal agreements or otherwise agreed between the parties at the outset of the relationship. Financial redress may be available to the lender if the borrower fails to redeliver loaned securities or collateral on the intended settlement date. Costs that would typically be covered include:

Direct interest and/or overdraft incurred.

Costs reasonably and properly incurred as a result of the borrower's failure to meet its sale or delivery obligations.

Total costs and expenses reasonably incurred by the lender as a result of a "buy-in" (that is, where the lender is forced to purchase securities in the open market following the borrower's failure to return them)

Costs that would usually be excluded are those arising from the transferee's negligence or willful default and any indirect or consequential losses. An example of that would be when the nonreturn of loaned securities causes an onward trade for a larger amount to fail. The norm is for only that proportion of the total costs which relates to the unreturned securities or collateral to be claimed. It is good practice, where possible, to consider "shaping" or "partialing" larger transactions (that is, breaking them down into a number of smaller amounts for settlement purposes) so as to avoid the possibility of the whole transaction failing if the transferor cannot redeliver the loaned securities or collateral on the intended settlement date.

Corporate Actions and Votes

The basic premise underlying securities lending is to make the lender "whole" for any corporate action event—such as a dividend, rights, or bonus issue—by putting the borrower under a contractual obligation to make equivalent payments to the lender, for instance by "manufacturing" dividends. However a shareholder's right to vote as part owner of a company cannot be manufactured. When securities are lent, legal ownership and the right to vote in shareholder meetings passes to the borrower, who will often sell the securities on. Where lenders have the right to recall securities, they can use this option to restore their holdings and voting rights. The onus is on the borrower to find the securities, by borrowing or purchasing them in the market if necessary. This can damage market liquidity, which is a risk that intermediaries manage.

It is important that beneficial owners are aware that when shares are lent the right to vote is also transferred. For example, in the United Kingdom, the Securities Lending and Repo Committee's (SLRC's) code of guidance states in Section 2.5.4 that lenders should make it clear to clients that voting rights are transferred. A balance needs to be struck between the importance of voting and the benefits derived from lending the securities. Beneficial owners need to ensure that any agents they have made responsible for their voting and stock lending act in a coordinated way.

Borrowing securities in order to build up a holding in a company with the deliberate purpose of influencing a shareholder vote is not necessarily illegal in the United Kingdom. However, institutional lenders have recently become more aware of the possibility, and tend not to see it as a legitimate use of securities borrowing.

A number of market bodies throughout the world have been addressing the relationship between securities lending and voting. Internationally, a working group of the International Corporate Governance Network is currently examining best practices for longterm investors in relation to securities lending and voting. The SLRC is also considering additions to its code in this area.

This section reviews the main financial risks in securities lending and how lenders usually manage them. More detailed discussion of these risks is provided in other later chapters.

Financial risks in securities lending are primarily managed through the use of collateral and netting. As described earlier in this chapter, collateral can be in the form of securities or cash. The market value of the collateral is typically greater than that of the lent portfolio. This margin is intended to protect the lender from loss and reflect the practical costs of collateral liquidation and repurchase of the lent portfolio in the event of default. Any profits made in the repurchase of the lent portfolio are normally returned to the borrower's liquidator. Losses incurred are borne by the lender with recourse to the borrower's liquidator along with other creditors.

Because of its wide acceptability and ease of management, cash can be highly appropriate collateral. However, the lender needs to decide how best to utilize this form of collateral. As described earlier in this chapter, a lender taking cash as collateral pays rebate interest to the securities borrower, so the cash must be reinvested at a higher rate to make any net return on the collateral. This means the lender needs to decide on an appropriate risk-return trade-off. In simple terms, reinvesting in assets that carry one of the following risks can increase expected returns: a higher credit risk: a risk of loss in the event of defaults or a longer maturity in relation to the likely term of the loan. Many of the large securities lending losses over the years have been associated with reinvestment of cash collateral.

Typically, lenders delegate reinvestment to their agents (e.g., custodian banks). They specify reinvestment guidelines, such as those set out earlier in this chapter. There is a move toward more quantitative, risk-based approaches, often specifying the "value at risk" in relation to the different expected returns earned from alternative reinvestment profiles. Agents do not usually offer an indemnity against losses on reinvestment activity so that the lender retains all of the risk while their agent is paid part of the return.

Compared with cash collateral, taking other securities as collateral is a way of avoiding reinvestment risk. In addition to the risks of error, systems failure and fraud always present in any market, problems then arise on the default of a borrower. In such cases the lender will seek to sell the collateral securities in order to raise the funds to replace the lent securities. Transactions collateralized with securities are exposed to a number of different risks that are described below.

Reaction and Legal Risk

If a lender experiences delays in either selling the collateral securities or repurchasing the lent securities, it runs a greater risk that the value of the collateral will fall below that of the loan in the interim. Typically, the longer the delay, the larger the risk.

Mispricing Risk

The lender will be exposed if either collateral securities have been overvalued or lent securities undervalued because the prices used to mark-to-market differ from prices that can actually be traded in the secondary market. One example of mispricing is using mid rather than bid prices for collateral. For illiquid securities, obtaining a reliable price source is particularly difficult because of the lack of trading activity.

Liquidity Risk

Illiquid securities are more likely to be released at a lower price than the valuation used. Valuation "haircuts" are used to mitigate this risk (that is, collateral is valued at, for example, 98% or 95% of the current market value). The haircuts might depend upon:

The proportion of the total security issue held in the portfolio—the larger the position, the greater the haircut

The average daily traded volume of the security: the lower the volume, the greater the haircut

The volatility of the security; the higher the volatility, the greater the haircut

Congruency of Collateral and Lent Portfolios (Mismatch Risk)

If the lent and collateral portfolios were identical, then there would be no market risk. In practice, of course, the lent and collateral portfolios are often very different. The lender's risk is that the market value of the lent securities increases but that of the collateral securities falls before rebalancing can be effected. Provided the counterpart has not defaulted, the lender will be able to call for additional collateral on any adverse collateral/loan price movements. However, following default, it will be exposed until it has been able sell the collateral and replace the lent securities.

The size of mismatch risk depends on the expected co-variance of the value of the collateral and lent securities. The risk will be greater if the value of the collateral is more volatile, the value of the lent securities is more volatile, or if their values do not tend to move together, so that the expected correlation between changes in their value is low.

Many agent intermediaries will offer beneficial owners protection against these risks by agreeing to return (buy-in) lent securities immediately for their clients following a fail, taking on the risk that the value of the collateral on liquidation is lower.

Securities lending is a global activity that the majority of financial organizations engage in to some greater or lesser extent. Some outsource what they see as a noncore activity to others (e.g., pension funds and hedge funds); others specialize in the activity and add value as either agent or principal intermediaries (e.g., custodian banks acting as agents or broker dealers acting as prime brokers.

The importance of this business to individual organizations varies significantly as they take their share of a $10 billion dollar gross revenue pool. The importance to the global markets overall is much more important as this activity facilitates liquidity, enables pricing efficiency, and provides hedging opportunities.

The author is grateful for the assistance provided by David Rule, Simon Hills, Dagmar Banton, John Serocold, Andrew Clayton, Joyce Martindale, Susan Adeane, Habib Motani, Niki Natarajan, Andrew Barrie, Jackie Davis, and Bill Cuthbert.

Blount, E., and Gerdeman, A. J. (2005). Managing liquidity risks in cash-based lending programs. In Fabozzi, F. J., and Mann, S. V. (eds.), Securities Finance: Securities Lending and Repurchase Agreements (pp. 127-140). Hoboken, NJ: John Wiley & Sons.

Dropkin, C. E. (2005). Developing effective guidelines for managing legal risks—U.S. guidelines. In Fabozzi, F. J., and Mann, S. V. (eds.), Securities Finance: Securities Lending and Repurchase Agreements (pp. 167-178). Hoboken, NJ: John Wiley & Sons.

Economou, P. (2005). Risk, return, and performance measurement in securities lending. In Fabozzi, F. J., and Mann, S. V. (eds.), Securities Finance: Securities Lending and Repurchase Agreements (pp. 151-166). Hoboken, NJ: John Wiley & Sons.

Fabozzi, F. J. (ed.) (1997). Securities Lending and Repurchase Agreements, Hoboken, NJ: John Wiley & Sons.

Faulkner, M. C. (2005a). Finding a route to market: An institutional guide to the securities lending labyrinth. In Fabozzi, F. J., and Mann, S. V. (eds.), Securities Finance: Securities Lending and Repurchase Agreements (pp. 57-78). Hoboken, NJ: John Wiley & Sons.

Faulkner, M. C. (2005b). Quantifying risks in securities lending transactions. In Fabozzi, F. J., and Mann, S. V. (eds.), Securities Finance: Securities Lending and Repurchase Agreements (pp. 141-150), Hoboken, NJ: John Wiley & Sons.

Kiefer, D. E., and Mabry, J. G. (2005). The auction process and its role in the securities lending markets. In Fabozzi, F. J., and Mann, S. V. (eds.), Securities Finance: Securities Lending and Repurchase Agreements (pp. 87-106). Hoboken, NJ: John Wiley & Sons.

Nazzaro, A. A. (2005). Evaluating lending options. In Fabozzi, F. J., and Mann, S. V. (eds.), Securities Finance: Securities Lending and Repurchase Agreements (pp. 79-86). Hoboken, NJ: John Wiley & Sons.

Peters, S. C. (2005). Accounting treatment of loans of securities. In Fabozzi, F. J., and Mann, S. V. (eds.), Securities Finance: Securities Lending and Repurchase Agreements (pp. 205-217). Hoboken, NJ: John Wiley & Sons.

Shapiro, R. J. (2005). Tax issues associated with securities lending. In Fabozzi, F. J., and Mann, S. V. (eds.), Securities Finance: Securities Lending and Repurchase Agreements (pp. 179-204). Hoboken, NJ: John Wiley & Sons.