JEROEN KERKHOF PhD

Vice President, Morgan Stanley

Abstract: Numerous financial institutions face inflation risk in their activities. Using inflation derivatives allows them to transfer their inflation risk. The payoff of inflation derivatives depends on the value of inflation indices. Inflation indices are constructed by statistical agencies using the value of representative baskets of goods. By linking the payoff of inflation derivatives to representative baskets of goods inflation derivatives allow investors to focus on real rather than nominal returns. A variety of inflation derivatives exist in market and the most common types are the zero-coupon inflation swap and the year-on-year inflation swap.

Keywords: inflation risk, inflation indices, seasonality, nominal returns, real returns, zero-coupon inflation swap, year-on-year inflation swap, real swaptions

Inflation derivatives allow the transfer of inflation risk. For example, pension funds may want to cover their natural liabilities to inflation risk, while utility companies may want to shed some of their natural exposure to inflation risk. In short, inflation derivatives provide an efficient way to transfer inflation risk. Their flexibility allows users to replicate in derivative form the inflation risks embedded in other instruments such as standard cash instruments (that is, inflation-linked bonds). For example, as is explained later, an inflation swap can be theoretically replicated using a portfolio of a zero-coupon inflation-linked bond and a zero-coupon nominal bond.

As in other markets inflation derivatives have the advantage over the more standard inflation-linked bonds that they can be tailored to fit particular investor needs. Although in essence very similar the variety of inflation derivatives is much greater than that of inflation-linked bonds. For instance, in the cash market most of the inflation-linked bonds have the same maturity date and thereby exposure to the same inflation index fixings. Using inflation swaps one can get exposure to the January, February, ..., or December index fixing. Besides having standard swap structures the inflation derivatives market also allows for exotic coupon structures linked to inflation. For instance, a real estate company might be interested in hedging the inflation adjustment in his rental income. In order to do so the company enters into a swap that replicates the cash flows from its rental contracts.

Contrary to their cash inflation-linked products, inflation derivatives are unfunded. Separating the issue of funding from inflation risk has made the inflation markets more accessible to parties with high funding costs and has made it cheaper to leverage inflation risk. For instance, hedge funds are increasingly involved in inflation markets and often use the derivative format rather than cash.

Since 2002 the inflation derivatives market has grown from a fairly exotic branch of the interest rate market to a well-established market of its own. Low returns on traditional fixed income assets in 2003 led to a demand for structured inflation products in 2003 on the back of which the zero-coupon swap market (due to hedging demand) increased substantially. Although the market has gathered critical mass and the growth has been swift, it still represents only a small fraction of the total interest rates market. In the longer run, one could expect the ratio of outstanding notional in nominal derivatives versus inflation derivatives to move towards the ratio of outstanding nominal bonds versus inflation-linked bonds.

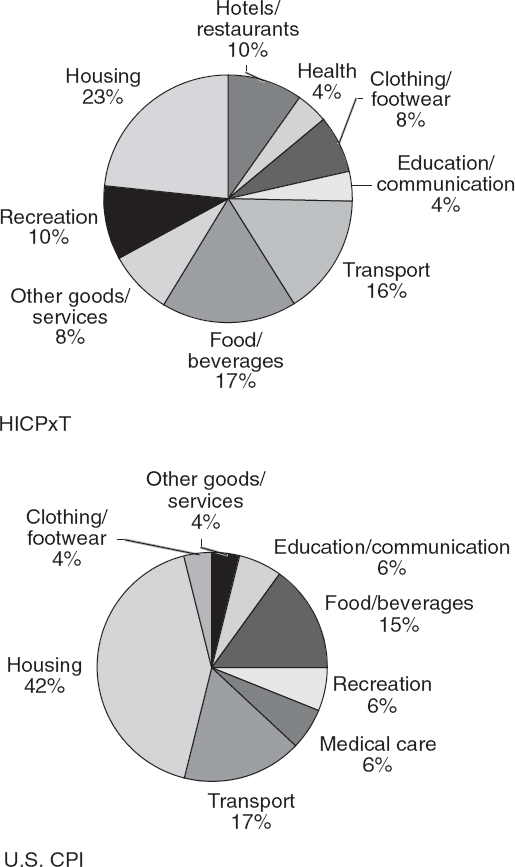

The actively traded indices in the inflation derivatives market are the same as in the cash market. The main markets are the European market which uses the Euro Consumer Price Index (HICPxT) published by Eurostat, the French market using the FRCPI published by the Institut National de la Statistique et des Etudes Economiques (INSEE), and the U.K. market using the Retail Prices Index (RPI) published by National Statistics. As of early 2007, the U.S. market is relatively small, despite having the largest cash market (the U.S. Treasury Inflation Protection Securities, TIPS); as the TIPS market the derivatives market also uses the CPURNSA index published by the Bureau of Labor Statistics (BLS). The compositions of the various indices can vary considerably as can be seen in Figure 68.1.

The payers of inflation in the market are typically entities that receive inflation in the natural line of their business. Prime examples are sovereigns and utility companies that receive inflation via taxes and fees, respectively. For them having inflation-linked debt fits very well in their asset-liability management. On the receiving side, we typically have investors that need to pay inflation in the natural line of business. Pension funds are the prime example. As their liabilities are (either explicitly or implicitly) linked to inflation, inflation-linked securities fit very well in their asset-liability management. Besides for the above mentioned natural players inflation markets are also attractive for inflation neutral investors as they allow for diversification benefits for their portfolios.

A simple, but important and fundamental, economic axiom states that economic agents are concerned about the relative value of money rather than its absolute value. This well-known economic axiom underlies the existence of the inflation-linked market. In order to represent the concept of real value a basket of goods and services is constructed that tries to represent the basket of goods and services used by a representative customer. The nominal value of the basket of goods and services is computed at regular intervals (typically monthly). An inflation index is defined as the relative value of the basket. A base date (period) is chosen at which the nominal value of the index is set equal to (typically) 100. If the nominal value of the basket equals €1,000 at the base date it means that the index will rise 1 point if the value of the basket of goods increases by €10.

Figure 68.1. Constituents of HICP Ex-Tobacco and U.S. CPI Source: Eurostat, Bureau of Labor Statistics.

For example, let us consider an investor with assets equal to €100,000. The investor can currently buy 100 baskets of goods with his assets. The value of his basket of goods is represented by an inflation index. A year later the index has risen from 100 to 104 (the cost of the basket has increased to €1,040). This means that inflation was equal to 4% (= 104/100 − 1). Besides the increase in the index, the nominal value of the assets of the investor has increased to €102,000. The nominal increase in income for the investor equalled:

However, due to the inflation of 4% the investor can now only buy 98.08 (= 102,000/1,040) baskets of goods and services. The real income change for the investor is therefore equal to:

Of course, there is no need to compute the real change via the value of the reference basket. We find the same result using the nominal values and the inflation index:

Even though the value of the investor's assets grew in nominal terms (+2%), in real terms his assets have actually decreased (−1.92%).

As investors care about real income rather than nominal income, they prefer to invest in securities guaranteeing them a real return rather than a nominal one. In this section, how investors can get guaranteed real returns instead of nominal returns by using inflation-linked bonds in a world with inflation is demonstrated.

An inflation-linked zero-coupon bond is a bond that has a single payment at time T, its maturity date. Its value today (denoting today with time 0) is denoted as DIL(0,T). The nominal payment at maturity equals

the value of the inflation index at the maturity date. As investors are interested in real returns, they value all cash flows relative to the index, I. Therefore, the inflation-linked bond has a real value equal to

real unit at maturity. In order to get the real value of this inflation-linked bond today, Dr(0,T), we need to divide the value of the inflation-linked bond by the current value of the inflation index, I(0). The real value of an inflation-linked zero-coupon bond is given by

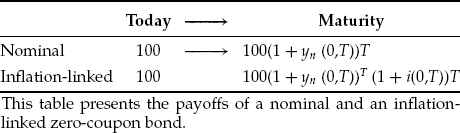

The current nominal value of €1 at time T is denoted by Dn(0,T), a nominal zero-coupon bond. Similarly, the current real value of 1 real unit at time T is denoted by Dr(0,T), a real zero-coupon bond. The cash flows and values of a nominal and an inflation-linked zero-coupon bond in both nominal and real terms are illustrated in Table 68.1.

The real return (that is, return in real units) on an inflation-linked zero-coupon bond is given by

where yr(0,T) denotes the annualized real zero-yield and Dr(0,T) denotes real value of an inflation-linked bond maturing at time T. Thus, using inflation-linked bonds one can get a guaranteed real return in the same way as nominal bonds allow one to get a guaranteed nominal return.

Table 68.1. Inflation-Linked Payments in Nominal and Real Terms

Today (t = 0) | Maturity (T) | |

|---|---|---|

Inflation-linked zero-coupon bond | ||

Nominal units | I(O)Dr(O,T) = DIL(O,T) | I(T) |

Real units | Dr(O,T) | 1 |

Nominal zero-coupon bond | ||

Nominal units | Dn(O,T) | 1 |

Real units | Dn(O,T)/I(O) | 1/I(T) |

The nominal return on an inflation-linked bond is uncertain and given by:

For example, without loss of generality, assume that the current index equals 100, I(0) = 100. The market trades an inflation-linked zero-coupon bond at 97.09% and a nominal bond at 95.24%, both with a time to maturity equal to 1 year (T = 1). From these values we can get the annualised nominal yields and real yields in the following manner.

Nominal yield on nominal zero-coupon bond:

Real yield on inflation-linked zero-coupon bond:

An investor can thus lock-in a guaranteed nominal return of 5% or a guaranteed real return of 3%. Given the growth of the inflation index, we can calculate the real yield on a nominal bond and the nominal yield on an inflation-linked bond. Assuming the inflation index grows to 102, I(T) = 102, these can be computed in the following manner.

Real yield on nominal zero-coupon bond:

Nominal yield on inflation-linked zero-coupon bond:

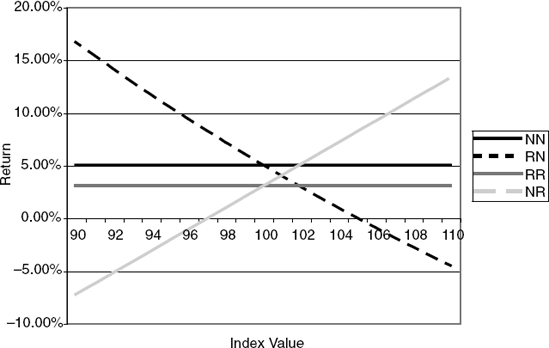

We see in Figure 68.2 that the nominal bond has a certain nominal return but uncertain real return, whereas the inflation-linked bond has a certain real return and an uncertain nominal return. Figure 68.2 also shows that for 1.94% inflation the nominal bond and the inflation-linked bond have the same nominal and real returns. This inflation level is denoted the breakeven inflation and I will discuss this later on in more depth.

As is the case in the nominal market, issuers do not issue zero-coupon bonds, but typically issue inflation-linked coupon bonds. In the same manner as for nominal bonds we can show that an inflation-linked coupon bond is nothing more than a portfolio of inflation-linked zero-coupon bonds with different maturities. Consider an inflation-linked coupon bond that pays a coupon equal to c at times T1,..., TN. We can write the nominal value of this bond at time 0 ≤ T1 as follows

Figure 68.2. Nominal versus Real Returns of Nominal and Inflation-Linked Bonds NN = nominal return on the nominal bond, RN = real return on the nominal bond, NR = nominal return on the real bond, and RR = real return on the real bond.

A detailed account of inflation-linked bonds is given in Deacon et al. (2004).

As discussed before, the main purpose of inflation-linked securities is to provide real value certainty. In the previous section, an ideal world was described. In practice, there are certain constraints due to which it is not possible to exactly guarantee a real return using inflation-linked bonds. First, it should be noted that only a limited number of inflation indices exist in the market. Because consumers are a heterogeneous group, one cannot hope to find a basket of goods which represents the different preferences of all consumers. At best, one can find a basket that represents the average consumer's preferences accurately. In measuring a real return an inflation index can therefore only be seen as an approximation.

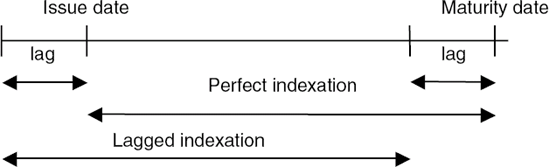

Lags

In order to achieve a high degree of real value certainty the inflation-linked cash flows should be linked as closely as possible to contemporaneous inflation. However, in practice, the value of the index is not yet known for the cash flow date and a lagged index value is taken. As a result, investors have no inflation protection over the last period (typically, three months) of their inflation-protected security. They are compensated for this by receiving the inflation of the period preceding the purchase of the security. This is illustrated in Figure 68.3. In general, the inflation over the perfect indexation period is not equal to the inflation over the lagged inflation period leading to a lower degree of real value certainty.

Differences are likely to be bigger for longer indexation lags and more volatile inflation environments. Furthermore, the influence of the lag increases with decreasing time to maturity. Therefore, a small indexation lag is preferred for a high degree of real value certainty.

This figure graphically illustrates the influence of lagged inflation on real value certainty.

The indexation lags stems from two reasons. First, it takes time to process consumer price data and compute inflation numbers. Due to the processing time, typically inflation is announced about two weeks after the month under consideration (for example, January inflation is announced on about February 15). Second, a lag is needed due to trading and settling of bonds between coupon payment dates. As for nominal bonds, inflation-linked bonds usually pay coupons; if the bond trades between coupon dates sellers should be compensated for having held the bond for part of the coupon period even though they will not receive the coupon. As for nominal bonds, this compensation is effected via the payment of accrued interest. Two main methods of accrued interest payment are seen in practice. The oldest is the one employed by inflation-linked gilts in the U.K. market issued before 2005, where the next coupon is known at all times. This is achieved by using an eight-month lag consisting of a two-month period allowing for publication of the inflation index and six months for the accrued interest calculation (the inflation-linked gilts pay semiannual coupons).

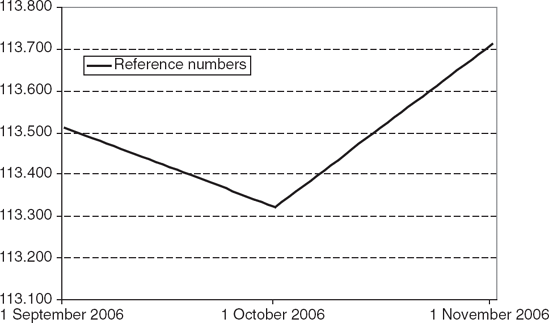

A more common and preferred method these days is to base the accrued interest on the cumulative movements in the associated inflation index. This calculation method was initiated by Canada for their inflation-linked bonds and has been adopted in continental Europe, the United States, and in the United Kingdom for bonds issued from 2005 onwards. The method computes (daily) reference numbers for dates using a linear interpolation of the index values of, typically, two and three months ago. The reference number for the first of any calendar month equals the index value of the calendar month three months earlier. I(01-Apr-07) = CPJ(Jan-07), J(01-May-07) = CPI(Feb-07), and so on. The reference numbers for other dates can then be computed using linear interpolation of the reference numbers of the first days of the calendar months. For example, in Figure 68.4 we compute the reference number, I(19-Sep-06) at 19 September 2006 for the French Consumer Price Index (CPI). In general, the daily reference number can be computed as follows:

I(dd/mm/yy)

where TOM denotes the number of the total days in the month for all days between the first of January and the first of December. For the days in December we have:

I(dd/mm/yy)

Using the (daily) reference numbers, inflation-linked bonds can be quoted in the standard manner, that is, as real bonds. However, in order to get the value of the inflation-linked bond, this price in real terms should be multiplied by the index ratio which is the current daily reference number computed in the manner suggested by the Canadian Treasury divided by the daily reference number at the start of the bond.

To explain the concept of breakeven inflation, we consider two products available in the market today. The first is a nominal zero-coupon bond with maturity date T, whose nominal value today is indicated by DIL(0,T) and pays off 1 at maturity. The second is a zero-coupon inflation-linked bond with maturity date T, whose nominal value today we indicate by DIL(0,T) = I(0)Dr(0,T), where I(0) denotes the current reference number and Dr(0,T) denotes the real value of a real bond with maturity date T. The final payoff of this inflation-linked bond at maturity will equal I(T), the reference number at maturity.

We assume an investor has €100 to invest and needs to choose between the following two investments. Investment 1 is in nominal zero-coupon bonds, while investment 2 is in inflation-linked zero-coupon bonds.

Invest €100 in zero-coupon nominal bonds, that is, 100/Dn(0,T) units. The nominal payoff of this investment at maturity is given by

where yn(0,T) is the annualised nominal yield on the nominal zero-coupon bond. Assuming Dn(0,T) = 0.9524 with T = 1, we have a final payoff of

Invest €100 in zero-coupon inflation-linked bonds, that is, 100/(I(0)Dr(0,T)) units. The nominal payoff of this investment at maturity is given by:

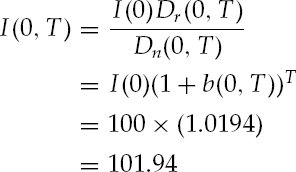

where i(0,T) denotes the annual realised inflation and yr(0,T) is the annualized real yield on the real bond. Assuming I(0) = 100 and Dr(0,T) = 0.9709 for T = 1 we have as a final payoff:

which will depend on the inflation realized in the next year. The returns are illustrated in Table 68.2. The payoff from the nominal investment can be contracted today, while the payoff from the inflation-linked bond depends on realized inflation.

For the nominal investment, the nominal payoff at maturity is known today as Dn(0,T), and thereby yn(0,T) are known today. For the inflation-linked investment, the nominal payoff at maturity depends on the realized inflation from today to maturity, i(0,T). If realized inflation, i(0,T), turns out to equal:

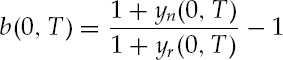

the investor would, ex post, be indifferent between investment 1 and 2. We define this quantity as the breakeven inflation rate, b(0,T):

It is easy to check that if inflation equalled 1.94% investors would have been indifferent between investing in the inflation-linked and the nominal bond. In the case of the nominal bond, they would have invested €100 in 100/0.9524 = 105.00 nominal bonds, which returned €105.00 at maturity. In the case of the inflation-linked bond, they would have invested €100 in 100/0.9709 = 103.00 inflation-linked bonds resulting in 103.00 × 101.94 = €105.00 at maturity. The payoffs in both nominal and real terms thus coincide for both the nominal and inflation-linked bond if realised inflation equals the breakeven inflation. If the realised inflation turns out to be higher (lower) than b(0,T), investors would have been better off investing in the inflation-linked (nominal) bond.

The breakeven rate gives us the indifference point of the realized inflation rate between the inflation-linked and the nominal investment. Another quantity of interest is the reference level for which the investor would be indifferent. This reference level is called the breakeven reference number and is denoted by I(0,T). If the reference level at maturity, I(T), equals:

the investor would, ex post, be indifferent between investment 1 and 2. If the reference index at maturity turns out to be higher (lower) than I(0,T), investors would have been better off investing in the inflation-linked (nominal) bond.

With the introduction of the breakeven reference level, we can write the current nominal value of an inflation-linked payment at time T as Dn(0,T) × I(0,T), the discounted nominal value of the breakeven reference number. This follows from the fact that, by definition, we have:

Components of Breakeven Inflation Rate

It is tempting to think that the breakeven rate should equal expected inflation. However, although expected inflation typically comprises the largest component of the breakeven swap rate, there are several reasons why they will not usually be the same. First, there is the compounding effect, which is a mathematical point. If the annualized inflation for the period from 0 to T, that is i(0,T), is random, the expected payoff of an inflation-linked security would be higher than if it were to grow at the expected annualized inflation rate as a consequence of Jensen's inequality. In formulas, the compounding effect can be presented as

where E denotes expectation. The equality applies only if i(0,T) is deterministic. Thus, the compounding effect has upward pressure on breakeven inflation rates.

Second, the inflation convexity, meaning the second-order price effect in case of inflation changes, increases with the maturity of the bond. High convexity is attractive for investors: it means that prices rise more than inflation duration predicts if breakeven inflation rates increase, and decrease less than inflation duration predicts if breakeven inflation rates decrease. As convexity is attractive for investors, it pushes down the breakeven rates.

Finally, as inflation-linked bonds provide a high degree of real value certainty, investors are willing to pay an inflation risk premium to receive inflation. The inflation risk premium pushes breakeven inflation higher than expected inflation. More specifically, consider risk-averse investors who are interested in real income which is perfectly matched by the daily reference numbers, I. At time t these investors can invest in either an inflation-linked bond with maturity T offering them a real return of yr(0,T) or a nominal bond with maturity T offering them a nominal return of yn(0,T). This gives the following real returns of the nominal and the inflation-linked bond, respectively.

Because the real return on the nominal bond is uncertain and the real return on the inflation-linked bond is certain, risk-averse investors will only consider investing in the nominal bond if they are compensated for bearing the inflation risk (or get diversification benefits). This will be the case if the expected real return on the nominal bond is higher than the real return on the inflation-linked bond, or if the nominal return on the nominal bond is higher than the expected nominal return on the inflation-linked bond, that is,

The additional return that sovereigns (or other issuers) need to pay on nominal issues compared with inflation-linked issues is called the inflation risk premium, which we denote by p(0,T). We can now write the nominal rate as a Fisher equation:

Thus, the nominal return equals the real return times the expected index increase times the risk premium. The size of the inflation risk premium depends on the volatility of inflation (higher volatility leads to higher premium) and the risk-averseness of investors (the more risk-averse the higher the premium).

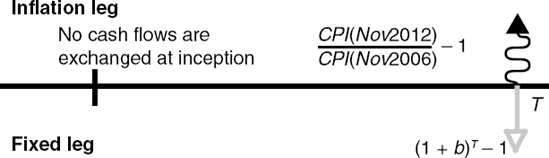

The basic building block of the inflation derivatives market is the zero-coupon inflation swap. Its appeal is its simplicity and the fact that it offers investors and hedgers a wide range of possibilities that did not previously exist in the cash market.

A fixed zero-coupon inflation swap is a bilateral contract that enables an investor or hedger to secure an inflation-protected return with respect to an inflation index. The inflation buyer (also called the inflation receiver) pays a predetermined fixed rate, and in return receives from the inflation seller (also called the inflation payer) an inflation-linked payment.

The mechanics are fairly simple; today an inflation payer and an inflation receiver agree to exchange the change in the inflation index value from a base month (say, November 2006) to an end month (say, November 2012) versus a compounded fixed rate (see Figure 68.5).

If the value of the index in the base month is known at the time of the inception of the contract, we call the inflation swap spot starting. If the value of the index in the base month is not yet known, we speak of a forward starting inflation swap (it is shown later that forward starting inflation swaps are the building blocks of period-on-period inflation swaps).

The inflation market trades inflation swaps using two different conventions. The first convention, the CPI convention, uses the value of the CPI in the payoff while the second convention, the interpolated convention, uses the daily reference numbers to compute the payoff. Table 68.3 gives an overview of the conventions used in the main inflation markets. Table 68.4 provides an example term sheet of a spot starting inflation swap for the European HICPxT market.

Table 68.3. Market Conventions for Zero-Coupon Swaps

Market | Method |

|---|---|

European (HICPxT, HICP – all items) | Monthly index level (3-month lag) |

French (FR CPI) | Interpolated values |

United Kingdom (UK RPI) | Monthly index level (2-month lag) |

United States (CPI-NSA) | Interpolated values |

Table 68.5. Example of a Term Sheet for French CPI Zero-Coupon Inflation Swap

Notional: | ɛ100,000,000 |

Index: | FRCPI (nonrevised) |

Source: First publication by INSEE as shown on Reuters OATINFLATION01 | |

Trade date: | 21-Sep-2006 |

Start date: | 25-Sep-2006 (Trade date + 2 business days) |

End date: | 25-Sep-2011 (Start date + tenor (5 years)) |

First fixing: | 113.358 (reference number for 25-Sep-2006) |

Fixed leg: | (1 + 2.00%)5 − 1 |

Inflation leg: | |

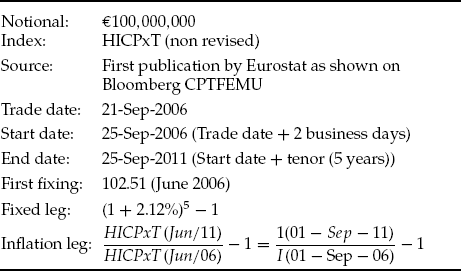

The inflation swap starts on 25 September 2006 and ends on 25 September 2011 with the exchange of cash flows. The only unknown quantity in the payoff is the value of the HICPxT index for June 2011.

As the value of the HICPxT index in the contract month of 2011 needs to be known at the payment, the contract month is lagged to the current month (usually by two to three months). In the above example, the contract month is June and the HICPxT index values for June are normally published mid-July, which is well before the payment/end date. As the value of the HICPxT index in June 2006 (it equalled 102.51) is known by September 21, 2006, the inflation swap in our example is spot starting. It is market standard to quote fixed inflation swaps whose initial lifetime equals a multiple of whole years (5 years in our example). Note that as the contract month is June, the inflation leg payoff in terms of reference numbers is based on September 1, not September 25. This has the advantage that all contracts trading with the same contract month and maturity have the same final payoff. This simplifies closing out of the position.

Not all markets use the convention to pay in terms of index levels. The market standard for the French FR-CPI and US-CPI is to define the payout on the inflation leg in terms of reference numbers. A term sheet would look like the one shown in Table 68.5.

The less liquid markets, such as the Dutch CBS index, are typically quoted as a spread to the HICPxT. For example, if the five-year breakeven rate for HICPxT equals 2% and the Dutch CBS index is quoted at 50 basis points, this means that the five-year breakeven rate for the Dutch CBS index equals 2.50%.

Valuing Zero-Coupon Swaps

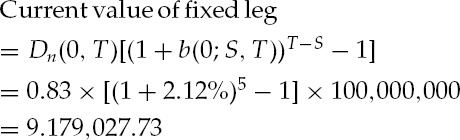

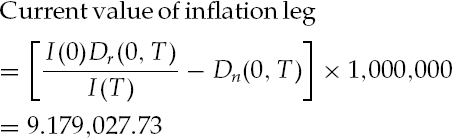

An inflation swap has an inflation period starting at time S and ending at T over which the inflation is computed and a single payment date, which typically equals T, when the inflation payment (on the inflation leg) is exchanged with a fixed amount (on the fixed leg). The inflation leg thus pays the net increase in reference numbers from S to T, where I(S) is known. The fixed leg pays a fixed amount which is conveniently written as an accumulated rate, b. The rate b is quoted in the market and called the breakeven swap rate. The rate b will differ depending on the current time and the inflation period, and therefore we use the notation b = b(0;S,T) for the breakeven swap rate today for an inflation period S to G. In general, S can be different from today. In the term sheet given in Table 68.3 we take S = 0l-Sep-06 and T = 01-Sep-ll and assume today is given by the September 21, 2006. The breakeven inflation swap rate quoted in the market equals b(0;01-Sep-06, 01-Sep-ll) = 2.12% and the discount factor for September 25, 2011 equals 0.83. Assuming a notional equal to €100,000,000 the value of the fixed leg can then be computed as:

The cash flow at maturity remains constant and therefore the fixed leg only varies with the discount factor. At inception the breakeven swap rate is set at such a level that the market considers the value of the fixed leg to equal the value of the uncertain inflation leg:

The only unknown on the inflation leg is the reference number at T. Using the concept of the inflation-linked zero-coupon bond introduced before we know that the current value of a payoff of I(T) at T equals I(0)Dr(0,T). This allows us to write the current value of the inflation leg as follows:

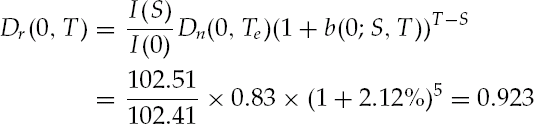

where the real discount bond, Dr(0,T), is the remaining unknown. Using the fact that the value of the fixed leg and inflation leg are equal at inception, we find that the value of Dr(0,T) consistent with the quoted breakeven swap rate equals:

where the value of the HICPxT index for June 2006 equals 102.51, the reference number today (September 21, 2006) equals 102.41, and as before the discount factor for September 25, 2011 equals 0.83.

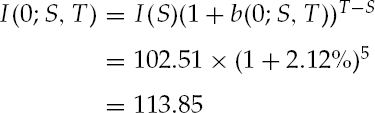

Besides a breakeven swap rate for the swap, we can also compute a breakeven reference number for the zero-coupon inflation swap which we denote by I(0;S,T). It is given by:

It is also easy to show that the start date of the period does not matter. Plugging in the bootstrapped value for Dr(0,T) gives:

One can easily check that I(0)Dr(0,T) = I(0,T)Dn(0,T). We have 102.41 × 0.923 = 113.85 × 0.83. As a special case of our extended definition of the breakeven swap rate, we have:

for a zero-coupon inflation swap with inflation period from today (t = 0) to T.

In the previous section I introduced and described the (fixed) zero-coupon inflation swap. Besides zero-coupon inflation swaps a number of other inflation swaps are traded, which are typically portfolios of zero-coupon swaps in one way or the other. Most are straightforward portfolios of spot starting zero-coupon inflation swaps. Here, a period-on-period (p-o-p) inflation swap which is a portfolio of forward starting zero-coupon swaps is described.

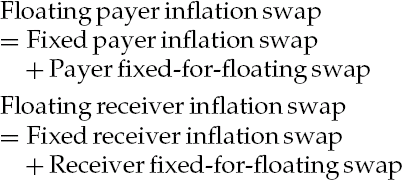

The inflation buyer (also called the inflation receiver) pays a predetermined fixed or floating rate (usually minus a spread). In return, the inflation buyer receives from the inflation seller (also called the inflation payer) inflation-linked payment(s). Two main types of (zero-coupon) inflation swaps exist: fixed inflation swaps (inflation versus fixed rate) and floating inflation swaps (inflation versus floating rate, usually Libor).

We call an inflation swap a payer inflation swap if you pay inflation and a receiver inflation swap if you receive inflation. Using an interest rate swap (IRS), we can find a no-arbitrage relationship between fixed and floating inflation swaps which we call the inflation swap parity:

A period-on-period swap has multiple payments during its life. It pays the inflation over a number of accrual periods. The most common structure is the year-on-year (y-o-y) inflation swap, which pays annual inflation at the end of each year. An example term sheet is given in Table 68.6. The y-o-y inflation swap in Table 68.6 is initiated on September 21,2006 and the inflation payer pays five times annual inflation from June to June every September 25 in the years 2006, ...,2011.

The cash flows on the inflation leg can be replicated using a series of forward starting zero-coupon inflation swaps. In the above example, we enter into forward starting zero-coupon swaps paying June 2006-2007 inflation,..., June 2010-2011 inflation. Therefore, the valuation can be done in terms of forward starting zero-coupon swaps. The valuation of forward starting zero-coupon swaps is not straightforward and involves modeling assumptions. Although the year-on-year inflation swap is the most popular instrument, other period-on-period swaps trade as well. We make a distinction between what we call pure period-on-period inflation swaps and annu-alized period-on-period inflation swaps.

Table 68.6. Example of a term sheet for HICPxT year-on-year inflation swap

Notional: | €100,000,000 |

Index: | HICPxT (non revised) |

Source: | First publication by Eurostat as shown on Bloomberg CPTFEMU |

Trade date: | 21-Sep-2006 |

Start date: | 25-Sep-2006 (Trade date + 2 business days) |

End date: | 25-Sep-2011 (Start date + tenor (5 years)) |

Rolls: | 25th |

Payment: | Annual, modified following |

Day count: | 30/360 unadjusted |

First fixing | 102.51 (June 2006) |

First rate: | 2.10% |

Fixed leg: | day count fraction X fixed rate |

Inflation leg: |

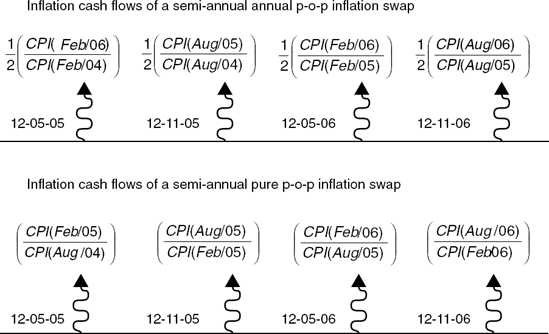

A pure p-o-p inflation swap pays the inflation over the period on the inflation leg. For example, a semi-annual pure p-o-p inflation swap with contract months June and December pays the net increase in the index from June to December and the net increase from June to December. As the inflation payments are not on an annual basis, seasonally is an important issue when valuing these swaps.

Just like a y-o-y inflation swap, an annual p-o-p inflation swap pays annual inflation, but it pays it at a higher frequency and weighted with the appropriate day count fraction. For example, a semiannual annual p-o-p inflation swap with contract months June and December pays half the net index increase from last June to June and half the net index increase from last December to December. (See Figure 68.6.)

As the period for a year-on-year swap equals a year, a y-o-y inflation swap falls in both categories.

As seasonality plays a role in valuing the pure period-on-period swaps, they would trade at a premium as the inflation seller needs to be rewarded for taking on the seasonal risk. Using high frequency (e.g., monthly) annualised period-on-period inflation swaps seems quite attractive as it spreads inflation payments over the year instead of one lump sum payment each year without a seasonality premium as seasonality does not affect the valuation.

The Chicago Mercantile Exchange (CME) started trading futures on the U.S. CPI inflation index in February 2004.

The figure plots the inflation leg cash flows from a semiannual p-o-p inflation swap with annual inflation periods and pure semi-annual inflation swaps. The fixed/floating leg payments are omitted.

The main advantage of CPI futures over zero-coupon inflation swaps is mitigated counterparty risk. The CPI futures traded on the CME are designed to resemble the Eurodollar futures contract. Likely due to the ill design of the CPI future (the contract traded annualised quarterly inflation), the market so far never really took off.

The CME started trading inflation futures on the Euro Consumer Price Index (HICPxT) in September 2005. One of the main advantages of the euro contract over the U.S. is that the inflation is annual. The main characteristics of the HICPxT contract are summarized in Table 68.7.

Considering their short maturity inflation futures complement the inflation-linked bond markets and allow investors to hedge short-term inflation exposures. As the futures trade on 12 consecutive months, investors can also take a view on inflation seasonality or hedge seasonality risk.

Limited Price Index Swaps

The Limited Price Index (LPI) swap is a typical U.K. instrument as U.K. pension funds that have limited indexation schemes. LPI swaps can come in a variety of flavors, but what they have in common is that, in one way or another, the inflation payment is capped and/or floored. If the inflation payment is both capped and floored, we call it collared. The most common traded LPI swap is the zero-coupon LPI swap. The zero-coupon LPI swap is particularly useful for pension funds that have liabilities related to the limited indexation of pensions in deferment as introduced in the 1995 Pension Act. They have liabilities of the following form:

Table 68.7. Contract specification for the Euro Consumer Price Index HICPxT inflation futures

Reference index | 100 - annual inflation rate in the 12 month period preceding the contract month based on the Eurozone Harmonised Index of Consumer Prices excluding tobacco published by Eurostat. The same index is used for the French, Italian and Greek Euro inflation-linked bonds. |

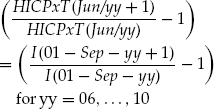

Settlement price | Final settlement amounts to 100 less the annual %-change in the HICPxT over the past 12 months and is rounded to four decimal places. Thus: |

where Ti denotes the contract month and Ti−12 the base month. For example, for the July 2004 contract the relevant HICPxT index values are June 2004 (115.10, released July 16, 2004) and July 2003 (112.70, released July 18, 2003). The final settlement price would have been: | |

A price of over 100 indicates deflation during the past 12-month period. | |

Contract months | 12 consecutive calendar months. |

Contract size | €10,000 times reference index. |

Minimum tick size | 0.01 index points, which amounts to ɛ100.00. |

Expiry date | Trading finishes 4:00 P.M. Greenwich Mean Time (GMT) on the business day preceding the scheduled day the HICPxT announcement is made in the contract month. In case the announcement is postponed beyond the contract month, trading ceases at 4:00 P.M. GMT on the last business day of the contract month. |

where L(0) denotes the liability when the retiree retires. The difference between Ti-1 and Ti is usually a year. (See Table 68.8 for an example term sheet.)

The zero-coupon LPI swap is a highly path-dependent product. Other values for the cap and floor can be used (e.g. 0% and 3% is not uncommon). The 0% and 5% used are a result of the 1995 Pension Act legislation.

Real Swaptions

In the nominal interest rate market swaptions are (with caps and floors) the primary interest rate volatility instruments. Although nominal swaptions trade as exchanges of fixed versus floating coupons they can be seen as an option to exchange a fixed coupon bond versus a floating rate bond by including an offsetting notional exchange at the final payment. For the real swaption we discuss here, we use a similar concept. We apply the idea of having an option to exchange an inflation-linked bond versus a floating rate bond. The difference with the nominal case is the inflation uplift on the notional for an inflation-linked bond. Where a nominal bond pays the notional at maturity an inflation-linked bond pays the notional times the inflation uplift, that is,

In order to correct for this we add a payment of I(T)/I(0) −1 to the inflation leg at maturity of the swap.

Note that we have chosen the unknown index for 2007 as the base in the inflation leg rather than the index for 2006.

Table 68.8. Example of a Term Sheet for LPI (0%-5%) Swap

Notional: | £ 100,000,000 |

Index: | UK RPI (nonrevised) |

Source: | First publication by National Statistics as shown on Bloomberg UKRPI |

Trade date: | 21-Sep-2006 |

Start date: | 25-Sep-2006 (Trade date + 2 business days) |

End date: | 25-Sep-2036 (Start date + tenor (30 years)) |

First fixing: | 198.50 (June 2006) |

Fixed leg: | (1 + 3.02%)30 |

Inflation leg: |

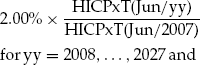

Table 68.9. Example of a Term Sheet for Real Swaption on HICPxT

Notional: | 100,000,000 |

Index: | HICPxT (non revised) |

Source: | First publication by Eurostat as shown on Bloomberg CPTFEMU |

Trade date: | 21-Sep-2006 |

Maturity date: | 25-Sep-2007 |

Swap Start date: | 25-Sep-2007 |

Swap end date: | 25-Sep-2027 (Start date + tenor (20 years)) |

Rolls: | 25th September, modified following. |

First fixing: | 102.51 (June 2006) |

Floating leg: | 12m EURIBOR |

Inflation leg: | |

This has advantages for the valuation of the real swaption. Using the current construction the real swaption can be valued using similar techniques as nominal swaptions. In case we would have used 2006 as the base the valuation becomes substantially harder as certain convexity adjustments need to be made.

In 2005 the International Swap and Derivatives Association (ISDA) published documentation on inflation definitions supplementing the ISDA Master Agreements. The main issues relate to delay and disruption in the publication of the inflation index. Furthermore, it defines the most relevant indices. Here I will discuss the most important problems that can occur while settling an inflation derivatives contract.

If an inflation index is not published on time a substitute index is used. If the inflation index has not been published five business days prior to the next payment date for the transaction related to that index, the calculation agent, which is specified in the term sheet, shall use a substitute index level using the following methodology:

If applicable, the calculation agent takes the same action to determine the substitute index level as that specified in the terms and conditions of the related bond. The related bond, if any, is specified in the confirmation of the trade. A related bond is typically specified for asset swaps, but not for inflation swaps.

If (1) does not result in a substitute index level for the affected payment date the calculation agent determines the substitute index level as follows:

where

Base level means the level of the index 12 calendar months prior to the month for which the substitute index level (definitive or provisional) is being determined, for example, December 2006.

Latest level means the latest available level (definitive or provisional) for the index, for example, November 2006.

Reference level means the level (definitive or provisional) of the index 12 calendar months prior to the month to which the latest level is referring, for example, November 2005.

If a relevant level is published after five business days prior to the next payment date, no adjustments will be made to the transaction. The determined substitute reference level will be the definitive level for that reference month.

If the inflation index no longer gets published, a replacement index will be used. If, during the term of the transaction, the index sponsor announces that an index will no longer be published or announced but will be superseded by a replacement index specified by the index sponsor, and the calculation agent determines that the replacement index is calculated using the same or similar methodology as the original index, this index is deemed the successor index.

If an index has not been published for two consecutive months or if the index sponsor (publisher) has announced that it will no longer publish the index, the calculation agent shall determine a successor index for the purpose of the transaction using the following methodology:

If a successor index has been designated by the calculation agent pursuant to the terms and conditions of the related bond, such successor index shall be designated a successor index hereunder.

If no related bond exists, the calculation agent shall ask five leading independent dealers to state what the replacement index shall be. If three or more dealers out of at least four responses state the same index, this index will be deemed the successor index. If, out of three responses, two or more dealers state the same index, this index will be deemed the successor index. If no successor index has been decided following responses from dealers by the third business day prior to the next payment date or by the date that is five business days after the last payment date (if no further payment dates are scheduled), the calculation agent determines an appropriate alternative index. This alternative index will be deemed the successor index. If the calculation agent determines that there is no appropriate alternative index, a termination event occurs and both parties are affected parties as defined in the 2002 ISDA Master Agreement.

If an index is rebased the rebased index will be used going forward. If the calculation agent determines that the index has been or will be rebased at any time, the rebased index will be used from then on. However, the calculation agent shall make adjustments pursuant to the terms and conditions of the related bond, if any. If there is no related bond, the calculation agent shall make adjustments to the past levels of the rebased index so that rebased index levels prior to the rebase date reflect the same inflation rate as before it was rebased.

If prior to five business days before a payment date an index sponsor announces that it will make a material change to an index, then the calculation agent shall make any adjustments to the index consistent with adjustments made to the related bond. If there is no related bond, only those adjustments necessary for the modified index to continue as the index will be made.

If, within 30 days of publication, the calculation agent is notified that the index level has to be corrected to remedy a material error in its original publication, the calculation agent will notify the parties of the correction and the amount payable as a result of that correction.

In this chapter I have discussed a number of underlying key concepts for understanding the need for inflation derivatives. It was shown that nominal cash flows can be transformed into real cash flows using inflation cash products and more flexible using inflation derivatives. The key instrument in the inflation market is the zero-coupon inflation swap which naturally performs the role of transforming nominal cash flows into real cash flows.

Belgrade, N., Benhamou, E., and Koehler, E. (2004). A market model for inflation. Working Paper, CDC Ixis Capital Markets.

Deacon, M., Derry, A., and Mirfendereski, D. (2004). Inflation-Indexed Securities, 2nd edition. London: John Wiley & Sons.

Hughston, L. (1998). Inflation derivatives. Working Paper, Merrill Lynch.

Mercurio, F. (2005). Pricing inflation-indexed derivatives. Quantitative Finance 5: 289-302.

Mercurio, F, and Moreni, N. (2006). Inflation with a smile. Risk 68: 70-75.

Any opinions expressed within this chapter are those of the author acting in a personal capacity and do not necessarily represent the views of Morgan Stanley. The content is provided on an 'as is' basis and no reliance should be placed on it. No representation or warranty is given as to accuracy, completeness, fitness for purpose or otherwise.