ROBERT DUBIL, PhD

Associate Professor, Lecturer of Finance, David Eccles School of Business, University of Utah

Abstract: From a structural point of view, all financial markets, whether for equities, bonds, currencies, or commodities, are the same. They all have distinct primary issuers and secondary traders. They all have spot, forward, and option vehicles. They all have two types of traders—hedgers and speculators—with two different trading motives. And in all markets, the primary trading strategy driving most of activity is relative risk arbitrage, whose goal is to earn reward for taking on exposure to secondary risk factors while eliminating primary directional risks through static or dynamic hedging.

Keywords: spot markets, forward markets, contingent claims, relative-value arbitrage, pure arbitrage, speculation, hedging, risk sharing, cash-and-carry

Financial markets play a major role in allocating wealth and excess savings to productive ventures in the global economy. This extremely desirable process takes on various forms. Commercial banks solicit depositors' funds in order to lend them out to businesses that invest in manufacturing and services or to home buyers who finance new construction or redevelopment. Investment banks bring to market offerings of equity and debt from newly formed or expanding corporations. Governments issue short- and long-term bonds to finance construction of new roads, schools, and transportation networks. Investors—bank depositors and securities buyers—-supply their funds in order to shift their consumption into the future by earning interest, dividends, and capital gains.

The process of transferring savings into investment involves various market participants: individuals, pension and mutual funds, banks, governments, insurance companies, industrial corporations, stock exchanges, over-the-counter dealer networks, and others. All these agents can at different times serve as demanders and suppliers of funds, and as transfer facilitators.

Market participants design optimal securities and institutions to make the process of transferring savings into investment most efficient. "Efficient" means to produce the best outcomes—lowest cost, least disputes, fastest, and so on—from the perspective of security issuers and investors, as well as for the society as a whole. In this chapter we briefly discuss some fundamental questions about today's financial markets. Why do we have things like stocks, bonds, or mortgage-backed securities? Are they outcomes of optimal design or happenstance? Do we really need "greedy" investment bankers, securities dealers, or brokers soliciting us by phone to purchase unit trusts or mutual funds? What role do financial exchanges play in today's economy? Why do developing nations strive to establish stock exchanges even though often they do not have any stocks to trade on them?

Once we have basic answers to these questions, it will not be difficult to see why almost all the financial markets are organically essentially the same. Like automobiles made by Toyota and Volkswagen, which all have an engine, four wheels, a radiator, a steering wheel, and so on, all interacting in a predetermined way, all markets, whether for stocks, bonds, commodities, currencies, or any other claims to purchasing power, are built from the same basic elements.

All markets have two separate segments: original issue and resale. These are characterized by different buyers and sellers and different intermediaries. They perform different timing functions. The first transfers capital from the suppliers of funds (investors) to the demanders of capital (businesses). The second transfers capital from the suppliers of capital (investors) to other suppliers of capital (investors). The two segments are:

Primary markets (issuer-to-investor transactions with investment banks as intermediaries in the securities markets, and banks, insurance companies and others in the loan markets)

Secondary markets (investor-to-investor transactions with broker-dealers and exchanges as intermediaries in the securities markets, and mostly banks in the loan markets)

All markets have the originators, or issuers, of the claims traded in them (the original demanders of funds) and two distinctive groups of agents operating as investors, or suppliers of funds. The two groups of funds suppliers have completely divergent motives. The first group aims to eliminate any undesirable risks of the traded assets and earn money on repackaging risks; the other actively seeks to take on those risks in exchange for uncertain compensation. The two groups are:

Hedgers: Dealers who aim to offset primary risks, be left with short-term or secondary risks, and earn spread from dealing

Speculators: Investors who hold positions for longer periods without simultaneously holding positions that offset primary risks

The claims traded in all financial markets can be delivered in three ways. The first is an immediate exchange of an asset for cash. The second is an agreement on the price to be paid, with the exchange taking place at a predetermined time in the future. The last is a delivery in the future contingent upon an outcome of a financial event (e.g., level of stock price or interest rate), with a fee paid up front for the right of delivery. The three market segments based on the delivery type are:

Spot or cash markets (immediate delivery)

Forward markets (mandatory future delivery or settlement)

Options markets (contingent future delivery or settlement)

We focus on these structural distinctions to bring out the fact that all markets not only transfer funds from suppliers to users, but also risk from users to suppliers. They allow risk transfer or risk sharing between investors. The majority of the trading activity in today's market is motivated by risk transfer, with the acquirer of risk receiving some form of sure or contingent compensation. The relative price of risk in the market is governed by a web of relatively simple arbitrage relationships that link all the markets.

These allow market participants to assess instantaneously the relative attractiveness of various investments within each market segment or across all of them. Understanding these relationships is mandatory for anyone trying to make sense of the vast and complex web of today's markets. Our line of thought here is adapted from Chapter 1 of Dubil (2004).

All financial contracts, whether in the form of securities or not, can be viewed as bundles, or packages of unit payoff claims (mini-contracts), each for a specific date in the future and a specific set of outcomes. In financial economics, these are referred to as state-contingent claims.

Let us start with the simplest illustration: an insurance contract. A one-year life insurance policy promising to pay $1 million in the event of the insured's death can be viewed as a package of 365 daily claims (lottery tickets), each paying $1 million if the holder dies on that day. The value of the policy up front (the premium) is equal to the sum of the values of all the individual tickets. As the holder of the policy goes through the year, he can discard tickets that did not pay off, and the value of the policy to him diminishes until it reaches zero at the end of the coverage period.

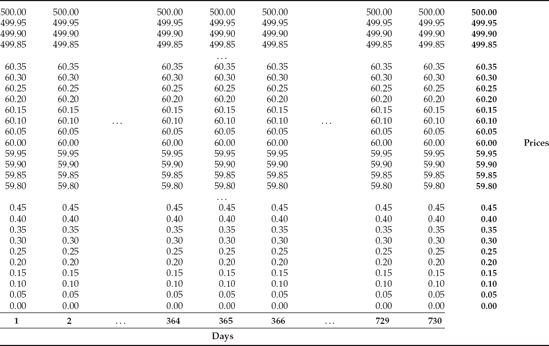

Let us apply the concept of state-contingent claims to known securities. Suppose you buy one share of XYZ SA stock currently trading at $45 per share. You intend to hold the share for two years. To simplify things, we assume that the stock trades in increments of $0.05 (tick size). The minimum price is $0 (a limited liability company cannot have a negative value) and the maximum price is $500. The share of XYZ SA can be viewed as a package of claims. Each claim represents a contingent cash flow from selling the share for a particular price at a particular date and time in the future. We can arrange the potential price levels from $0 to $500 in increments of $0.05 to have overall 10001 price levels. We arrange the dates from today to two years from today (our holding horizon). Overall, we have 730 dates. The stock is equivalent to 10,001 times 730, or 7,300,730 claims. The easiest way to imagine this set of claims is as a rectangular chessboard as shown in Table 8.1, where on the horizontal axis we have time and on the vertical the potential values the stock can take on (states of nature). The price of the stock today is equal to the sum of the values of all the claims, that is, all the squares of the chessboard.

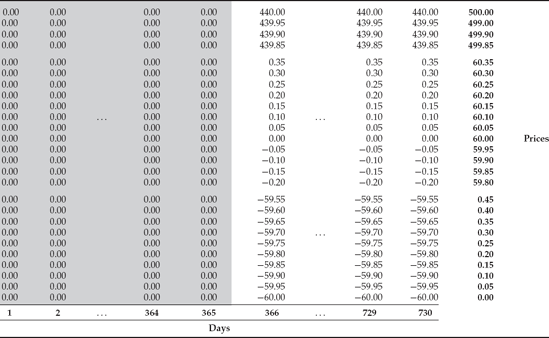

A forward contract on XYZ SA's stock can be viewed as a subset of this rectangle. Suppose we enter into a contract today to purchase the stock one year from today for $60. We intend to hold the stock for one year after that. The forward can be viewed as 10,001 by 365 rectangles with the first 365 days' worth of claims taken out (that is, we are left with the latter 365 columns of the board; the first 365 are taken out), as in Table 8.2. The cash flow of each claim is equal to the difference between the stock price for that state of nature and the contract price of $60. A forward carries an obligation on both sides of the contract, so some claims will have a positive value (stock is above $60) and some negative (stock is below $60).

Table 8.1. Stock Held for Two Years as a Chessboard of Contingent Claims in Two Dimensions: Time (Days 1 through 730) and Prices ($0 through $500)

|

Table 8.2. One-Year Forward Buy at $60 of Stock as a Chessboard of Contingent Claims (Payoff in Cells Equal to S-60 for Year 2; No payoff in Year 1)

|

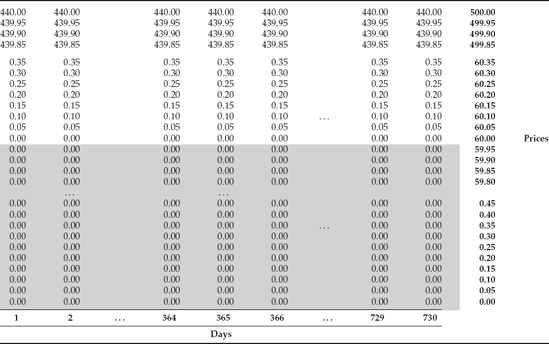

Table 8.3. American Call Struck at $60 with an Expiry in Two Years as a Chessboard of Contingent Claims (Payoff in Cells Equal to S −60 if S < 60)

|

An American call option contract to buy XYZ SA's shares for $60 with an expiry two years from today (exercised only if the stock is above $60) can be represented as an 8,800 × 730 subset of our original rectangular 10,001 × 730 chessboard. This time, the squares corresponding to the stock prices of $60 or below are eliminated, because they have no value, as in Table 8.3. The payoff of each claim is equal to the intrinsic (exercise) value of the call. As we will see later, the price of each claim today is equal to at least that.

Spot securities, forwards, and options are discussed in detail in subsequent chapters. Here, we briefly touch on the valuation of securities and state-contingent claims. The fundamental tenet of the valuation is that if we can value each claim (chessboard square) or small sets of claims (entire sections of the chessboard) in the package, then we can value the package as a whole. Conversely, if we can value a package, then often we are be able to value smaller sub-sets of claims (through a "subtraction"). In addition, we are sometimes able to combine very disparate sets of claims (stocks and bonds) to form complex securities (e.g., convertible bonds). By knowing the value of the combination, we can infer the value of a subset (bullet bond).

In general, the value of a contingent claim does not stay constant over time. If the holder of the life insurance becomes sick during the year and the likelihood of his death increases, then likely the value of all claims increases. In the stock example, as information about the company's earnings prospects reaches the market, the price of the claims changes. Not all the claims in the package have to change in value by the same amount. An improvement in the earnings prospects for the company may be only short term. The policyholder's likelihood of death may increase for all the days immediately following his illness, but not for more distant dates. The prices of the individual claims fluctuate over time, and so does the value of the entire bundle. However, at any given moment in time, given all information available as of that moment, the sum of the values of the claims must be equal to the value of the package, the insurance policy, or the stock. We always restrict the valuation effort to here and now, knowing that we will have to repeat the exercise an instant later.

Let us fix the time to see what assumptions we can make about some of the claims in the package. In the insurance policy example, we may surmise that the value of the claims for far-out dates is greater than that for near dates, given that the patient is alive and well now, and barring an accident, he is relatively more likely to take time to develop a life-threatening condition. In the stock example, we assigned the value of $0 to all claims in states with stock exceeding $500 over the next two years, as the likelihood of reaching these price levels is almost zero. We often assign the value of zero to claims for far dates (e.g., beyond 100 years), since the present value of those payoffs, even if they are large, is close to zero. We reduce a numerically infinite problem to a finite one. We cap the potential states under consideration, future dates and times.

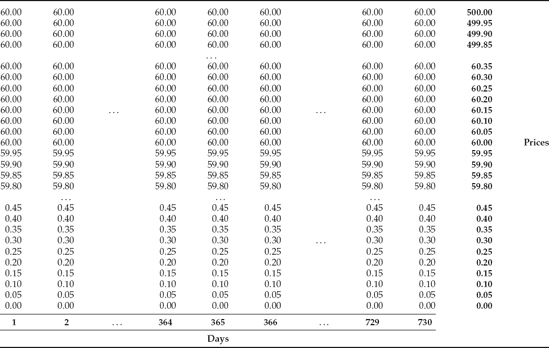

Table 8.4. Stock Plus Short American Call Struck at $60 as a Chessboard of Contingent Claims (Payoff in Cells Equal to 60 if S > 60 and to S if S < 60)

|

A good valuation model has to strive to make the values of the claims in a package independent of each other. In our life insurance policy example, the payoff depends on the person's dying on that day and not on whether the person is dead or alive on a given day. In that setup, only one claim out of the whole set will pay. If we modeled the payoff to depend on being dead and not dying, all the claims after the morbid event date would have positive prices and would be contingent on each other. Sometimes, however, even with the best of efforts, it may be impossible to model the claims in a package as independent. If a payoff at a later date depends on whether the stock reached some level at an earlier date, the later claim's value depends on the prior one. A mortgage bond's payoff at a later date depends on whether the mortgage has not already been prepaid. This is referred to as a survival or path-dependence problem. Our imaginary two-dimensional chessboards cannot handle path dependence, and we ignore this dimension of risk throughout the book as it adds very little to our discussion.

Let us turn to the definition of risk sharing: Risk sharing is a sale, explicit or through a side contract, of all or some of the state-contingent claims in the package to another party.

In real life, risk sharing takes on many forms. The owner of the XYZ share may decide to sell a covered call on the stock (see Chapter 14 of Volume I). If he sells an American-style call struck at $60 with an expiry date of two years from today, he gives the buyer the right to purchase the share at $60 from him even if XYZ trades higher in the market (e.g., at $75). The covered call seller is choosing to cap his potential payoff from the stock at $60 in exchange for an up-front fee (option premium) he receives. This corresponds to exchanging the squares corresponding to price levels above $60 (with values between $60 and $500) for squares with a flat payoff of $60, as illustrated in Table 8.4.

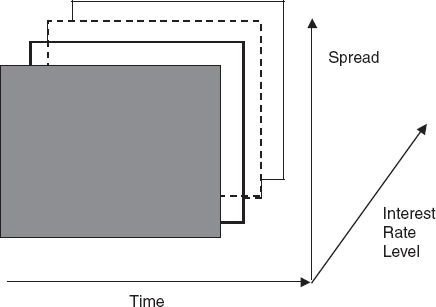

Another example of risk sharing can be a hedge of a corporate bond with a risk-free government bond. A hedge is a sale of a package of state-contingent claims against a primary position that eliminates all the essential risk of that position. Only a sale of a security that is identical in all aspects to the primary position can eliminate all the risk. A hedge always leaves some risk unhedged! Let us examine a very common hedge of a corporate with a government bond. An institutional trader purchases a 10-year 5% coupon bond issued by XYZ Corporation. In an effort to eliminate interest rate risk, the trader simultaneously shorts a 10-year 4.5% coupon government bond. The size of the short is duration-matched to the principal amount of the corporate bond. This guarantees that for small parallel movements in the interest rates, the changes in the values of the two positions are identical but opposite in sign. If interest rates rise, the loss on the corporate bond holding will be offset by the gain on the shorted government bond. If interest rates decline, the gain on the corporate bond will be offset by the loss on the government bond. The trader, in effect, speculates that the credit spread on the corporate bond will decline. Irrespective of whether interest rates rise or fall, whenever the XYZ credit spread declines, the trader gains since the corporate bond's price goes up more, or goes down less, than that of the government bond. Whenever the credit standing of XYZ worsens and the spread rises, the trader suffers a loss. The corporate bond is exposed over time to two dimensions of risk, interest rates and corporate spread. Our chessboard representing the corporate bond becomes a large rectangular cube, with time, interest rate, and credit spread as dimensions, as illustrated in Figure 8.1. The government bond hedge eliminates all potential payoffs along the interest rate axis, reducing the cube to a plane, with only time and credit spread as dimensions.

Practically any hedge position can be thought of in the context of a multidimensional cube defined by time and risk axes. The hedge eliminates a dimension or a subspace from the cube.

Most people view financial markets like a Saturday bazaar. Buyers spend their cash to acquire paper claims on future earnings, coupon interest, or insurance payouts. If they buy good claims, their value goes up and they can sell them for more; if they buy bad ones, their value goes down and they lose money.

When probed a little more on how markets are structured, most finance and economics professionals provide a seemingly more complete description, adding detail about who buys and sells what and why in each market. The respondent is likely to inform us that businesses need funds in various forms of equity and debt. They issue stock, lease- and asset-backed bonds, and unsecured debentures; sell short-term commercial paper; or rely on bank loans. Issuers get the needed funds in exchange for a promise to pay interest payments or dividends in the future. The legal claims on business assets are purchased by investors, individual and institutional, who spend cash today to get more cash in the future, that is, they invest. Securities are also bought and sold by governments, banks, real estate investment trust, leasing companies, and others. The cash-for-paper exchanges are immediate. Investors who want to leverage themselves can borrow cash to buy more securities, but through that they themselves become issuers of broker margin or bank loans. Both issuers and investors live and die with the markets. When stock prices increase, investors who have bought stocks gain. When stock prices decline, they lose. New investors have to "buy high" when share prices rise, but can "buy low" when share prices decline. The decline benefits past issuers who "sold high". The rise hurts them since they got little money for the sold stock and now have to deliver good earnings. In fixed-income markets, when interest rates fall, investors gain as the value of debt obligations they hold increases. The issuers suffer as the rates they pay on the existing obligations are higher than the going cost of money. When interest rates rise, investors lose as the value of debt obligations they hold decreases. The issuers gain as the rates they pay on the existing obligations are lower than the going cost of money.

In this view of the markets, both sides—the issuers and the investors—speculate on the direction of the markets. In a sense, the word investment is a euphemism for speculation. The direction of the market given the position held determines whether the investment turns out good or bad. Most of the time, current issuers and investors hold opposite positions (long vs. short): when investors gain, issuers lose, and vice versa. Current and new participants may also have opposite interests. When equities rise or interest rates fall, existing investors gain and existing issuers lose, but new investors suffer and new issuers gain.

The investor is exposed to market forces as long as he holds the security. He can enhance or mitigate his exposure, or risk, by concentrating or diversifying the types of assets held. An equity investor may hold shares of companies from different industrial sectors. A pension fund may hold some positions in domestic equities and some positions in domestic and foreign bonds to allocate risk exposure to stocks, interest rates and currencies. The risk is "good" or "bad" depending on whether the investor is long or short an exposure. An investor who has shorted a stock gains when the share price declines. A homeowner with an adjustable mortgage gains when interest rates decline (he is short interest rates) as the rate he pays resets lower, while a homeowner with a fixed mortgage loses as he is "stuck" paying a high rate (he is long interest rates).

While this standard description of the financial markets appears to be very comprehensive, it is rather like a two-dimensional portrait of a multidimensional object. The missing dimension here is the time of delivery. The standard view focuses exclusively on spot markets. Investors purchase securities from issuers or other investors and pay for them at the time of the purchase. They modify the risks the purchased investments expose them to by diversifying their portfolios or holding shorts against longs in the same or similar assets. Most tend to be speculators as the universe of hedge securities they face is fairly limited.

Let us introduce the time of delivery into this picture. That is, let us relax the assumption that all trades (that is, exchanges of securities for cash) are immediate. Consider an equity investor who agrees today to buy a stock for a certain market price, but will deliver cash and receive the stock one year from today. The investor is entering into a forward buy transaction. His risk profile is drastically different from that of a spot buyer. Like the spot stock buyer, he is exposed to the price of the stock, but his exposure does not start till one year from now. He does not care if the stock drops in value as long as it recovers by the delivery date. He also does not benefit from the temporary appreciation of the stock compared to the spot buyer who could sell the stock immediately. In our time-risk chessboard with time and stock price on the axes, the forward buy looks like a spot buy with a subplane demarcated by today and one year from today taken out. If we ignore the time value of money, the area above the current price line corresponds to "good" risk (that is, a gain), and the area below to "bad" risk (that is, a loss). A forward sell would cover the same subplane, but the good and the bad areas would be reversed.

Market participants can buy and sell not just spot but also forward. For the purpose of our discussion, it does not matter if, at the future delivery time, what takes place is an actual exchange of securities for cash, or just a marked-to-market settlement in cash. If the stock is trading at $75 in the spot market, whether the parties to a prior $60 forward transaction exchange cash ($60) for stock (one share) or simply settle the difference in value with a payment of $15 is quite irrelevant, as long as the stock is liquid enough so that it can be sold for $75 without any loss. Also, for our purposes, futures contracts can be treated as identical to forwards, even though they involve a daily settlement regimen and may never result in the physical delivery of the underlying commodity or stock basket.

Let us now further complicate the standard view of the markets by introducing the concept of contingent delivery time. A trade, or an exchange of a security for cash, agreed upon today, is not only delayed into the future, but is also made contingent upon a future event. The simplest example is an insurance contract. The payment of a benefit on a $1 million life insurance policy takes place only upon the death of the insured person. The amount of the benefit is agreed upon and fixed up front between the policy-holder and the issuing company. It can be increased only if the policyholder pays additional premium. Hazard insurance (fire, auto, flood) is slightly different from life in that the amount of the benefit depends on the "size" of the future event. The greater the damage is, the greater the payment is. An option contract is very similar to a hazard insurance policy. The amount of the benefit follows a specific formula that depends on the value of the underlying financial variable in the future (see Chapter 14 of Volume I). For example, a put option on the S&P 100 index traded on an exchange in Chicago pays the difference between the selected strike price and the value of the index at some future date and times $100, but only if the index goes down below that strike price level. The buyer thus insures himself against the index's going down, and the more the index goes down, the more benefit he obtains from his put option, just as if he held a fire insurance policy. Another example is a cap on an interest rate index that provides the holder with a periodic payment every time the underlying interest rate goes above a certain level. Borrowers use caps to protect themselves against interest rate hikes.

Options are used not only for obtaining protection, which is only one form of risk sharing, but also for risk taking, that is, providing specific risk protection for up-front compensation. A bank borrower relying on a revolving credit line with an interest rate defined as some spread over the U.S. prime rate or the three-month London Interbank Offered Rate (LIBOR) can sell floors to offset the cost of the borrowing. When the index rate goes down, he is required to make periodic payments to the floor buyer that depend on the magnitude of the interest rate decline. He willingly accepts that risk because when rates go down and he has to make the floor payments, the interest he is charged on the revolving loan also declines. In effect, he fixes his minimum borrowing rate in exchange for an up-front premium receipt.

Options are not the only packages of contingent claims traded in today's markets. In fact, the feature of contingent delivery is embedded in many commonly traded securities. Buyers of convertible bonds exchange their bonds for shares when interest rates and/or stock prices are high making the postconversion equity value higher than the present value of the remaining interest on the unconverted bond. Issuers call their outstanding callable bonds when interest rates decline below a level at which the value of those bonds is higher than the call price. Adjustable mortgages typically contain periodic caps, which prevent the interest rate and thus the monthly payment charged to the homeowner from changing too rapidly from period to period. Many bonds have credit covenants attached to them, which require the issuing company to maintain certain financial ratios, and noncompliance triggers automatic repayment or default. Car lease agreements give the lessees the right to purchase the automobile at the end of the lease period for a prespecified residual value. Lessees sometimes exercise those rights when the residual value is sufficiently lower than the market price of the vehicle. In many countries, including the United States, the homeowners with fixed-rate mortgages can prepay their loans partially or fully at any time without penalty. This feature allows the homeowners to refinance their loans with new ones when interest rates drop by a significant enough margin. The cash flows from the original fixed-rate loans are thus contingent upon interest rates staying high. Other examples abound.

The key to understanding these types of securities is the ability to break them down into simpler components: spot, forward, and contingent delivery. These components may trade separately in the institutional markets, but they are most likely bundled together for retail customers or original (primary market) acquirers. Not uncommonly, they are unbundled and rebundled several times during their lives.

Proposition. All financial market evolve to have three structural components: the market for spot securities, the market for forwards and futures, and the contingent securities market, which includes options and other derivatives.

All financial markets eventually evolve to have activity in three areas: spot trading for immediate delivery, trading with forward delivery, and trading with contingent forward delivery. Most of the activity of the last two forms is reserved for large institutions, which is why most people are unaware of them. Yet their existence is necessary for the smooth functioning of the spot markets. The trading for forward and contingent forward delivery allows dynamic risk sharing for holders of cash securities who trade in and out of contracts tied to different dates and future uncertain events. This risk-sharing activity, by signaling the constantly changing price of risk, in turn facilitates the flow of the fundamental information that determines the "bundled" value of the spot securities. In a way, the spot securities that we are all familiar with are the most complicated ones from the informational content perspective. Their value reflects all available information about the financial prospects of the entity that issued them and expectations about the broad market, and is equal to the sum of the values of all state-contingent claims that can be viewed as informational units. The value of forwards and option-like contracts is tied to more narrow information subsets. These contracts have an expiry date that is short relative to the underlying security and are tailored to a specific dimension of risk. Their existence allows the unbundling of the information contained in the spot security. This function is extremely desirable to holders of cash assets as it offers them a way to sell off undesirable risks and acquire desirable ones at various points in time. If you own a bond issued by a tobacco company, you may be worried that legal proceedings against the company may adversely affect the credit spread and thus the value of the bond you hold. You could sell the bond spot and repurchase it forward with the contract date set far into the future. You could purchase a spread-related option or a put option on the bond, or you could sell calls on the bond. All of these activities would allow you to share the risks of the bond with another party to tailor the duration of the risk sharing to your needs.

In this section, we introduce the notion of relative-value arbitrage, which drives the trading behavior of financial firms irrespective of the market they are engaged in. Relative arbitrage takes the concept of pure arbitrage beyond its technical definition of riskless profit. In it, all primary market risks are eliminated, but some secondary market exposures are deliberately left unhedged.

Arbitrage is defined in most textbooks as riskless instantaneous profit. It occurs when the law of one price, which states that the same item cannot sell at two different prices at the same time, is violated. The same stock cannot trade for one price at one exchange and for a different price at another unless there are fees, taxes, and the like. If it does, traders will buy it on the exchange where it sells for less and sell it on the one where it sells for more. Buying Czech korunas for British pounds cannot be more or less expensive than buying dollars for pounds and using dollars to buy korunas. If one can get more korunas for pounds by buying dollars first, no one will buy ko-runas for pounds directly. On top of that, anyone with access to both markets will buy korunas through dollars and immediately sell them for pounds to realize an instantaneous and riskless profit. This strategy is a very simple example of pure arbitrage in the spot currency markets. More complicated pure arbitrage involves forward and contingent markets. It can take a static form, where the trade is put on at the outset and liquidated once at a future date (e.g., trading forward rate agreements against spot LIBORs for two different terms), or a dynamic one, in which the trader commits to a series of steps that eliminate all directional market risks and ensures virtually riskless profit upon completion of these steps. For example, a bond dealer purchases a callable bond from the issuer, buys a swaption from a third party to offset the call risk, and delta-hedges the rate risk by shorting some bullet swaps. He guarantees himself a riskless profit provided that neither the issuer nor the swaption seller defaults.

Pure arbitrage is defined as generating riskless profit today by statically or dynamically matching current and future obligations to exactly offset each other, inclusive of incurring known financing costs. Not surprisingly, opportunities for pure arbitrage in today's ultra-sophisticated markets are limited. Most institutions' money-making activities rely on the principle of relative-value arbitrage. Hedge funds and proprietary trading desks of large financial firms, commonly referred to as arb desks, employ extensively relative arbitrage techniques. Relative-value arbitrage consists of a broadly defined hedge in which a close substitute for a particular risk dimension of the primary security is found and the law of one price is applied as if the substitute were a perfect match. Typically, the position in the substitute is opposite to that in the primary security in order to offset the most significant or unwanted risk inherent in the primary security. Other risks are left purposely unhedged, but if the substitute is well chosen, they are controllable (except in highly leveraged positions). Like pure arbitrage, relative arbitrage can be both static and dynamic. Let us consider examples of static relative arbitrage.

Suppose you buy $100 million of a 30-year U.S. government bond. At the same time you sell (short) $102 million of a 26-year bond. The amounts $100 and $102 are chosen through "duration matching" (see Chapter 14 of Volume III for a discussion of duration), which ensures that when interest rates go up or down by a few basis points the gains on one position exactly offset the losses on the other. The only way the combined position makes or loses money is when interest rates do not change in parallel; that is, the 30-year rates change by more or less than the 26-year rates. The combined position is not risk free. It is speculative, but only in a secondary risk factor. Investors hardly distinguish between 30- and 26-year rates; they worry about the overall level of rates. The two rates tend to move closely together. The relative arbitrageur bets that they will diverge.

The bulk of swap trading in the world relies on static relative arbitrage. An interest rate swap dealer agrees to pay a fixed-coupon stream to a corporate customer, himself an issuer of a fixed-rate bond. The dealer hedges by buying a fixed-coupon government bond. He eliminates any exposure to interest rate movements as coupon receipts from the government bond offset the swap payments, but is left with swap spread risk. If the credit quality of the issuer deteriorates, the swap becomes unfair and the combined position has a negative present value to the dealer.

Dynamic relative arbitrage is slightly more complicated in that the hedge must be rebalanced continuously according to very specific computable rules. A seller of a three-year over-the-counter equity call may hedge by buying three- and six-month calls on the exchange and shorting some of the stock. He then must rebalance the number of shares he is short on a daily basis as the price of those shares fluctuates. This so-called delta hedge (see Chapter 41 of Volume II) eliminates exposure to the price risk. The main unhedged exposure is to the implied volatility differences between the options sold and bought. In the preceding static swap example, the swap dealer may elect not to match the cash flows exactly on each swap he enters into. Instead, he may take positions in a small number of benchmark bonds in order to offset the cash flows in bulk. This shortcut, however, will require him to dynamically rebalance the portfolio of bonds.

Relative-value arbitrage is defined as generating profit today by statically or dynamically matching current and future obligations to nearly offset each other, net of incurring closely estimable financing costs. To an untrained eye, the difference between relative-value arbitrage and speculation is tenuous. To a professional, the two are easily discernible. A popular equity trading strategy called pairs trading is a good case in point. The strategy of buying Pfizer (PFE) stock and selling GlaxoSmithKline (GSK) is pure speculation. One can argue that both companies are in pharmaceuticals, both are large, and both have similar research-and-development budgets and new drug pipelines. The specific risks of the two companies, however, are quite different and they cannot be considered close substitutes. Buying Polish zlotys with British pounds and selling Czech korunas for British pounds is also an example of speculation, not of relative-value arbitrage. Polish zlotys and Czech korunas are not close substitutes. An in-between case, but clearly on the speculative side, is called a basis trade. An airline needing to lock in the future prices of jet fuel, instead of entering into a long-term contract with a refiner, buys a series of crude oil futures, the idea being that supply shocks that cause oil prices to rise affect jet fuel in the same way. When prices increase, the airline pays higher prices for jet fuel, but profits from oil futures offset those increases, leaving the total cost of acquiring jet fuel unchanged. Buying oil futures is appealing as it allows liquidating the protection scheme when prices decline instead of rising, or getting out halfway through an increase. This trade is not uncommon, but it exposes the airline to the basis risk. When the supply shocks take place at the refinery level, not the oil delivery level, spot jet fuel prices may increase more rapidly than crude oil futures.

Most derivatives dealers espouse the relative-value arbitrage principle. They sell options and at the same time buy or sell the underlying stocks, bonds, or mortgages in the right proportions to exactly offset the value changes of the sold option and the position in the underlying financial asset. Their lives are, however, quite complicated in that they have to repeat the exercise every day as long as the options they sold are alive, even if they do not sell additional options. This is because the appropriate proportions of the underlyings they need to buy or sell change every day. These proportions or hedge ratios depend on changing market factors. It is these market factors that are the secondary risks the dealers are exposed to. The dynamic rebalancing of the positions serves to create a close substitute to the options sold, but it does not offset all the risks.

Relative-value arbitrage in most markets relies on a building block of a static or dynamic cash-and-carry trade. The static version of the cash-and-carry trade (explained in Chapter 42 of Volume III) consists typically of a spot purchase (for cash) and a forward sell, or the reverse. The dynamic trade, like in the preceding option example, consists of a series of spot purchases or sales at different dates and a contingent payoff at the forward date. The glue that ties the spot and the forward together is the cost of financing, the "carry", of the borrowing to buy spot or lending after a spot sale. Even the most complicated structured derivative transactions are combinations of such building blocks across different markets. When analyzing such trades, focusing on institutional and market infrastructure details in each market can only becloud this basic structure of arbitrage. This book clarifies the essence of such trades by emphasizing common elements. It also explains why most institutions rely on the interaction of dealers on large trading floors to take advantage of inter-market arbitrages. The principle of arbitrage is exploited not only to show what motivates traders to participate in each market (program trading of stock index futures vs. stock baskets, fixed coupon stripping in bonds, triangular arbitrage in currencies), but also what drives the risk arbitrage between markets (simultaneous trades in currencies in money markets, hedging mortgage servicing contracts with swap options, etc.).

Many readers view no-arbitrage conditions found in finance textbooks as strict mathematical constructs. It should be clear from the preceding discussion that they are not mathematical at all. These equations do not represent the will of God like those pertaining to gravity or thermodynamics in physics. They stem from and are continuously ensured by the most basic human characteristic: greed. Dealers tirelessly look to discover pure and relative-value arbitrage (that is, opportunities to buy something at one price and to sell a disguised version of the same thing for another price). By executing trades to take advantage of the temporary deviations from these paramount rules, they eliminate them by moving prices back in line, where riskless money cannot be made and, by extension, the equations are satisfied. Each side of a financial math equation represents the present value of a pure arbitrage strategy. By spotting pure arbitrage and contrasting it with speculation, one is able to identify the in-between case of relative-value arbitrage (sometimes also referred to as risk arbitrage). Apart from the ever-shrinking commissions, most traders earn profit from "spread"—a reward for relative-value risk arbitrage. A swap trader who fixes the borrowing rate for a corporate client hedges by selling Treasury bonds. He engages in a relative-value trade (swaps vs. government bonds) that exposes him to swap spread movements. A bank that borrows by opening new checking deposits and lends by issuing mortgages eliminates the risk of parallel interest rate movements (which perhaps affect deposit and mortgage rates to the same degree), but leaves itself exposed to yield curve tilts (non-parallel interest rate movements) or default risk. In all these cases, the largest risks (the exposure to interest rate changes) are hedged out, and the dealer is left exposed to secondary ones (swap spread, default).

Most forms of what is conventionally labeled as investment under our definition qualify as speculation. A stock investor who does not hedge, or risk-share in some way, is exposed to the primary price risk of his asset. It is expected that in our lives, barring short-term fluctuations, the value of our assets increases over time. The economy in general grows, productivity increases, and our incomes rise as we acquire more experience. We find ourselves having to save for future consumption, family, and retirement. Most of the time, often indirectly through pension and mutual funds, we "invest" in real estate, stocks, and bonds. Knowingly or not, we speculate. Financial institutions, as their assets grow, find themselves in the same position. Recognizing that fact, they put their capital to use in new products and services. They speculate on their success. However, a lot of today's institutional dealers' trading activity is not driven by the desire to bet their institutions' capital on buy-low/sell-high speculative ventures. Institutional traders do not want to take primary risks by speculating on markets rising or falling. Instead, they hedge the primary risks by simultaneously buying and selling or borrowing and lending in spot, forward, and option markets. They leave themselves exposed only to secondary "spread" risks. Well-managed financial institutions are compensated for taking those secondary risks. Even most apt business school students often misunderstand this fine distinction between speculation and relative-value arbitrage. Chief executive officers often do, too. Nearly everyone has heard of the Barings, IG Metallgeselshaft, and Orange County fiascos of the 1990s. The history of finance is filled with examples of financial institutions gone bankrupt as a result of gambling.

Institutional trading floors are designed to best take advantage of relative arbitrage within each market. They are arranged around individual trading desks, surrounded by associated marketing and clearing teams, each covering customers within a specific market segment. Trading desks that are likely to buy each other's products are placed next to each other. Special proprietary desks (for short called prop or arb desks) deal with many customer desks of the same firm or other firms and many outside customers in various markets. Their job is to specifically focus on relative-value trades or outright speculation across markets. The distinction between the two types of desks—customer versus proprietary—is in constant flux as some markets expand and some shrink. Trading desks may collaborate in the types of transactions they engage in. For example, a money market desk arranges an issuance of short-term paper whose coupon depends on a stock index. It then arranges a trade between the customer and its swap desk to alter the interest rate exposure profile and between the customer and the equity derivatives desk to eliminate the customer's exposure to equity risk. The customer ends up with a low cost of financing and no equity risks. The dealer firm lays off the swap and equity risk with another institution. Hundreds of such intermarket transactions take place every day in the dealing houses in London, New York, and Hong Kong.

Commercial banks operate on the same principle. They bundle mortgage, car loan, or credit card receipts into securities with multiple risk characteristics and sell the unwanted ones to other banks. They eliminate the prepayment risk in their mortgage portfolios by buying swaptions from swap dealers.

Financial institutions can be broadly divided into two categories based on their raison d'être:

Asset transformers

Broker-dealers

The easiest way to identify them is by examining their balance sheets. Asset transformers' assets have different legal characteristics from their liabilities. Broker-dealers may have different mixes on the two sides of the balance sheet, but the categories tend to be the same.

An asset transformer is an institution that invests in certain assets, but issues liabilities in a form designed to appeal to a particular group of customers. The best example is a commercial bank. On the asset side, a bank issues consumer (mortgage, auto) and business loans, invests in bonds, and so on. The main form of liability it issues is checking accounts, saving accounts, and certificates of deposit (CDs). Customers specifically desire these vehicles as they facilitate their day-to-day transactions and often offer security of government insurance against the bank's insolvency. For example, in the United States the Federal Deposit Insurance Corporation (FDIC) guarantees all deposits up to $100,000 per customer per bank. The bank's customers do not want to invest directly in the bank's assets. This would be quite inconvenient, as they would have to buy and sell these bulky assets frequently to meet their normal living expenditures. From a retail customer's perspective, the bank's assets often have undesirably long maturity that entails price risk if they are sold quickly, and they are offered only in large denominations. In order to attract funding, the bank repackages its mortgage and business loan assets into liabilities, such as checking accounts and CDs, that have more palatable characteristics—immediate bankomat access, small denomination, short maturity, and deposit insurance. Another example of an asset transformer is a mutual fund (or a unit investment trust). A mutual fund invests in a diversified portfolio of stocks, bonds, or money market instruments, but issues to its customers small-denomination, easily redeemable participation shares (unit trust certificates) and offers a variety of services like daily net asset value calculation, fund redemption and exchange, or a limited check-writing ability. Other large-asset transformers are insurance companies that invest in real estate, stocks, and bonds (assets), but issue policies with payouts tied to life or hardships events (liabilities).

Asset transformers are subject to special regulations and government supervision. Banks require bank charters to operate, are subject to central bank oversight, and must belong to deposit insurance schemes. Mutual funds' regulation is aimed at protecting small investors (e.g., as provided for by the Investment Company Act in the United States). Insurance companies rates are often sanctioned by state insurance boards. The laws in all these cases set specific forms of legal liabilities asset transformers may create and sound investment guidelines they must follow (e.g., percentage of assets in a particular category). Asset transformers are compensated largely for their role in repackaging their assets with undesirable features into liabilities with customer-friendly features. That very activity automatically introduces great risks into their operations. Banks' liabilities have much shorter duration (checking accounts) than their assets (fixed-rate mortgages). If interest rates do not move in parallel, the spread they earn (interest differential between rates charged on loans and rates paid on deposits) fluctuates and can be negative. They pursue relative-value arbitrage in order to reduce this duration gap.

Broker-dealers do not change the legal and functional form of the securities they own and owe. They buy stocks, currencies, mortgage bonds, leases, and so on, and they sell the same securities. As dealers, they own them temporarily before they sell them, exposing themselves to temporary market risks. As brokers, they simply match buyers and sellers. Broker-dealers participate in both primary sale and secondary resale transactions. They transfer securities from the original issuers to buyers, as well as from existing owners to new owners. The first is known as investment banking or corporate finance, the latter as dealing or trading. The purest forms of broker-dealers exist in the United States and Japan, where the laws have historically separated them from other forms of banking. Most securities firms in those two countries are pure broker-dealers (investment banking, institutional trading, and retail brokerage) with an addition of asset-transforming businesses of asset management and lending. In most of continental Europe, financial institutions are conglomerates commonly referred to as universal banks, as they combine both functions. In recent years, with the repeal of the Glass-Steagall Act in the United States and the wave of consolidations taking place on both sides of the Atlantic, U.S. firms have the possibility to converge more closely to the European model. Broker-dealers tend to be much less regulated than asset transformers, and the focus of the laws tends to be on small-investor protection (securities disclosure, fiduciary responsibilities of advisers, etc.).

Asset transformers and broker-dealers compete for each other's business. Securities firms engage in secured and unsecured lending and offer check writing in their brokerage accounts. They also compete with mutual funds by creating bundled or indexed securities designed to offer the same benefits of diversification. In the United States, the trading on the American Stock Exchange is dominated by ETFs (exchange-traded funds), holding company depositary receipts (HOLDRs), Qubes (so named because of their QQQQ ticker symbol), and the like, all of which are designed to compete with index funds, instead of ordinary shares. Commercial banks securitize their credit card and mortgage loans to trade them out of their balance sheets. The overall trend has been toward disintermediation (that is, securitization of previously transformed assets into more standardized, tradeable packages). As burdensome regulations fall and costs of securitization plummet, retail customers are increasingly given access to markets previously reserved for institutions.

From the welfare perspective, the primary role of financial markets has always been to transfer funds between suppliers of excess funds and their users. The users include businesses that produce goods and services in the economy, households that demand mortgage and consumer loans, governments that build roads and schools, financial institutions, and many others. All of these economic agents are involved in productive activities that are deemed economically and socially desirable. Throughout most of the history, it was bankers and banks who made that transfer of funds possible by accepting funds from depositors and lending them to kings, commercial ventures, and others. With the transition from feudalism to capitalism came the new vehicles of performing that transfer in the form of shares in limited liability companies and bonds issued by sovereigns and corporations. Stock, bond, and commodity exchanges were formed to allow original investors in these securities to efficiently share the risks of these instruments with new investors. This in turn induced many suppliers of funds to become investors in the first place as the risks of holding paper were diminished. Paper could be easily sold and funds recovered. A specialized class of traders emerged who dealt only with trading "paper" on the exchanges or over the counter (OTC). To them, paper was and is faceless. At the same time, the old role of finding new productive ventures in need of capital shifted from bankers to investment bankers, who, instead of granting loans, specialized in creating new shares and bonds for sale to investors for the first time. To investment bankers, the paper is far from faceless. Prior to the launch of any issue, the main job of an investment banker or his corporate finance staff, like that of a loan banker, is to evaluate the issuing company's business and its financial condition and to prepare a valuation analysis for the offered security.

As we stated before, financial markets for securities are organized into two segments defined by the parties to a securities transaction: primary and secondary markets. This segregation exists only in securities, not in private-party contracts like OTC derivatives. In private contracts, the primary market issuers also tend to be the secondary market traders, and the secondary market operates through assignments and mark-to-market settlements rather than through resale.

In primary markets, the suppliers of funds transfer their excess funds directly to the users of funds through a purchase of securities. An investment banker acts as an intermediary, but the paper-for-cash exchange is between the issuing company and the investor. The shares are sold either publicly, through an initial public offering or a seasoned offering, or privately through a private placement with "qualified investors," typically large institutions. Securities laws of the country in which the shares are sold spell out all the steps the investment bank must take in order to bring the issue to market. For example, in the United States, the shares must be registered with the Securities and Exchange Commission (SEC), a prospectus must be presented to new investors prior to a sale, and so on. Private placements follow different rules, the presumption being that large qualified investors need less protection than retail investors. In the United States, they are governed by Rule 144-A, which allows their subsequent secondary trading through a system similar to an exchange.

In secondary markets, securities are bought and sold only by investors without the involvement of the original user of funds. Secondary markets can be organized as exchanges or as OTC networks of dealers connected by phone or computer, or the hybrid of the two. The Deutsche Börse and the New York Stock Exchange (NYSE) are examples of organized exchanges. It is worth noting, however, that exchanges differ greatly from each other. The NYSE gives access to trade flow information to human market makers called specialists to ensure the continuity of the market making in a given stock, while the Tokyo Stock Exchange is an electronic market where continuity is not guaranteed, but no dealer can earn monopoly rents from private information about buys and sells. Corporate and government bond trading are the best examples of OTC markets. There, as in swap and currency markets, all participants are dealers who trade one on one for their own account. They maintain contact with each other over a phone and computer network, and jointly police the fair conduct rules through industry associations. For example, in the OTC derivatives markets, the International Swaps and Derivatives Association (ISDA) standardizes the terminology used in quoting the terms and rates and formalizes the documentation used in confirming trades for a variety of swap and credit derivative agreements. The best example of a hybrid between an exchange and an OTC market is the National Association of Securities Dealers Automated Quotation System (NASDAQ) in the United States. The exchange is only virtual, as participants are connected through a computer system. Access is limited to members only, and all members are dealers.

Developing countries strive to create smooth-functioning secondary markets. They often rush to open stock exchanges even though there may only be a handful of companies large enough to have a significant number of dispersed shareholders. In order to improve the liquidity of trading, nascent exchanges limit the number of exchange seats to very few, the operating hours to sometimes only one per day, and so on. All these efforts are aimed at funneling all buyers and sellers into one venue. This parallels the goals of the specialist system on the NYSE. Developing countries' governments strive to establish a well-functioning government bond market. They start by issuing short-term obligations and introduce longer maturities as quickly as the market will have an appetite for them.

The main objective in establishing these secondary trading places is to lower the cost of raising capital in the primary markets by offering the primary market investors a large outlet for risk sharing. Unless investors are convinced that they can easily get in and out of these securities, they will not buy the equities and bonds offered by the issuers (local businesses and governments) in the first place. This "tail wagging the dog" pattern of creating secondary markets first is very typical not only for lesser developed nations, but is quite common in introducing brand new risk classes into the marketplace. In the late 1980s, Michael Milken's success in selling highly speculative high-yield bonds to investors relied primarily on creating a secondary OTC market by assuring active market making by his firm Drexel Burnham Lambert. Similarly, prior to its collapse in 2002, Enron's success in originating energy forwards and contingent contracts was driven by Enron's ability to establish itself as a virtual exchange of energy derivatives (with Enron acting as the monopolist dealer, of course). In both of these cases, the firms behind the creation of these markets failed, but the primary and secondary markets they started remained strong, the high-yield market being one of the booming high performers during the tech stock bubble collapse in 2000 to 2002.

According to a common saying, nothing in life is certain except death and taxes. No investment in the market is riskless, even if it is in some way guaranteed. Let us challenge some seemingly intuitive notions of what is risky and what is safe.

Sparkasse savers in Germany, postal account holders in Japan, and U.S. Treasury bill investors, for most intents and purposes, avoid default risk and are guaranteed a positive nominal return on their savings. T-bill and CD investors lock in the rates until the maturity of the instruments they hold. Are they then risk-free investors and not speculators? They can calculate in advance the exact dollar amount their investment will pay at maturity. After subtraction of the original investment, the computed percentage return will always be positive. Yet, by locking in the cash flows, they are forgoing the chance to make more. If, while they are holding their CD, short-term or rollover rates increase, they will have lost the extra opportunity return they could have earned. We are hinting here at the notion of opportunity cost of capital common in finance.

Let us consider another example. John Smith uses the $1,000 he got from his uncle to purchase shares in XYZ Corporation. After one year, he sells his shares for $1,100. His annual return is 10%. Adam Jones borrows $1,000 at 5% from his broker to purchase shares in XYZ Corporation. After one year, he sells his shares for $1,100. His annual return is 10% on XYZ shares, but he has to pay 5% or $50 interest on the loan, so his net return is 5%. Should we praise John for earning 10% on his capital and scold Adam for earning only 5%? Obviously not. Adam's cost of capital was 5%. So was John's! His was the nebulous opportunity cost of capital, or a shadow cost. He could have earned 5% virtually risk free by lending to the broker instead of investing in risky shares. So his relative return, or excess return, was only 5%. In our T-bill or CD example, one can argue that an investor in a fixed-rate CD is a speculator as he gambles on the rates not increasing prior to the maturity of his CD. The fact that his net receipts from the CD at maturity are guaranteed to be positive is irrelevant. There is nothing special about a 0% threshold for your return objective (especially if one takes into account inflation).

All investors who take a position in an asset, whether by borrowing or using owned funds, and the asset's return over its life is not contractually identical to the investor's cost of capital, can be considered speculators. This definition is relative only to some benchmark cost of capital. In this sense both Adam and John speculate by acquiring shares whose rate of return differs from their cost of capital of 5%. An outright CD investment is speculative, as the rate on the CD is not guaranteed to be the same as that obtained by leaving the investment in a variable-rate money market account. A homeowner who takes out a fixed-rate mortgage to finance a house purchase is a speculator even though he fixes his monthly payments for the next 30 years! When he refinances his loan, he cancels a prior bet on interest rates and places a new one. In contrast, an adjustable-rate mortgage borrower pays the fair market rate every period equal to the short-term rate plus a fixed margin.

Most financial market participants can be divided into two categories based on whether their capital is used to place bets on the direction of the market prices or rates or whether it isused to finance holdings of sets of transactions that largely offset each other's primary risks: speculators and hedgers.

Speculators are economic agents who take on explicit market risks in order to earn returns in excess of their cost of capital. The risks they are exposed to through their investments are not offset by simultaneous "hedge" transactions. Hedgers are economic agents who enter into simultaneous transactions designed to have offsetting market risks in such a way that the net returns they earn are over and above their cost of capital. All arbitrageurs, whether pure or relative, are hedgers. They aim to earn nearly risk free returns after paying all their financing costs. A pure arbitrageur's or strict hedger's returns are completely risk free. A relative arbitrageur's returns are not risk free; he is exposed to secondary market risks.

All investors who use their capital to explicitly take on market risks are speculators. Their capital often comes in the form of an outside endowment. Mutual funds obtain fresh funds by shareholders sending them cash. Pension funds get capital from payroll deductions. Insurance companies sell life or hazard policies and invest the premiums in stocks, bonds, and real estate. Individual investors deposit cash into their brokerage accounts in order to buy, sell, or short sell stocks and bonds. In all these cases, the investors use their funds (that is, sacrifice their cost of capital) to bet on the direction of the market they invest in. They "buy" the services of brokers and dealers who facilitate their investment strategies. In order to help these investors improve the precision of the bets they take, broker-dealers, who are hedgers by nature, invent new products, which they "sell" to the investors. These can be new types of bonds, warrants and other derivatives, new classes of shares, new types of trusts, and annuities. Often, the division of the players into speculators and hedgers is replaced by the alternative terms of buy-side participants and sell-side participants.

Buy-side players are investors who do not originate the new investment vehicles. They choose from a menu offered to them by the sell-side players. The sell-siders try to avoid gambling their own capital on the explicit direction of the market. They want to use their capital to finance the hedge, that is, to "manufacture" the new products. As soon as they sell them, they look to enter into a largely offsetting trade with another counterparty or to hedge the risks through a relative arbitrage strategy. Often the sell-sider's hedge strategies are imperfect and take time to arrange. That is when sell-siders act as speculators. The hedger/speculator compartmentalization is not exactly equivalent to sell-/buy-side division. Sell-siders often act as both hedgers and speculators, but their mindset is more like that of the hedger ("to find the other side of the trade"). Buy-siders enter into transactions with sell-siders in order to get exposed to, or alter how they are exposed to, market risks ("to get in on a trade").

We use quotes around the words buy and sell to emphasize that the sell-sider does not necessarily sell a stock or bond to a buy-sider. He can just as well buy it. But he hedges his transaction while the buy-sider does not.

Geographically, the sell-side resides in global financial centers, like New York or London, and is represented by the largest 50 global financial institutions. The buy-side is very dispersed and includes all medium and smaller banks with mostly commercial business, all mutual and pension funds, some university endowments, all insurance companies, and all finance corporations. The buy/sell and hedger/speculator distinctions have recently become blurred. Larger regional banks in the United States, which have traditionally been buy-side institutions, have started their own institutional trading businesses. They now offer security placement and new derivative product services to smaller banks and thrifts. In the 1990s, some insurance companies established sell-side trading subsidiaries and used their capital strength and credit rating to compete vigorously with broker-dealers. Most of these subsidiaries have the phrase "Financial Products" inserted in their name (e.g., Gen Re Financial Products or AIG FP).

One type of company that can be, by design, on both the buy and sell side is a hedge fund. Hedge funds are capitalized like typical speculators (read: investment companies), similar to mutual funds, but without the regulatory protection of the small investor. Yet almost all hedge fund strategies are some form of relative-value arbitrage; that is, they are hedges. The original capital is used only to acquire leverage and to replicate a hedge strategy as much as possible. Most hedge funds have been traditionally buy-siders. They have tended not to innovate, but to use off-the-shelf contracts from dealers. Sometimes, however, hedge funds grow so large in their market segment that they are able to wrest control of the demand-and-supply information flow from the dealers and are able to sell hedges to the dealers, effectively becoming sellers of innovative strategies. In the late 1990s, funds like Tiger, AIM, and Long-Term Capital Management, sometimes put on very large hedged positions, crowding dealers into speculative choices as the supply of hedges was exhausted by the funds. In the early 2000s, hedge funds retrenched to their traditional buy-side role as the average size of the fund declined. However, by 2006 the number of funds increased dramatically, topping 8,000 with assets over $1.2 trillion and some of the larger funds playing both buy- and sell-side roles.

From a structural point of view, all financial markets are the same in that they have the same (1) distinct primary issuers and secondary traders, (2) spot, forward, and option vehicles, (3) types of traders with two different trading motives (hedgers and speculators), and (4) primary trading strategy driving most of activity is relative risk arbitrage.

The goal of relative risk arbitrage is to earn reward for taking on exposure to secondary risk factors while eliminating primary directional risks through static or dynamic hedging. Taking an arbitrage perspective, in this chapter we explained how risk sharing drives most of the world's trading activity.

Arrow, K. J. (1951). Alternative approaches to the theory of choice in risk-taking situation. Econometrica 19, 4: 404– 737.

Baxter, M. and Rennie, A. (1996). Financial Calculus: An Introduction to Derivative Pricing, Cambridge: Cambridge University Press.

Cox, J. C. and Rubinstein, M. (1985). Options Markets. En-glewood Cliffs, NJ: Prentice-Hall.

Debreu, G. (1959). Theory of Value. New Haven, CT: Yale University Press.

Dubil, R. (2004). An Arbitrage Guide to Financial Markets. Chichester, England: John Wiley & Sons.

Fabozzi, F. J., Davis H. A., and Choudhry, M. (2006). Introduction to Structured Finance. Hoboken, NJ: John Wiley & Sons.

Huang, C. and Litzenberger, R. H. (1998). Foundations for Financial Economics. New York, NY: North-Holland.

Kolb, R. W. and Overdahl, J. A. (2003).Financial Derivatives, 3rd Ed. Hoboken, NJ: John Wiley & Sons.

Merton, R. C. (1990). Continuous-Time Finance. Cambridge, MA: Blackwell Publishers.

Neftci, S. N. (2004). Principles of Financial Engineering. London, UK: Elsevier Academic Press.

Shiller, R. J. (2003). The New Financial Order: Risk in the 21st Century. Princeton, NJ: Princeton University Press.

Strang, G. (1980).Linear Algebra and Its Applications. Second Ed. New York, NY: Harcourt Brace Jovanovich.