BRUCE COLLINS, PhD

Professor of Finance, Western Connecticut State University

FRANK J. FABOZZI, PhD, CFA, CPA

Professor in the Practice of Finance, Yale School of Management

Abstract: The development of the OTC equity derivatives market offers investors investment opportunities that are simply not available in the listed market or cash market. The international banking community has created a marketplace that has improved the efficiency of investing. Serious investors can no longer ignore the value of using OTC derivative products as a major part of their overall investment strategy. It is incumbent on plan sponsors, money managers, insurance companies, mutual funds, and corporations to consider the use of equity derivatives in achieving their investment objectives. The OTC equity derivatives market can be divided into three main components: OTC options and warrants, equity-linked debt instruments, and equity swaps. OTC equity options are customized option contracts that can be applied to any equity index, basket of stocks, or an individual stock. Equity derivatives have a variety of applications to investment management. Among the considerations for equity portfolio management are ways to take advantage of promising returns through the reallocation of funds within the portfolio. This portfolio rebalancing might include sector rotation, international diversification, style rotation, or return enhancement. These strategies mostly focus on stock selection in some way.

Keywords: OTC options, barrier options, compound options, knock-in options, knock-out options, equity swap, equity-linked debt, rainbow option, overperformance option, lookback option, quanto option, chooser option, Asian option, average option, basket option, binary option

An equity derivative can be delivered on a stand-alone basis or as part of a structured product. Structured products involve packaging standard or exotic options, equity swaps, or equity-linked debt into a single product in any combination to meet the risk/return objectives of the investor and may represent an alternative to the cash market even when cash instruments are available. The purpose of this chapter is to provide an overview of over-the-counter (OTC) equity derivatives.

The three basic components of OTC equity derivatives are OTC options and OTC warrants, equity swaps, and equity-linked debt. These components offer an array of product structures that can assist investors in developing and implementing investment strategies that respond to a changing financial world. The rapidly changing investment climate has fundamentally changed investor attitudes toward the use of derivative products. It is no longer a question of what can an investor gain from the use of OTC derivatives, but how much is sacrificed by avoiding this marketplace. OTC derivatives can assist the investor with cost minimization, diversification, hedging, asset allocation, and risk management. In this chapter we examine the product fundamentals across each category of OTC equity derivatives.

Table 15.1. OTC Equity Derivative Applications

Derivative Structure | Application | Benefit |

|---|---|---|

OTC options | Risk management Return enhancement Equity investment Single stock Stock portfolio Sector rotation Traditional option strategies Currency hedged investment | Customization Cost reduction Leverage Accessibility |

Equity swap | Asset allocation Diversification Accessing foreign markets Index fund alternative Currency hedged investment | Cost reduction Leverage Customization Simplicity of deal |

Equity-linked | Risk management | Customization |

Debt | Accessing foreign markets Equity investment Single stock Stock portfolio | Leverage Debt instrument |

Table 15.1 summarizes various OTC equity derivative structures, their use, and their benefits. The benefits of using derivatives range from cost reduction to market access. There are several applications within each derivative category listed in the table. OTC structures can be devised to aid almost any style of equity management. OTC options can be used to buy or sell securities with lower market impact costs. All three OTC equity derivative structures provide a means for risk management. The benefits are not restricted to one investor group. Money managers and pension funds can utilize these derivatives as an integral part of their strategic and tactical investment plans. Every investment strategy has a derivatives application.

Let's take a quick look at the landscape of the equity investment world in order to make the connection between OTC equity derivative products and equity investments. There are two interrelated issues that all investment managers must address—risk and return. Applications of OTC derivatives can emphasize return enhancement or risk management issues. For example, a zero-cost collar structure in the OTC market can address the issue of hedging market risk by selling off a piece of the upside potential of the investment. A barrier option can isolate the precise conditions that the investor believes are most likely to occur without the need to buy all possible outcomes. In both cases, the manager is focusing on risk management.

However, an OTC structure such as an equity swap may be designed to take advantage of higher expected returns in a foreign market. In either application, one cannot separate return from risk, but we can separate the choice of an asset within an asset class from managing the market risk associated with the asset class itself. Thus, we can view equity investment as part of a strategic asset allocation strategy and utilize, when necessary, OTC structures to manage the asset allocation exposure to equities.

Another way to explore equity investments is to separate passive from active management. Passive management via indexing involves the construction of a portfolio of securities designed to exactly replicate the returns and risk profile of an established index. No attempt is made to time the market in order to enhance returns. In contrast, active management is based on the premise that managers with superior knowledge can add value to realized risk-adjusted returns above a corresponding passive strategy. Active management takes on many forms and in some sense can be linked through the methods of implementation. For example, an active strategy based on value involves the purchase of an equity portfolio of stocks that meet a certain fundamental criteria such as a high earnings-to-price ratio. The OTC market offers value managers a means of risk management and strategy implementation that extends beyond the domestic market. The same holds true for growth-oriented active management, or some other active approach. The point of linkage is in risk management and extending the boundaries of the selection universe. Regardless of a manager's equity style, their common denominators can be addressed in the OTC market.

OTC options can be classified as first-generation and second-generation options. The latter are called exotic options. We describe each type of OTC option below.

The basic type of first-generation OTC options either relaxed or extended the standardized structure of an existing listed option or created an option on stocks, stock baskets, or stock indexes without listed options or futures. Thus, OTC options were first used to modify one or more of the features of listed options: the strike price, maturity, size, exercise type (American or European), and delivery mechanism. The terms were tailored to the specific needs of the investor. For example, the strike price can be any level, the maturity date at any time, the contract of any size, the exercise type American or European, the underlying can be a stock, a stock portfolio, or an equity index or a foreign equity index, and the settlement can be physical, in cash or a combination. An example of how OTC options can differ from listed options is exemplified by an Asian option. Listed options are either European or American in structure relating to the timing of exercise. Flex options are listed options that go beyond standard European or American styles. One example is to provide a capped structure. Asian options are options with a payout that is dependent on the average price of the spot price over the life of the option. Due to the averaging process involved, the volatility of the spot price is reduced. Thus, Asian options are cheaper than similar European or American options.

The first generation of OTC options offered flexible solutions to investment situations that listed options did not. For example, hedging strategies using the OTC market allow the investor to achieve customized total risk protection for a specific time horizon. The first generation of OTC options allow investors to fine-tune their traditional equity investment strategies through customizing strike prices, and maturities, and choosing any underlying equity security or portfolio of securities. Investors could now improve the management of risk through customized hedging strategies or enhance returns through customized buy writes. In addition, investors could invest in foreign stocks without the need to own them, profit from an industry downturn without the need to short stocks, or implement an intermediate asset allocation strategy through the purchase of a warrant.

The second generation of OTC equity options includes a set of products that have more complex payoff characteristics than standard American or European call and put options. These second-generation options are sometimes referred to as "exotic" options and are essentially options with specific rules that govern the payoff. Exotic option structures can be created on a stand-alone basis or as part of a broader financing package such as an attachment to a bond issue.

Some OTC option structures are path dependent, which means that the value of the option to some extent depends on the price pattern of the underlying asset over the life of the option. In fact, the survival of some options, such as barrier options, depends on this price pattern. Other examples of path-dependent options include Asian options, lookback options, and reset options. Another group of OTC option structures has properties similar to step functions. They have fixed singular payoffs when a particular condition is met. Examples of this include digital or binary options and contingent options. A third group of options is classified as multivariate because the payoff is related to more than one underlying asset. Examples of this group include a general category of rainbow options such as spread options and basket options.

Competitive market makers are now prepared to offer investors a broad range of derivative products that satisfy the specific requirements of investors. The fastest growing portion of this market pertaining to equities involves products with option-like characteristics on major stock indexes or stock portfolios. It is derived from investor demand for long-dated European options and for options with more complex option structures. The real attractiveness of this market is that there is virtually no limit to the types of payouts.

In this section we review a few selective OTC product structures that can be used as management tools for traditional equity investment strategies. Table 15.2 provides a partial listing of exotic options together with a brief description, an accompanying equity investment strategy application, and a comment on pricing. For an extensive discussion of exotic option products see, Nelken (1996) and Francis, Toy, and Whittaker (1995). We provide a basic description to accompany Table 15.2. The list of option structures is hardly exhaustive and is intended only to provide an introduction to some of the more common structures.

Table 15.2. Description of Some Basic Exotic Options

Option Structure | Description | Use | Pricing Comment |

|---|---|---|---|

Knockout call | One of a class of barrier options Option is canceled if the spot price violates barrier target price | Overwriting | Less expensive than standard call option |

Knockout put | One of a class of barrier options Option is canceled if the spot price goes above barrier target | Hedging | Less expensive than standard call option |

Compound option | Option on an option, call on a put Gives owner the option: to buy the put | Hedging Speculating | Less expensive than standard call option |

Spread option | Payout depends on the difference in performance between two assets | Asset allocation | Large risk premium due to correlation |

Lookback option | Option that gives the right to holder to buy or sell underlying at best price attained over the life of the option | Equity exposure to volatile sectors | More expensive than standard options Market timing |

Quanto option | Quantity-adjusted option Payout depends on underlying price and size in proportion to price | Access to foreign markets with currency hedge. Pricing depends on correlation of exchange rate and spot price | |

Chooser option | Holder must choose to set the option as a call or put at some specific time | Similar to straddle | Less expensive than straddle |

Asian option | Payout depends on average price of the underlying over a specified time period | Allows participation on average return | Less expensive than standard options Liability management |

Basket option | Similar to index options, option written on basket of stocks | Hedging custom equity portfolios | Less expensive than portfolio of options |

Binary option | Cash or nothing | Market timing Asset or nothing | Less expensive than standard option. |

Barrier Options

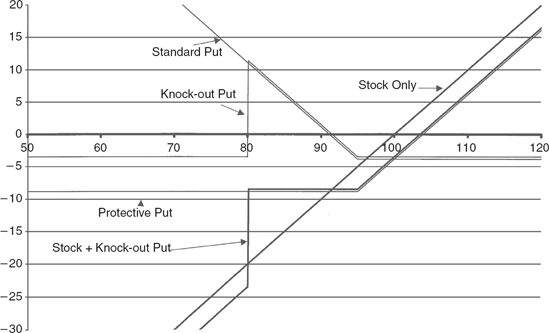

Barrier options are path dependent options whose value and survival depends on the path or price pattern of the underlying asset over the life of the option. Moreover, the survival of the option is dependent on whether a "barrier" or predetermined price is crossed by the price of the underlying asset. Knock-out and knock-in options are examples of barrier options. Knock-out options go out of existence or do not survive when the barrier price is reached or exceeded. Knock-in options, however, come into existence when a barrier is reached or exceeded. The option can be a call or a put and the barrier can be below or above the current underlying asset value. In practice, when a knockout option is terminated, a rebate is given to the holder of the option. Conversely, if a knock-in option comes into existence, a rebate is paid to the option writer. The options are priced assuming the rebates are paid at expiration or when the barrier is reached. Barrier options can be structured as European, American or Bermudan with regard to when they may be exercised. A Bermudan style option only allows the holder to exercise at specific, discrete times over the life of the option. Thus, a Bermudan option is somewhere between a European and an American. The difference in exercise style can have a dramatic impact on pricing.

Figure 15.1 is payout diagram that compares a standard protective put strategy with one that uses a knock-out put. The knock-out put terminates at a price of 80 and offers no rebate. The consequences are obvious from the exhibit. As long as the barrier is not breached, the strategy behaves similar to a protective put. The savings makes sense as long the investor is satisfied with the downside risk.

Compound Options

A compound option is an option written against another option. In other words, the underlying asset of a compound option is an option itself. There are 16 different types of compound options based on the exercise provisions of both the option and the underlying option and whether each is a call or a put. Thus, a call on a put would allow the holder of the call option to purchase a put option. The call could be a European type and the underlying put could be an American type. The pricing of compound options depends on the exercise style of both options and is less expensive than standard options.

Compound options are an alternative way of paying a premium upfront for the right to purchase an option at a later date should the need arise. Often market timing strategies are contingent on new information that enters the market. This could be Federal Reserve policy changes, earnings information or other events that influence financial asset prices. Investors who follow market trends may be engaged in a decision-making process to determine market exposure. The compound option provides an additional layer of choices for the investor in exchange for a premium. Once the decision is made to reduce market exposure, the investor can exercise the compound option or buy a standard option meeting their needs.

Rainbow Options

Overperformance options are rarely used despite their apparent attractiveness. The reason is the price is dependent on the correlation between the two assets, which is quite volatile over time. This makes hedging very difficult for market makers. The most common rainbow option is the option to exchange one asset for another, which is another name for a spread option or an overperformance option.

These options are structured to yield a payoff that depends on the relative performance of one asset versus another. An at-the-money call structure would pay off if there is a positive return differential between the two assets. For example, a call spread option on the relative returns of two stocks, A and B, would pay off if the returns to stock A were sufficiently above the returns to stock B over the investment horizon to pay for the cost of the option. The intrinsic value of the option is the difference between the returns since inception of the contract. The usefulness of this contract is that it can pay off even when equity prices are declining.

Lookback Options

A lookback option is one that allows the holder to buy or sell the underlying asset at the most favorable price attained over the life of the contract. This is the price that maximizes the value of the option at expiration. For lookback call options with fixed strike prices, this means using the highest price over that time and for a put option it means using the lowest price. For lookback options with floating strike prices, which are the most common, the opposite holds true.

Lookbacks can be expensive, so it is important to use them appropriately. They can be relatively attractive during periods of high volatility, but not in periods of persistent price appreciation. Lookbacks are preferred to standard options when the price differential between the initial stock price and the lowest (highest) price expected over the life of the option exceeds the difference between the lookback option premium and the premium on a standard option.

Quanto Options

"Quanto" is a term applied to option contracts that are "quantity adjusted" for the size of the exposure. This means that the payoff of a quanto option depends on the price of the underlying asset just as an ordinary option does, but it also depends on the size of the exposure as a function of the price. Most applications using quanto derivatives involve the purchase or sale of an asset in a currency different from the investor's domestic currency. The payoff is priced in terms of one currency, but made in terms of another. Consequently, the quanto option is automatically hedged for currency risk. Thus, for investors who want foreign market exposure without currency risk, a quanto put option is one alternative.

Chooser Options

A chooser option is also called an as-you-like-it option or a pay-now-choose-later option. It is initiated as neither a call nor a put but contains a provision that allows the holder to designate within some prescribed period whether the option will become a call or a put. There are two important types of chooser options: simple chooser and complex chooser. In the case of a simple chooser structure, the call and put alternatives have the same strike price and time to expiration. This is not the case for complex choosers, which can have a call and put alternatives that vary in both strike price and expiration.

Asian Options

Asian options are path-dependent options with a payout based on an average price. They are also known as average options. The payout for this type of option is based on the difference between two prices where one is based on the average price of the underlying asset for a set of dates over a prescribed period of time. Either the final spot price or the strike price is replaced by the average price of the underlying. Consequently, Asian options are priced at a discount to otherwise similar standard options and can be used as a way to reduce the cost of an option strategy.

Table 15.3 shows three different paths that both result in a final price of 36. The profit for the European put is 47.5 −36 −0.75 is 10.75, which offsets the 14 loss in the stock position. This is a typical protective put. The Asian option profits are path dependent. Path 2 results in no offsetting gain at all while path 1 provides some protection. The standard put option will always do better in down markets, but in up markets and some volatile market, such as that given by path 3, will not perform as well.

Basket Options

A basket option is an option structured against a portfolio or basket of assets, which may include a group of stocks or may include multiple asset classes. For equity baskets, the stocks are selected on the basis of a criterion such as industry group, risk characteristic or other factor that represents the investor's objective. This is comparable to an index option where the price of the option on an equity index is less than the average price of the options on each individual stock that makes up the index. Basket options are particularly appropriate for investors with equity portfolios that do no resemble the indexes that underlie listed index option contracts. These options are suitable for an investor wishing to use options with an underlying asset that exactly reflects their current portfolio holdings.

Table 15.3. Alternative Price Paths: Average Option Example

Observation | Path1 | Path2 | Path3 |

|---|---|---|---|

1 | 50 | 50 | 50 |

2 | 48 | 48 | 45 |

3 | 46 | 51 | 40 |

4 | 45 | 52 | 38 |

5 | 44 | 53 | 36 |

6 | 42 | 51 | 42 |

7 | 41 | 50 | 44 |

8 | 40 | 52 | 45 |

9 | 39 | 51 | 46 |

10 | 38 | 50 | 47 |

11 | 37 | 49 | 48 |

12 | 36 | 36 | 49 |

Average Price | 42.16667 | 49.41667 | 44.16667 |

Binary Options

Binary options make an inherent gamble that pays off if the price of the underlying asset is above or below a particular price at expiration of the option. Binary options are like gambles that pay something when you win and nothing when you lose. The payment can be cash or the asset or nothing. Binary options are also called digital options or all-or-nothing options or cash-or-nothing options. The solution to a cash-or-nothing call option is the present value of the fixed payout times the probability of the stock price ending above the strike price. Binary options can be structured to pay out only if the spot price is higher than the strike price at expiration or if the spot price exceeds the strike price at any time during the life of the option. The size of the move is irrelevant because the payout is all or nothing.

Before an investor decides to use exotic options, it is important to understand the impact that a specific exotic structure will have on the risk/reward profile of the current investment and the cost of implementing the strategy. For example, a lookback option that guarantees the optimal exercise value of the option seems very attractive. However, due to the expense of such an option, the investor may not be better off than if she had purchased the underlying security. Thus, cost becomes an important consideration in evaluating the impact of using exotics.

In order to accomplish this, investors need to understand the nature of the exotic derivative in question, including the pricing dynamics, the risks, and the expected benefits. Moreover, a complete understanding of what could go wrong is necessary including the potential costs, the tax implications, and the impact on the performance of the investor's portfolio. Consider, for example, a situation where the investor chooses a put option with a barrier structure that is designed to knock out at some level above the current price. If the barrier is hit suddenly and the put option is "knocked out," the risk is that the market reverses just as suddenly leaving the investor unprotected. Therefore, it is crucial that the investor understand that the cost saving of a barrier option compared to a standard put option has a risk component.

As shown in Table 15.3 there are several traditional equity investment strategies that can be facilitated using second generation options. These include hedging, overwrites, asset allocation, sector rotation, and style management exposure. Also as noted in the description in the table, exotic structures are often, but not always, less expensive than standard option solutions.

Despite the apparent applications, the use of exotic options brings a new element into the portfolio management process. Therefore, the use of exotics ought to be carefully considered and should provide a degree of precision to satisfy the investment objective that can only be achieved with an OTC exotic structure. Investment objectives that can be met with equal efficiency using methods that don't involve options need not require the use of exotic options. Nonetheless, OTC options do provide investors with opportunities to fine-tune their risk/reward profiles by providing flexible product structures that meet very specific investor requirements.

Options have risk management, returns management, cost management, and regulatory management applications. The addition of exotics can only add to these applications. We can sum this up by saying that the value of these products is the means they provide in meeting objectives with greater flexibility and efficiency. However, it must be emphasized that exotic structures are not appropriate in all situations. On the one hand, there are investors who are eager to use the latest derivative product whether they need to or not; on the other hand, there are investors who fear derivatives and will not use them regardless of whether it would facilitate meeting their financial objectives. It is crucial to evaluate the investor's investment objectives in terms of risk and return and how these objectives can be efficiently met. When risk management needs can be met using listed markets, it may be prudent to do so. However, for investors with specific needs that cannot be met by the listed market, a derivatives process ought to be developed and a set of criteria established that can be used as guidelines for determining whether or not an exotic structure makes sense. A partial list of conditions that investors should consider before using derivatives, particularly ones with complex rules governing the payoff is provided below:

Complete understanding of investor objectives.

Complete evaluation of current risk/reward profile.

Analysis of current portfolio and targeted portfolio.

Assessment of all alternative methods to meet objectives.

Complete understanding of all financial products under consideration.

Identify all risks associated with any derivative security.

Develop worse case scenario analysis and a protocol for responding.

Incorporate a complete strategy into the derivative.

Consider tax and accounting consequences.

Reevaluate procedure and explain it to all parties.

Conduct a cost/benefit analysis.

The first step is to review the investor's objectives, their attitude toward risk and analyze the risk/return profile of the current portfolio and the targeted or benchmark portfolio. Once this is accomplished, then all possible alternative ways of meeting the objective must be explored in order to ascertain whether or not a solution using options is required. For now, it must be clear that the investor must either possess the knowledge and understanding of all the products and markets under consideration or have access to an expert who does. This includes understanding all aspects of the option and most importantly the risks.

Once the decision is made to use options, then the steps that follow involve identifying and fully considering the proposed option transaction. This includes an intimate understanding of the impact the transactions will have on the current portfolio and what could go wrong. Prior to a transaction involving an exotic structure, it is crucial to understand what can go wrong and what are the risks. Are you buying a risk or selling a risk, and is this the risk you want, one consistent with your tolerance for risk and desire for return? Once this is fully understood, even if the investor finds a means of implementing an investment strategy that uses derivatives in the listed market, it may still make sense to examine the OTC market. There are situations where dealers can more aggressively price an OTC product that produces the same risk profile as a portfolio of listed products.

The question of how issuers and dealers can offer OTC exotic products with complex payout structures at a superior price compared to collection of listed products can be explained by at least three factors. These include the need for a very specific risk exposure, the existence of market inefficiencies, and more effective delivery mechanisms. Market inefficiencies can arise when there are fewer payouts than states of the world. These inefficiencies lead to higher costs in the listed market, which reflect greater risks to the market maker.

In the final analysis, investors who are entertaining the possibility of using exotic option structures ought to engage in a serious effort to educate themselves and surround themselves with experts in the field. All alternatives must then be considered and finally a choice must be made to use exotics on the basis of benefits versus costs and the potential for limiting unfavorable outcomes or disaster.

Equity-linked debt (ELD) investments are typically privately placed debt instruments. They differ from conventional debt instruments because the principal, coupon payment, or both are linked to the performance of an established equity index, a portfolio of stocks, or an individual stock. Consistent with other OTC equity derivative securities, equity-linked products have extremely flexible structures. For example, the equity component of the product can assume the characteristics of a call or a put or some combination. The payouts can be more complex mixing exotic-type option payouts with a bond.

In addition to providing flexible structures, equity-linked products also offer the investor the potential for higher returns than conventional debt instruments of similar credit risk. Other characteristics include: more volatile cash flows, the principal guaranteed by issuers with investment grade credit, and the avoidance of certain regulatory restrictions that prevent investors from entering into futures contracts, options, or swap agreements. For example, some pension funds are restricted from using derivatives. ELNs are recorded as a debt instrument and circumvent the restriction. Equity-linked products are typically longer-term investments and therefore have limited liquidity.

ELD investments are also referred to as equity-linked notes. Examples of these are equity participation notes (EPNs, offered by Merrill Lynch), stock upside notes (SUNs, offered by Merrill Lynch), structured upside participating equity receipt (SUPER), and synthetic high-income equity-linked security (SHIELDS). Equity-linked notes are issued by banks, corporations, and government sponsored enterprises, and have maturities ranging from 1 year to 10 years. The coupon can be fixed or floating, linked to an equity index, a portfolio of stocks, or a single stock and denominated in any currency. The equity-linked payment is typically equal to 100% of the equity appreciation, and redemption at maturity is the par value of the bond plus the equity appreciation. Equity participation is actually flexible and changes depending on whether the ELD instrument includes a coupon payment.

The conventional ELD instrument is simply a portfolio consisting of a zero-coupon bond and an index call option. This structure can be extended to include a put or an exotic option. The cash flows associated with an ELD structure are as follows. At issuance, the investor purchases the note, which represents the initial cash flow. Periodic cash flows are derived exclusively from the performance of the linked equity index. For example, if the index appreciated 10% for the year and equity participation is 100%, then assuming that the notional amount is $1 million, the investor would receive $100,000 as a periodic cash flow. The final cash flow includes the return of principal and the final equity payment.

Often, however, cash flows are subject to a cap, which limits the upside participation. SUNs, for example, provide 100% of principal at maturity and pay an annual coupon based on 133% of the year-over-year appreciation in the S&P 500 index subject to a cap of 10%. Thus, the maximum appreciation is 13.3% per annum. If an investor believes the S&P 500 will appreciate by more, this not the appropriate investment vehicle.

The use of an ELD is particularly attractive to domestic insurance companies subject to risk-based capital guidelines, which mandate higher capital requirements for investing in equity than for debt. ELDs are carried as debt, but have their performance linked to equity. Thus, insurance companies can maintain the capital requirements associated with debt instruments and still obtain equity market exposure. Pension funds also can benefit by using ELDs to gain access to foreign equity markets. Direct foreign equity investments subject pension funds to withholding taxes. The use of ELD structures, where the equity component is a foreign index, allows pension funds to avoid withholding taxes. The note has the same structure flexibility as conventional ELD instruments and can also include a currency hedge.

An example of such an equity-linked note is one that combines a zero-coupon bond and an at-the-money call option on the FTSE-100 Index. The redemption value of the note is the higher of par value or the product of par value times the ratio of the value of the FTSE-100 Index at maturity and its value when the note is purchased. This equity-linked note creates a debt instrument with payments based on the returns to the FTSE-100 Index, while eliminating all unwanted risks and costs associated with holding U.K. equities.

As in the case of OTC options, ELD structures are extremely flexible. The investor can decide upon the amount of equity participation, whether to include a coupon or not, whether to target levels of equity appreciation over the life of the product when the target is realized, or whether to create a synthetic convertible bond.

Equity swaps are similar in concept to interest rate or currency swaps. They are contractual agreements between two counterparties which provide for the periodic exchange of a schedule of cash flows over a specified time period where at least one of the two payments is linked to the performance of an equity index, a basket of stocks, or a single stock. Like options and futures, equity swaps are substitutes for a direct investment in equities. In a standard or plain vanilla equity swap one counterparty agrees to pay the other the total return to an equity index in exchange for receiving either the total return of another asset or a fixed or floating interest rate. All payments are based on a fixed notional amount and payments are made over a fixed time period.

Equity swap structures are very flexible with maturities ranging from a few months to 10 years. The returns of virtually any asset can be swapped for another without incurring the costs associated with a transaction in the cash market. Payment schedules can be denominated in any currency irrespective of the equity asset and payments can be exchanged monthly, quarterly, annually, or at maturity. The equity asset can be any equity index or portfolio of stocks, and denominated in any currency, hedged or unhedged.

Variations of the plain vanilla equity swap include: international equity swaps where the equity return is linked to an international equity index; currency-hedged swaps where the swap is structured to eliminate currency risk; and call swaps where the equity payment is paid only if the equity index appreciates (depreciation will not result in a payment from the counterparty receiving the equity return to the other counterparty because of call protection). In fact, the first equity swap was designed as a means to invest in foreign securities while avoiding the tax consequences of a direct investment.

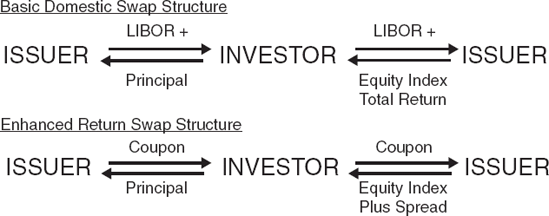

A basic swap structure is illustrated in Figure 15.2. In this case, the investor owns a short-term credit instrument that yields the London Interbank Offered Rate (LIBOR) plus a spread. (Note the difference in the quotation convention for equity swaps compared to interest rate swaps. For the latter, the floating rate is quoted flat while the fixed-rate side is quoted as the rate on a comparable maturity Treasury plus the swap spread.) The investor then enters into a swap to exchange LIBOR plus the spread for the total return to an equity index. The counterparty pays the total return to the index in exchange for LIBOR plus a spread. Assuming the equity index is the Nikkei 225, a U.S. investor could swap dollar-denominated LIBOR plus a spread for cash flows from the total return to the Nikkei denominated in yen or U.S. dollars. The index could be any foreign or domestic equity index. A swap could also be structured to generate superior returns if the financing instrument in the swap yields a higher return than LIBOR.

Equity swaps have a wide variety of applications including asset allocation, accessing international markets, enhancing equity returns, hedging equity exposure, and synthetically shorting stocks.

An example of an equity swap is a one-year agreement where the counterparty agrees to pay the investor the total return to the S&P 500 Index in exchange for dollar-denominated LIBOR on a quarterly basis. The investor would pay LIBOR plus a spread × 91/360 × notional amount. This type of equity swap is the economic equivalent of financing a long position in the S&P 500 Index at a spread to LIBOR. The advantages of using the swap are no transaction costs, no sales or dividend withholding tax, and no tracking error or basis risk versus the index.

The basic mechanics of equity swaps are the same regardless of the structure. However, the rules governing the exchange of payments may differ. For example, a U.S. investor wanting to diversify internationally can enter into a swap and, depending on the investment objective, exchange payments on a currency-hedged basis. If the investment objective is to reduce U.S. equity exposure and increase Japanese equity exposure, for example, a swap could be structured to exchange the total returns to the S&P 500 Index for the total returns to the Nikkei 225 Index. If, however, the investment objective is to gain access to the Japanese equity market, a swap can be structured to exchange LIBOR plus a spread for the total returns to the Nikkei 225 Index. This is an example of diversifying internationally and the cash flows can be denominated in either yen or dollars. The advantages of entering into an equity swap to obtain international diversification are that the investor exposure is devoid of tracking error, and the investor incurs no sales tax, custodial fees, withholding fees, or market impact associated with entering and exiting a market. This swap is the economic equivalent of being long the Nikkei 225 financed at a spread to LIBOR at a fixed exchange rate.

There are numerous applications of equity swaps, but all assume the basic structure outlined above. Investors can virtually swap any financial asset for the total returns to an equity index, a portfolio of stocks, or a single stock. Market makers are prepared to create structures that allow an investor to exchange the returns of any two assets. The schedule of cash flows exchanged is a function of the assets. For example, an investor wanting to outperform an equity benchmark may be able to accomplish this by purchasing a particular bond and swapping the cash flows for the S&P 500 total return minus a spread.

Equity swaps are a useful means of implementing an asset allocation strategy. One example is an asset swap of the S&P 500 total returns for the total returns to the DAX index. The investor can reduce U.S. equity exposure and increase German equity exposure through an equity swap, thereby avoiding the costs associated with cash market transactions.

OTC options are privately negotiated contractual agreements between an investor and an issuing dealer. The structure of the option is completely flexible in terms of strike price, expiration, and payout features. OTC warrants are long-term options on equity indexes, basket of stocks, or an individual stock and have the same flexible structure capability as OTC options. Equity-linked debt is a debt instrument with principal or coupon payments linked to the performance of an established equity index, a basket of stocks, or a single stock. Equity swaps are similar in structure to interest rate or currency swaps. They are contractual agreements between two counterparties providing for the periodic exchange of a schedule of cash flows over a specified time period where at least one of the two payments is linked to the performance of an equity index, a basket of stocks, or a single stock.

OTC equity derivatives can provide investors with a means of lowering transaction costs, including commissions and market impact costs. In addition, OTC equity derivatives may be useful for tax management purposes by delaying capital gains. From the standpoint of pension funds, equity derivatives may provide a vehicle for reducing management fees and custodian fees. There are also a variety of legal and regulatory barriers that can be overcome using OTC equity derivatives. These features add to the payoff possibilities available from structured products. Investors can hedge any risk or assume any risk in ways that are only limited by their ability to characterize their desired financial objectives.

Boyle, P., and Boyle, F. (2001). Derivatives: The Tools That Changed Finance. London: Risk Books.

Chance, D. M. (2004). An Introduction to Derivatives, 6th edition. Mason, OH: Thomson South-Western.

Collins, B., and Fabozzi, F. J. (1999). Derivatives and Equity Portfolio Management. Hoboken, NJ: John Wiley & Sons.

Dubofsky, D. A., and Miller, T. W. (2003). Derivatives: Valuation and Risk Management. New York: Oxford University Press.

Francis, J. C., Toy, W., and Whittaker, G. (1995). The Handbook of Equity Derivatives. Burr Ridge, IL: Irwin Professional Publishing.

Gastineau, G., and Kritzman, M. (1997). Dictionary of Financial Risk Management. Hoboken, NJ: John Wiley & Sons.

Hull, J. (2006). Options, Futures, and Other Derivative Securities. Upper Saddle River, NJ: Prentice Hall.

Kat, H. (2001). Structured Equity Derivatives. Chichester, England: John Wiley & Sons.

McLaughlin, R. M. (1999). Over-the-Counter Derivative Products. New York: McGraw-Hill.

Nelken, I. (ed.) (1996). The Handbook of Exotic Options. Burr Ridge, IL: Irwin Professional Publishing.

Rubinstein, M. (1991). Exotic options. Working paper, March.