FRANK J. FABOZZI, PhD, CFA, CPA

Professor in the Practice of Finance, Yale School of Management

STEVEN V. MANN, PhD

Professor of Finance, Moore School of Business, University of South Carolina

FILIPPO STEFANINI

Deputy Chief Investment Officer, Aletti Gestielle Alternative SGR Professor of Risk Management, Faculty of Engineering at Bergamo University in Italy

Abstract: Corporations finance themselves by selling claims to the expected future cash flows generated by their assets. The two basic claims issued are debt claims in the form of bonds and equity claims in the form of common stocks. Between these two endpoints, there exists a continuum of securities that possess features of both bonds and stocks. Among the most prominent of these hybrid securities is convertible bonds. A convertible bond is a combination of an option-free bond and the option to convert the bond into a given number of shares of the issuer's common stock. Convertible bonds may also be callable or putable or both. Depending on the performance of the underlying company, a convertible bond may behave more like a common stock or more like an option-free bond.

Keywords: conversion ratio, conversion premium, conversion price, hard put, soft put, conversion value, straight value, premium payback period, premium over straight value, fixed income equivalent, common stock equivalent, mandatory convertible, reverse convertible, convertible bond arbitrage

A convertible bond is a security that gives the investor the option to convert into a specified number of shares of the issuer's common stock. Convertible bonds issued today typically possess more than one embedded option in that they can be callable and putable. Accordingly, valuing convertible bonds is more challenging because the bond's value will depend on: (1) how interest rate changes impact the bond's expected future cash flows via call and/or put options, (2) how creditworthiness of the underlying company impacts expected future cash flows, (3) how the stock price changes impact the value of the conversion feature, and (4) how volatile the stock price is.

In its most basic form, there are two equivalent ways to describe a convertible bond. First, a convertible bond represents the combination of an option-free bond and call option on the common stock. However, unlike the exercise price of a call option, which is fixed, the value of the bond is surrendered to obtain a predetermined number of shares of stock. Second, a convertible bond is a combination of common stock and a put option, which gives the bondholder the right to sell the stock back to the issuer with an exercise price equal to the market value of the convertible. If the investor chooses not to convert, she effectively exercises the put and thereby keeps receiving the bond's cash flows.

Closely related to a convertible bond is an exchangeable bond. An exchangeable bond gives the bondholder the right, but not the obligation, to exchange the bond for the common stock of a firm other than the security issuer. For example, in April 2007, UBS AG issued 6% six-month notes that were exchangeable into a fixed number of shares of Honda Motor Corporation. For the remainder of the chapter, we will use the term "convertible bond" to refer to both convertible and exchangeable bonds.

In this chapter, we describe the defining characteristics of convertible bonds and provide a sketch of the convertible bond market. The traditional approach to analyzing convertibles is examined. Variants of the traditional convertible bond structure are introduced. Finally, the issue of why convertible bond arbitrage is a popular hedge fund strategy is discussed.

The U.S. convertible bond market is by far the largest convertible bond market. Most U.S. convertible bonds are issued as private placements under Securities and Exchange Commission (SEC) Rule 144A. These issues can be sold to only qualified investors. Conversely, in Japan, the convertible bond market is comprised of a large number of very small domestic issues that are listed and traded on the Tokyo stock exchange.

There are marked differences in the size and creditwor-thiness of issuers of convertible in the United States and Europe. Most European convertible bonds are issued by large corporations with investment-grade credit ratings. In contrast, the majority of U.S. convertible bonds are issued by smaller corporations that are rated below investment grade.

In this section, we will introduce the defining characteristics of a convertible bond using an example. Consider a convertible bond issued by United Auto Group in April 2006. This convertible bond carries a 3.5% coupon rate and the right to convert extends until the maturity date of April 1, 2026. As noted, the conversion provision grants the security holder the right, but not the obligation, to convert the bond into a predetermined number of shares of the issuer's common stock. The predetermined number of shares is called the conversion ratio. This ratio is always adjusted proportionally for stock splits and stock dividends. For the United Auto Group convertible, the conversion ratio is 42.2052 shares. Accordingly, the security holder at a time of her choosing may surrender the $1,000 maturity value bond for 42.2052 shares of United Auto Group common stock.

Armed with the conversion ratio, it is straightforward to determine the price per share the convertible bondholder pays when purchasing the share via the conversion mechanism. This is called the conversion price and is found by dividing the bond's price by the conversion ratio. If the United Auto Group bond is converted, the investor will receive 42.2052 shares of its common stock. Accordingly, at issuance, the shares are purchased at $23.69 per share ($1,000/42.2052). Purchasing the common stock with a convertible security requires that the investor pay a premium over the current share price. Investors accede to this because of the embedded optionality The premium is often measured in percentage terms and is called the conversion premium. When the United Auto Group bonds were issued, the stock price was $18.95 and the conversion price was $23.69, so the initial conversion premium was 25%

Virtually all convertible bonds are callable such that the call feature gives the investor the right to buy the bond back at a given price (that is, the call price) before maturity. The United Auto Group bond has a 5-year call protection period such that the first call date is April 6, 2011, and gives the issuer the option to buy the bonds back before maturity. The call price is 100.

Many convertible bonds also possess a put feature. The put feature gives the bondholder the right but not the obligation to sell the bond back to the issuer at par before the maturity date. The United Auto Group bond is putable at par starting on April 6, 2011, five years after issuance. Put features may be classified as either "hard" or "soft" and differ as to the form of payment to the bondholder when the put is exercised. A hard put requires the convertible security to be redeemed for cash. Conversely, when a soft put is exercised, the issuer is allowed to choose the form of payment, which may be cash, common stock, subordinated debt, or some combination of the three.

The traditional approach to the analysis and valuation of convertible bonds predates models designed to value bonds with embedded options. As such, traditional analysis does not take into consideration the value of any of the convertible bond's embedded options directly.

The traditional approach to the valuation of convertible bonds begins with the determination of two values— conversion and straight. A bond's straight value is found by valuing the bond as if the conversion feature does not exist. The conversion value is the security's value if it converted immediately. Specifically,

At any point before maturity, a convertible bond must be worth at least as much as the greater of the conversion value or the straight value. This is an arbitrage-enforced result. To see this, suppose the conversion value is greater than the straight value and the convertible bond's price is equal to its straight value. To exploit this arbitrage opportunity, an investor would buy the convertible and immediately convert. These actions enable the investor to capture the difference between the conversion value and the straight value less transaction costs. Suppose the opposite is true: The straight value is greater than the conversion value and the bond trades at its conversion value. If this occurs, the investor will be holding a bond that is undervalued relative to an otherwise the same straight bond.

When an investor takes a position in a convertible bond, he or she is buying the upside potential driven by the common stock with the downside protection of the straight bond. Accordingly, investors are willing to pay a premium over the current share price to purchase the common stock using the convertible. The price paid per share if the convertible is purchased and then converted is called the market conversion price or the conversion parity price. The market conversion price is computed as follows:

Analysts view the market conversion price as a "breakeven price" because if the share price rises to this level, it just equals the price at which the investor purchased the shares using the convertible security.

The next phase in our analysis is to recast the premium paid for buying the shares using the convertible as a call option. This is true because the conversion feature allows for upside share price appreciation with a limited downside. To do this, we calculate the market conversion premium per share as follows:

The market conversion premium per share can be viewed as the value of the call option on common stock underlying the convertible. An important difference between the two positions is the downside risk exposure. The downside of a long call position is limited to the price paid for the option. Moreover, the downside risk exposure is the convertible's straight value serves as a floor of the convertible security's value. The floor, unfortunately, is like the floor of an elevator in that it can go up or down. This is true because the straight bond's value is a function of the level of interest rates, credit risk, and the like.

The market conversion premium per share can also be expressed as a percentage of the current share price. Specifically, the market conversion premium ratio is computed as follows:

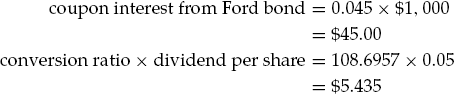

As an illustration, consider a convertible issued by Ford Motor Company in December 2006. The issue pays a 4.5% coupon semiannually and matures in December 2036. This bond has a conversion ratio of 108.6957 shares and the bond's current market value is 1,113.80. The market conversion price is

Accordingly, the investor is paying $10,247 a share for Ford Motor Company common stock. Suppose the current market share price of Ford is $8.01. The market conversion premium per share is computed as follows:

This number tells us that if investors buy Ford common stock via the convertible, they pay a premium of $2.24 a share as opposed to buying the stock at the prevailing market price. Finally, the market conversion premium ratio is computed as follows:

This percentage is interpreted as the investor is paying a premium of 27.93% to purchase the Ford common stock through the convertible.

Assuming that the issuer does not default on its debt, convertible bonds usually generate more in coupon interest than dividend income received from a number of common shares equal to the conversion ratio. This income advantage counterbalances the premium paid for common stock purchased via the convertible bond. When analysts assess relative value, they often compute a measure called the premium payback period (also called the break-even time). The premium payback period measures how long it takes to pay for the market conversion premium per share with the convertible's income advantage. The premium payback period is computed with the following:

where the favorable income differential per share is computed as follows:

The ratio has two parts. The first part (numerator) is the favorable income differential which is simply the coupon interest paid by the convertible less the dividend income forgone by not converting. The second part (denominator) is just the conversion ratio and puts the income advantage on a per share basis. Accordingly, the premium payback period answers the question: How long must one hold the convertible bond with its favorable income differential until the premium per share for buying the common stock via the convertible is recovered? We hasten to add that this measure does not account for future dividend changes or the time value of money.

We will use the Ford Motor Company convertible bond to illustrate this measure. Our first task is to find the favorable income differential per share. We need to calculate the following:

This number tells us it will take approximately 6.2 years for the higher income of the convertible bond versus holding the common stock directly to recover the market conversion premium per share. The preceding ignores any dividend changes and the time value of money.

Traditional convertible analysis erroneously views a convertible bond's straight value as the floor for the bond's value. Following this line of reasoning, the distance between the current market price and the straight value can be viewed as a measure of the investor's downside risk exposure. Formally, the downside risk is measured as a percentage of the straight value (that is, the floor), referred to as the premium over straight value. It is calculated using the following formula:

All else being equal, the greater the premium over the straight value, the greater the investor's exposure to downside risk.

The flaw in this measure is that the straight value is mistakenly viewed as a fixed and an immoveable barrier. The straight value depends on the level of yields and will move inversely to changes in those yields. The "floor" is a moving target.

We illustrate this measure using the Ford Motor Company convertible bond, whose current market value is $1,112.80:

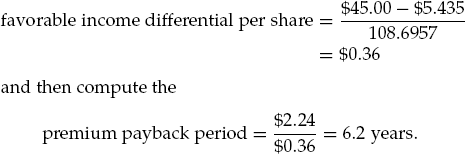

A convertible bond is a hybrid financial instrument that combines elements of a position in a fixed income security and a position in the underlying common stock. The relative importance of each component is driven primarily by the financial performance of the underlying company that is ultimately reflected in the stock price. The relationship between the convertible bond price and the underlying stock price can be described as a continuum (see Figure 29.1). At one end of the continuum, the stock price is relatively low, such that the straight value of the convertible is considerably higher than the conversion value. When this occurs, convertibles have a low sensitivity to the underlying stock price because the conversion option is deep out-of-the-money and will trade like a high-yield straight bond. Convertibles in such circumstances are ierraeafixed-income equivalent or busted convertible. At the opposite end of the continuum, the stock price is relatively high, such that the conversion value is considerably higher than the straight value. The convertible bond will be highly responsive to changes in the stock price and possess a low conversion premium. When this occurs, the convertible bond will trade much like a common stock. The convertible under these conditions is said to be a common stock equivalent. At points in between the two endpoints, the convertible trades like a hybrid security possessing the characteristics of both a bond and a stock.

There are two prominent variants of the traditional convertible bond—mandatory convertibles and reverse convertibles. Each is discussed in turn in this section.

Mandatory convertibles are equity-linked hybrid securities that convert automatically at maturity into shares of the issuer's common stock. This automatic conversion differs from convertible bonds where conversion is optional.

Mandatory convertibles offer higher coupon payments relative to the dividend income from holding the common stock directly. To glean these benefits, investors in mandatory convertibles pay a premium for the shares to be acquired at maturity. Moreover, these securities provide investors with limited upside participation in the underlying common stock. Mandatory convertibles are known by other trade names, including debt exchangeable for common stock (DECS).

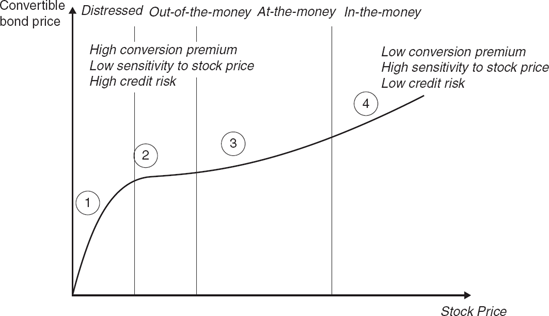

Mandatory convertibles are converted at maturity into a number of shares determined by the underlying share price as presented in Figure 29.2. There are three possible outcomes. First, if the share price at maturity is below the lower exercise price Pi, the investor receives a fixed number of shares. Second, if the share price at maturity falls between the two exercise prices, the investor receives a variable number of shares such that their value remains constant (VN) between the two exercise prices. Third, if the share price at maturity is above the higher exercise price P2, the investor receives a fixed number of shares that is lower than in the first outcome.

As an illustration, Deutsche Telekom AG issued a mandatory convertible on February 24, 2003, through its Dutch financial company Deutsche Telekom International Finance B.V. The amount issued was €2.2885 billion. The bond paid a 6.5% coupon annually and matured on June 1, 2006. Conversion was mandatory at maturity, but investors had the option to convert from July 1, 2003, until April 30, 2006. The lower exercise price was €11.80, and the higher exercise price was €14.632. The minimum/maximum conversion ratios were 3,417.17/ 4,237.29.

One appealing feature of a regular convertible bond is the downside protection of the bond component. If the underlying common stock price performance is anemic and the conversion feature has no value, investors still have the bond. Due to the automatic conversion at expiration, a mandatory convertible has no bond floor and offers no downside protection.

The major difference between a regular convertible and reverse convertible turns on who owns the conversion option. A reverse convertible can be thought of as the combination of a long position in an option-free bond and a short position in a put option. The issuer of the reverse convertible owns the put option and has the right but not the obligation to exercise its option to sell. If the price of the issuer's common stock is below the exercise price at the exercise date, the bondholder receives a fixed number of shares of stock. The investor is obligated in effect to purchase shares above its market value. Conversely, if the stock price is above the exercise price at expiration, the bondholder receives the bond's maturity value.

As explained in Chapter 48 of Volume II, convertibles are ideal securities for arbitrage because the convertible itself, namely, the underlying stock and the associated derivatives, are value expressions of the same company and any discrepancy or mispricing would give rise to arbitrage opportunities for hedge fund managers to exploit. As we have seen, the valuation of convertible bonds is driven by four primary factors: (1) interest rates, (2) credit spreads, (3) stock prices, and (4) volatility of stock prices. Convertible bond arbitrage involves taking a leveraged position (long or short) in the convertible bond to gain exposure to a mispriced factor while simultaneously hedging interest rates and small changes in stock prices. Now, suppose that a hedge fund manager has a view that a convertible bond is undervalued. How would the hedge fund manager take advantage of this view? The natural response is to take a long position in the convertible bond. This strategy is exposed to at least three significant risks. First, the hedge fund manager could be wrong about his/her valuation assessment. Since this is how hedge fund managers add value, this is a risk they are willing to bear.

Second, a long position in the convertible is exposed to adverse movements in stock prices. To neutralize this risk, the hedge fund manager establishes a short position in an appropriate amount of the underlying common stock. The appropriate amount depends on the sensitivity of the convertible bond's value and changes in the underlying stock price. We call this price sensitivity "delta," and it tells us for a $1 change in the conversion value what is the associated change in the convertible bond's value. Suppose that delta is 0.60. This measure tells that for a $1 change in the conversion value, the convertible bond's value changes by approximately $0.60. To hedge the exposure to adverse share price movements, the hedge fund manager would short a number of shares per bond equal to 0.60 multiplied by the conversion ratio. The combined value of the long convertible bond position and the short common stock position should be invariant to small change in the underlying stock price.

The third risk exposure is the adverse movements in interest rates. This risk can be measured, for example, by the effective dollar duration of the convertible position. Effective dollar duration tells us the dollar price change in the value of a bond position given a 100 basis point shift in yield. (For a discussion of effective duration, see Chapter 13 of Volume III.) To hedge this risk, managers take a short position in Treasury securities or a short position in interest rates futures.

The fourth risk exposure is the drop in the stock volatility that can happen in lackluster equity markets. The fifth risk exposure is the lack of liquidity in the market and the consequent widening of bid-ask spreads.

A convertible bond is a security that gives the investor the option to convert into a specified number of shares of the issuer's common stock. In this chapter, we described the basic structure of a convertible bond. The traditional approach to the analysis of convertible bonds was presented. This approach does not attempt to value the options embedded in the convertible directly. Other types of convertibles—mandatory and reversible—are introduced. To the savvy hedge fund manager, convertible bonds represent a "target-rich" environment for finding and exploiting mispriced securities.

Arak, M., and Martin, A. (2005). Convertible bonds: How much equity, how much debt? Financial Analysts Journal 61, 2: 44-50.

Bhattacharya, M. (2005). Convertible securities and their valuation. In F. J. Fabozzi (ed.), The Handbook of Fixed Income Securities (pp. 1393-1442). New York: McGraw-Hill.

Calamos, J. P. (1998). Convertible Securities: The Latest Instruments, Portfolio Strategies, and Valuation Analysis. New York: McGraw-Hill.

Connolly, K. B. (1998). Pricing Convertible Bonds. England: John Wiley & Sons.

de La Grandville, O. (2001). Bond Pricing and Portfolio Analysis, 1st edition. Cambridge, MA: MIT Press.

Dialynas, C. P., and Ritchie, J. C. (2005). Convertible securities and their investment characteristics. In F. J. Fabozzi (ed.), The Handbook of Fixed Income Securities (pp. 1371-1392). New York: McGraw-Hill.

Ho, T., and Pfeffer, D. (1996). Convertible bonds: Model, value attribution, and analytics. Financial Analysts Journal 51,1: 35-44.

Mann, S., Moore, W, and Ramanlal, P. (1999). Timing of convertible debt issues. Journal of Business Research 45, 2:101-105.

Moore, W (2001). Real Options and Option Embedded Securities, 1st edition. Hoboken, NJ: John Wiley & Sons.

Moore, W, and Korkeamaki, T. (2004). Convertible bond design and capital investment: The role of call provisions. Journal of Finance 59,1: 391-405.

Reverre, S. (2001), The Complete Arbitrage Deskbook, 1st edition. New York: McGraw-Hill.

Stefanini, F. (2006). Investment Strategies of Hedge Funds. Chichester, UK: John Wiley & Sons.