FRANK J. FABOZZI, PhD, CFA, CPA

Professor in the Practice of Finance, Yale School of Management

Abstract: Bonds are debt instruments that are issued by a wide-range of entities throughout the world. Unlike the investor in common stock who hopes to share in the good fortunes of a corporation through increased dividends and price appreciation in the stock's price, an investor in a bond has agreed to accept a fixed contractual interest rate. The features that may be included in a bond affect both the performance of a bond when market interest rates change and its risk characteristics. An investor in a bond is exposed to one or more of the following risks: interest rate risk, call and prepayment risk, credit risk, liquidity risk, exchange rate or currency risk, and inflation or purchasing power risk. There are various yield measures that are quoted for bonds: current yield, yield to maturity, yield to call, yield to put, yield to worst, and cash flow yield.

Keywords: bond, global bond market, domestic bond market, foreign bond market, international bond market, offshore bond market, Eurobond market, Eurobonds, maturity, term to maturity, money market instruments, money market, principal, face value, redemption value, maturity value, coupon rate, coupon, step-up notes, zero-coupon bonds, floating-rate securities, fixed-rate bond market, floating-rate bond market, coupon reset date, inverse floaters, reverse floaters, cap, floor, range note, accrued interest, full price, clean price, traded flat, trade date, settlement date, value date, day count conventions, bullet maturity, serial bonds, amortizing securities, sinking fund provision, deferred call, first call date, refunding, first par call date, prepayment, prepayment option, balloon maturity, accelerated sinking fund provision, convertible bond, current yield, yield to maturity, bond-equivalent yield, yield to call, yield to first call, yield to next call, a yield to first par call, yield to refunding, yield to put, yield to worst, cash flow yield, interest rate risk, call risk, prepayment risk, credit risk, default risk, rating agencies, credit spread risk, downgrade risk, liquidity risk, exchange rate risk, currency risk, inflation risk, purchasing power risk

In its simplest form, a bond is a financial obligation of an entity that promises to pay a specified sum of money at specified future dates. The entity that promises to make the payment is called the issuer of the security or the borrower. Some examples of issuers are the U.S. government or a foreign government, a state or local government entity, a domestic or foreign corporation, and a supranational government such as the World Bank. The investor who purchases a bond is said to be the lender or creditor. The promised payments that the issuer agrees to make at the specified dates consist of two components: interest payments and repayment of the amount borrowed.

The purpose of this chapter is to explain the investment features of bonds, the various measures of yield quoted for bonds, and the risks that investors face when investing in bonds.

There are many ways to classify the bond market. One way is in terms of the taxability of the interest at the federal income tax level. In the United States, most securities issued by state and local governments and by entities that they establish, referred to as municipal bonds or municipal securities, are exempt from federal income taxation. While there are reasons why some issuers of municipal bonds will issue taxable bonds, the municipal bond market is generally viewed as the market for tax-exempt securities. As such, the primary attraction to investors is this tax feature.

The largest part of the bond market is the taxable market. There are various ways to describe this sector. Investment banking firms that have developed bond market indexes use various classifications. The most popular indexes are those published by Lehman Brothers and within the group of indexes it publishes, the one followed most closely by investors in the United States is the U.S. Aggregate Index. That index contains the six sectors shown in Table 17.1 along with the percentage of each sector in terms of market value as of July 20, 2007. We'll review each of the sectors later in this chapter.

Another way of classifying bond markets is in terms of the global bond market. One starts by partitioning a given country's bond market into a national bond market and an international bond market. In turn, a country's national bond market can be divided into a domestic bond market and a foreign bond market with the distinction being the domicile of the issuer. The domestic bond market is the market where bond issues of entities domiciled within that country are issued and then traded; the foreign bond market is the market where bond issues of nondomiciled entities of that country are issued and then subsequently traded within the country. Each country has a nickname for foreign bonds. For example, in the United States, "Yankee bonds" are bonds issued by non-U.S. entities and then traded in the U.S. market. In the United Kingdom, foreign bonds are called "bulldog bonds." The international bond market, also referred to as the offshore bond market, is the market where bonds are issued and then traded outside of the country and not regulated by the country.

Table 17.1. Sectors of the Lehman Brothers U.S. Aggregate Index

Sector | Percent of Market Value (as of July 20, 2007) |

|---|---|

Source: Data obtained from Lehman Brothers, Global Relative Value, Fixed Income Research, July 23, 2007. | |

Treasury | 23.49% |

Agency | 10.60 |

Mortgage Pass-through | 37.90 |

Commercial MBS | 4.89 |

Asset-Backed Securities | 1.12 |

Credit | 22.02 |

An important sector of the international bond market is the market for bonds that are underwritten by an international syndicate, issued simultaneously to investors in a number of countries, and issued outside of the jurisdiction of any single country. This market is popularly referred to as the Eurobond market and the bonds are called Eurobonds. Unfortunately, the name is misleading. The currency in which Eurobonds are denominated can be any currency, not just euros. In fact, Eurobonds are classified according to the denomination of the currency (e.g., Eurodollar bonds and Euroyen bonds). Nor are Eurobonds traded in just Europe. Global bonds from the perspective of a country are bonds that are not only traded in that country's foreign bond market but also in the Eurobond market.

While the U.S. bond market is the largest bond market in the world, there are other bond markets in which U.S. investors participate. These are described in Chapters 24, 25, 26 and 31 of Volume I.

The promises of the issuer and the rights of the bondholders are set forth in great detail in the indenture. Bondholders would have great difficulty in determining from time to time whether the issuer was keeping all the promises made in the indenture. This problem is resolved for the most part by bringing in a trustee as a third party to the contract. The indenture is made out to the trustee as a representative of the interests of the bondholders; that is, a trustee acts in a fiduciary capacity for bondholders. A trustee is a bond or trust company with a trust department whose officers are experts in performing the functions of a trustee.

Unlike common stock which has a perpetual life, bonds have a date on which they mature. The number of years over which the issuer has promised to meet the conditions of the obligation is referred to as the term to maturity. The maturity of a bond refers to the date that the debt will cease to exist, at which time the issuer will redeem the bond by paying the amount borrowed. The maturity date of a bond is always identified when describing a bond. For example, a description of a bond might state "due 12/15/2025."

The practice in the bond market is to refer to the "term to maturity" of a bond as simply its "maturity" or "term." Despite sounding like a fixed date in which the bond matures, there are provisions that may be included in the indenture that grants either the issuer or bondholder the right to alter a bond's term to maturity. These provisions, which will be described later in this chapter, include call provisions, put provisions, conversion provisions and accelerated sinking fund provisions.

The maturity of a debt instrument is used for classifying two sectors of the market. Debt instruments with a maturity of 1 year or less are referred to as money market instruments and trade in the money market. What we typically refer to as the "bond market" is debt instruments with a maturity greater than one year. The bond market is then categorized further based on the debt instrument's term to maturity: short-term, intermediate-term, and long-term. The classification is somewhat arbitrary and varies amongst market participants. A common classification is that short-term bonds have a maturity of from 1 to 5 years, intermediate-term bonds have a maturity from 5 to 12 years, and long-term bonds have a maturity that exceeds 12 years.

Typically, the maturity of a bond does not exceed 30 years. There are, of course, exceptions. For example, Walt Disney Company issued 100-year bonds in July 1993 and the Tennessee Valley Authority issued 50-year bonds in December 1993.

The term to maturity of a bond is important for two reasons in addition to indicating the time period over which the bondholder can expect to receive interest payments and the number of years before the principal will be paid in full. The first reason is that the yield on a bond depends on it. At any given point in time, the relationship between the yield and maturity of a bond (called the yield curve) indicates how bondholders are compensated for investing in bonds with different maturities. The second reason is that the price of a bond will fluctuate over its life as interest rates in the market change. The degree of price volatility of a bond is dependent on its maturity. More specifically, all other factors constant, the longer the maturity of a bond, the greater the price volatility resulting from a change in interest rates.

The par value of a bond is the amount that the issuer agrees to repay the bondholder by the maturity date. This amount is also referred to as the principal, face value, redemption value, or maturity value.

Because bonds can have a different par value, the practice is to quote the price of a bond as a percentage of its par value. A value of 100 means 100% of par value. So, for example, if a bond has a par value of $1,000 and is selling for $850, this bond would be said to be selling at 85. If a bond with a par value of $100,000 is selling for $106,000, the bond is said to be selling for 106.

The annual interest rate that the issuer agrees to pay each year is called the coupon rate. The annual amount of the interest payment made to bondholders during the term of the bond is called the coupon and is determined by multiplying the coupon rate by the par value of the bond. For example, a bond with a 6% coupon rate and a par value of $1,000 will pay annual interest of $60.

When describing a bond issue, the coupon rate is indicated along with the maturity date. For example, the expression "5.5s of 2/15/2024" means a bond with a 5.5% coupon rate maturing on 2/15/2024.

For bonds issued in the United States, the usual practice is for the issuer to pay the coupon in two semiannual installments. Mortgage-backed securities and asset-backed securities typically pay interest monthly. For bonds issued in some markets outside the United States, coupon payments are made only once per year.

In addition to indicating the coupon payments that the investor should expect to receive over the term of the bond, the coupon rate also affects the bond's price sensitivity to changes in market interest rates. All other factors constant, the higher the coupon rate, the less the price will change in response to a change in market interest rates.

There are securities that have a coupon rate that increases over time according to a specified schedule. These securities are called step-up notes because the coupon rate "steps up" over time. For example, a 5-year step-up note might have a coupon rate that is 5% for the first two years and 6% for the last three years. Or, the step-up note could call for a 5% coupon rate for the first two years, 5.5% for the third and fourth years, and 6% for the fifth year. When there is only one change (or step up), as in our first example, the issue is referred to as a single step-up note. When there is more than one increase, as in our second example, the issue is referred to as a multiple step-up note.

Not all bonds make periodic coupon payments. Zero-coupon bonds, as the name indicates, do not make periodic coupon payments. Instead, the holder of a zero-coupon bond realizes interest at the maturity date. The aggregate interest earned is the difference between the maturity value and the purchase price. For example, if an investor purchases a zero-coupon bond for 63, the aggregate interest at the maturity date is 37, the difference between the par value (100) and the price paid (63). The reason why certain investors like zero-coupon bonds is that they eliminated one of the risks that we will discuss later, reinvestment risk. The disadvantage of a zero-coupon bond is that the accrued interest earned each year is taxed despite the fact that no actual cash payment is made.

There are issues whose coupon payment is deferred for a specified number of years. That is, there is no coupon payment for the deferred period and then a lump sum payment at some specified date and coupon payments until maturity. These securities are referred to as deferred interest securities.

A coupon-bearing security need not have a fixed interest rate over the term of the bond. These are bonds that have an interest rate that is as variable. These bonds are referred to as floating-rate securities. In fact, another way to classify bond markets is the fixed-rate bond market and the floating-rate bond market. Floating-rate securities appeal to institutional investors such as depository institutions (banks, savings and loan associations, and credit unions) because it provides a better match against their funding costs which are typically floating-rate debt. Typically, the interest rate is adjusted on specific dates, referred to as the coupon reset date. There is typically a formula for the new coupon rate that has the following generic formula:

| Reference rate + Quoted margin |

The quoted margin is the additional amount that the issuer agrees to pay above the reference rate. The most common reference rate is the London Interbank Offered Rate (LIBOR). LIBOR is the interest rate at which major international banks offer each other on Eurodollar certificates of deposit with given maturities. The maturities range from overnight to five years. Suppose that the reference rate is one-month LIBOR and the index spread is 80 basis points. (A basis point is equal to 0.0001 or 0.01%. Thus, 100 basis points are equal to 1%.) Then the coupon reset formula is:

| One-month LIBOR + 80 basis points |

So, if one-month LIBOR on the coupon reset date is 4.6%, the coupon rate is reset for that period at 5.4% (4.6% plus 80 basis points).

The quoted margin need not be a positive value. It could be subtracted from the reference rate. For example, the reference rate could be the yield on a five-year Treasury security and the coupon rate could reset every six months based on the following coupon reset formula:

While the reference rate for most floating-rate securities is an interest rate or an interest rate index, there are some issues where this is not the case. Instead, the reference rate can be some financial index such as the return on the Standard & Poor's 500 index or a nonfinancial index such as the price of a commodity or the consumer price index.

Typically, the coupon reset formula on floating-rate securities is such that the coupon rate increases when the reference rate increases, and decreases when the reference rate decreases. There are issues whose coupon rate moves in the opposite direction from the change in the reference rate. Such issues are called inverse floaters or reverse floaters. A general coupon reset formula for an inverse floater is:

For example, suppose that for a particular inverse floater K is 10% and L is 1. Then the coupon reset formula would be:

Suppose that the reference rate is one-month LIBOR, then the coupon reset formula would be:

If in some month one-month LIBOR at the coupon reset date is 5%, the coupon rate for the period is 5%. If in the next month one-month LIBOR declines to 4.5%, the coupon rate increases to 5.5%.

A floating-rate security may have a restriction on the maximum coupon rate that will be paid at a reset date. The maximum coupon rate is called a cap. Because a cap restricts the coupon rate from increasing, a cap is an unattractive feature for the investor. In the case of an inverse floater, one can see from the general formula that the maximum interest rate would be K. This occurs when the reference rate is zero. In contrast, there could be a floor which is the minimum coupon rate specified and this is an attractive feature for the investor.

Not all floating-rate notes have the generic formula given above. Some have a coupon rate that depends on the range for a reference rate. This type of floating-rate security, called a range note, has a coupon rate equal to the reference rate as long as the reference rate is within a certain range at the reset date. If the reference rate is outside of the range, the coupon rate is zero for that period. For example, a three-year range note might specify that the reference rate is one-year LIBOR and that the coupon rate resets every year. The coupon rate for the year will be one-year LIBOR as long as one-year LIBOR at the coupon reset date falls within the range as specified below:

Year 1 | Year 2 | Year 3 | |

|---|---|---|---|

Lower limit of range | 4.5% | 5.25% | 6.00% |

Upper limit of range | 5.5% | 6.75% | 7.50% |

If one-year LIBOR is outside of the range, the coupon rate is zero. For example, if in year 1 one-year LIBOR is 5% at the coupon reset date, the coupon rate for the year is 5%. However, if one-year LIBOR is 6%, the coupon rate for the year is zero since one-year LIBOR is greater than the upper limit for year 1 of 5.5%.

In the United States, coupon interest is typically paid semiannual for government bonds, corporate, agency, and municipal bonds. In some countries, interest is paid annually. For mortgage-backed and asset-backed securities, interest is usually paid monthly. The coupon interest payment is made to the bondholder of record. Thus, if an investor sells a bond between coupon payments and the buyer holds it until the next coupon payment, then the entire coupon interest earned for the period will be paid to the buyer of the bond since the buyer will be the holder of record. The seller of the bond gives up the interest from the time of the last coupon payment to the time until the bond is sold. The amount of interest over this period that will be received by the buyer even though it was earned by the seller is called accrued interest.

In the United States and in many countries, the bond buyer must compensate the bond seller for the accrued interest. The amount that the buyer pays the seller is the agreed-upon price for the bond plus accrued interest. This amount is called the full price. The agreed-upon bond price without accrued interest is called the clean price.

A bond in which the buyer must pay the seller accrued interest is said to be trading cum-coupon. If the buyer forgoes the next coupon payment, the bond is said to be trading ex-coupon. In the United States, bonds are always traded cum-coupon. There are bond markets outside the United States where bonds are traded ex-coupon for a certain period before the coupon payment date.

There are exceptions to the rule that the bond buyer must pay the bond seller accrued interest. The most important exception is when the issuer has not fulfilled its promise to make the periodic payments. In this case, the issuer is said to be in default. In such instances, the bond's price is sold without accrued interest and is said to be traded flat.

When calculating accrued interest, three pieces of information are needed: (1) the number of days in the accrued interest period, (2) the number of days in the coupon period, and (3) the dollar amount of the coupon payment. The number of days in the accrued interest period represents the number of days over which the investor has earned interest. Given these values, the accrued interest (AI), assuming semiannual payments, is calculated as follows:

For example, suppose that (1) there are 50 days in the accrued interest period, (2) there are 183 days in a coupon period, and (3) the annual coupon per $100 of par value is $8. Then the accrued interest is:

It is not simple to determine the number of days in the accrued interest period and the number of days in the coupon period. The calculation begins with the determination of three key dates:

Trade date

Settlement date

Value date

The trade date is the date on which the transaction is executed. The settlement date is the date a transaction is completed. The settlement date varies by the type of bond. Unlike the settlement date, the value date is not constrained to fall on a business day.

Interest accrues on a bond from and including the date of the previous coupon up to but excluding the value date. (This is the definition used by the International Securities Market Association [ISMA].) However, this may differ slightly in some non-U.S. markets. For example, in some countries interest accrues up to and including the value date. For a newly issued security, there is no previous coupon payment. Instead, the interest accrues from a date called the dated date.

Day Count Conventions

The number of days in the accrued interest period and the number of days in the coupon period may not be simply the actual number of calendar days between two dates. The reason is that there is a market convention for each type of security that specifies how to determine the number of days between two dates. These conventions are called day count conventions.

In calculating the number of days between two dates, the actual number of days is not always the same as the number of days that should be used in the accrued interest formula. The number of days used depends on the day count convention for the particular security. Specifically, there are different day count conventions for Treasury securities than for government agency securities, municipal bonds, and corporate bonds.

For coupon-bearing Treasury securities, the day count convention used is to determine the actual number of days between two dates. This is referred to as the "actual/actual day count convention." For example, consider a coupon-bearing Treasury security whose previous coupon payment was March 1. The next coupon payment would be on September 1. Suppose this Treasury security is purchased with a value date of July 17. The actual number of days between July 17 (the value date) and September 1 (the date of the next coupon payment is 46 days) is shown below:

July 17 to July 31 | 14 days |

August | 31 days |

September 1 | 1 day |

46 days |

The number of days in the coupon period is the actual number of days between March 1 and September 1, which is 184 days. The number of days between the last coupon payment (March 1) to July 17 is therefore 138 days (184 days −46 days).

For coupon-bearing agency, municipal, and corporate bonds, a different day count convention is used. It is assumed that every month has 30 days, that any 6-month period has 180 days, and that there are 360 days in a year. This day count convention is referred to as the "30/360 day count convention." For example, consider a security purchased with a value date of July 17, the previous coupon payment on March 1, and the next coupon payment on September 1. If the security is an agency, municipal, or corporate bond rather than a Treasury security, the number of days until the next coupon payment is 44 days as shown below:

July 17 to July 31 | 13 days |

August | 30 days |

September 1 | 1 day |

44 days |

The number of days from March 1 to July 17 is 136, which is the number of days in the accrued interest period.

The issuer of a bond agrees to repay the principal by the stated maturity date. The issuer can agree to repay the entire amount borrowed in one lump sum payment at the maturity date. That is, the issuer is not required to make any principal repayments prior to the maturity date. Such bonds are said to have a bullet maturity.

There are bond issues which consist of a series of blocks of securities maturing in sequence. The blocks of securities are said to be serial bonds. The coupon rate for each block can be different. One type of corporate bond in which there are serial bonds is an equipment trust certificate. Municipal bonds are often issued as serial bonds.

Bonds backed by pools of loans (mortgage-backed securities and asset-backed securities) often have a schedule of principal repayments. Such bonds are said to be amortizing securities. For many loans, the payments are structured so that when the last loan payment is made, the entire amount owed is fully paid off. Another example of an amortizing feature is a bond that has a sinking fund provision. This provision for repayment of a bond may be designed to liquidate all of an issue by the maturity date, or it may be arranged to repay only a part of the total by the maturity date.

A bond issue may have a call provision granting the issuer an option to retire all or part of the issue prior to the stated maturity date. Some issues specify that the issuer must retire a predetermined amount of the issue periodically. Various types of call provisions are discussed below.

Call and Refunding Provisions

An issuer generally wants the right to retire a bond issue prior to the stated maturity date because it recognizes that at some time in the future the general level of interest rates may fall sufficiently below the issue's coupon rate so that redeeming the issue and replacing it with another issue with a lower coupon rate would be economically beneficial. This right is a disadvantage to the bondholder since proceeds received must be reinvested at a lower interest rate. As a result, an issuer who wants to include this right as part of a bond offering must compensate the bondholder when the issue is sold by offering a higher coupon rate, or equivalently, accepting a lower price than if the right is not included.

The right of the issuer to retire the issue prior to the stated maturity date is referred to as a call option. If an issuer exercises this right, the issuer is said to "call the bond." The price which the issuer must pay to retire the issue is referred to as the call price. There may not be a call price but a call schedule which sets forth a call price based on when the issuer can exercise the call option.

When a bond is issued, typically the issuer may not call the bond for a number of years. That is, the issue is said to have a deferred call. The date at which the bond may first be called is referred to as the first call date. However, not all issues have a deferred call. If a bond issue does not have any protection against early call, then it is said to be a currently callable issue. But most new bond issues, even if currently callable, usually have some restrictions against certain types of early redemption. The most common restriction is that prohibiting the refunding of the bonds for a certain number of years. Refunding a bond issue means redeeming bonds with funds obtained through the sale of a new bond issue.

Call protection is much more absolute than refunding protection. While there may be certain exceptions to absolute or complete call protection in some cases, it still provides greater assurance against premature and unwanted redemption than does refunding protection. Refunding prohibition merely prevents redemption only from certain sources of funds, namely the proceeds of other debt issues sold at a lower cost of money. The bondholder is only protected if interest rates decline, and the borrower can obtain lower-cost money to pay off the debt.

Bonds can be called in whole (the entire issue) or in part (only a portion). When less than the entire issue is called, the specific bonds to be called are selected randomly or on a pro rata basis.

Generally, the call schedule is such that the call price at the first call date is a premium over the par value and scaled down to the par value over time. The date at which the issue is first callable at par value is referred to as the first par call date. However, not all issues have a call schedule in which the call price starts out as a premium over par. There are issues where the call price at the first call date and subsequent call dates is par value. In such cases, the first call date is the same as the first par call date.

For zero-coupon bonds, there are three types of call schedules that can be used. The first is a call schedule for which the call price is below par value at the first call date and scales up to par value over time. The second type is one in which the call price at the first call date is above par and scales down to par. The third type is a schedule in which the call price is par value at the first call date and any subsequent call date.

The call prices in a call schedule are referred to as the regular or general redemption prices. There are also special redemption prices for debt redeemed through the sinking fund and through other provisions, and the proceeds from the confiscation of property through the right of eminent domain. The special redemption price is usually par value, but in the case of some utility issues it initially may be the public offering price, which is amortized down to par value (if a premium) over the life of the bonds.

Prepayments

For amortizing securities backed by loans and have a schedule of principal repayments, individual borrowers typically have the option to pay off all or part of their loan prior to the scheduled date. Any principal repayment prior to the scheduled date is called a prepayment. The right of borrowers to prepay is called the prepayment option.

Basically, the prepayment option is the same as a call option. However, unlike a call option, there is not a call price that depends on when the borrower pays off the issue. Typically, the price at which a loan is prepaid is at par value.

Sinking Fund Provision

A sinking fund provision included in a bond indenture requires the issuer to retire a specified portion of an issue each year. Usually, the periodic payments required for sinking fund purposes will be the same for each period. A few indentures might permit variable periodic payments, where payments change according to certain prescribed conditions set forth in the indenture. The alleged purpose of the sinking fund provision is to reduce credit risk. This kind of provision for repayment of debt may be designed to liquidate all of a bond issue by the maturity date, or it may be arranged to pay only a part of the total by the end of the term. If only a part is paid, the remainder is called a balloon maturity. Many indentures include a provision that grants the issuer the option to retire more than the amount stipulated for sinking fund retirement. This is referred to as an accelerated sinking fund provision.

To satisfy the sinking fund requirement, an issuer is typically granted one of following choices: (1) make a cash payment of the face amount of the bonds to be retired to the trustee, who then calls the bonds for redemption using a lottery, or (2) deliver to the trustee bonds purchased in the open market that have a total par value equal to the amount that must be retired. If the bonds are retired using the first method, interest payments stop at the redemption date.

Usually the sinking fund call price is the par value if the bonds were originally sold at par. When issued at a price in excess of par, the call price generally starts at the issuance price and scales down to par as the issue approaches maturity.

There is a difference between the amortizing feature for a bond with a sinking fund provision, and the regularly scheduled principal repayment for a mortgage-backed and an asset-backed security. The owner of a mortgage-backed security and an asset-backed security knows that assuming no default that there will be principal repayments. In contrast, the owner of a bond with a sinking fund provision is not assured that his or her particular holding will be called to satisfy the sinking fund requirement.

A provision in the indenture could grant either the bondholder and/or the issuer an option to take some action against the other party. The most common type of option embedded in a bond is a call option which we discussed above. This option is granted to the issuer. There are two options that can be granted to the bondholder: the right to put the issue and the right to convert the issue.

An issue with a put provision grants the bondholder the right to sell the issue (that is, force the issuer to redeem the issue) at a specified price on designated dates. The specified price is called the put price. Typically, a bond is puttable at par value if it is issued at or close to par value. For a zero-coupon bond, the put price is below par. The advantage of the put provision to the bondholder is that if after the issue date market rates rise above the issue's coupon rate, the bondholder can force the issuer to redeem the bond at the put price and then reinvest the proceeds at the prevailing higher rate.

A convertible bond is an issue giving the bondholder the right to exchange the bond for a specified number of shares of common stock. Such a feature allows the bondholder to take advantage of favorable movements in the price of the issuer's common stock. An exchangeable bond allows the bondholder to exchange the issue for a specified number of shares of common stock of a corporation different from the issuer of the bond. Convertible bonds are described in Chapter 29 of Volume I.

The payments that the issuer makes to the bondholder can be in any currency. For bonds issued in the United States, the issuer typically makes both coupon payments and principal repayments in U.S. dollars. However, there is nothing that forces the issuer to make payments in U.S dollars. The indenture can specify that the issuer may make payments in some other specified currency. For example, payments may be made in euros or yen.

An issue in which payments to bondholders are in U.S. dollars is called a dollar-denominated issue. A nondollar-denominated issue is one in which payments are not denominated in U.S. dollars. There are some issues whose coupon payments are in one currency and whose principal payment is in another currency. An issue with this characteristic is called a dual-currency issue.

Some issues allow either the issuer or the bondholder the right to select the currency in which a payment will be paid. This option effectively gives the party with the right to choose the currency the opportunity to benefit from a favorable exchange rate movement.

When an investor purchases a bond, he or she can expect to receive a dollar return from one or more of the following sources:

The coupon interest payments made by the issuer.

Any capital gain (or capital loss—a negative dollar return) when the security matures, is called, or is sold.

Income from reinvestment of the interim cash flows.

Any yield measure that purports to measure the potential return from a bond should consider all three sources of return described above.

The most obvious source of return is the periodic coupon interest payments. For zero-coupon instruments, the return from this source is zero, although the investor is effectively receiving interest by purchasing a security below its par value and realizing interest at the maturity date when the investor receives the par value.

When the proceeds received when a bond matures, is called, or is sold are greater than the purchase price, a capital gain results. For a bond held to maturity, there will be a capital gain if the bond is purchased below its par value. A bond purchased below its par value is said to be purchased at a discount. For example, a bond purchased for $94.17 with a par value of $100 will generate a capital gain of $5.83 ($100 – $94.17) if held to maturity. For a callable bond, a capital gain results if the price at which the bond is called (that is, the call price) is greater than the purchase price. For example, if the bond in our previous example is callable and subsequently called at $100.5, a capital gain of $6.33 ($100.5 – $94.17) will be realized. If the same bond is sold prior to its maturity or before it is called, a capital gain will result if the proceeds exceed the purchase price. So, if our hypothetical bond is sold prior to the maturity date for $103, the capital gain would be $8.83 ($103 – $94.17).

A capital loss is generated when the proceeds received when a bond matures, is called, or is sold are less than the purchase price. For a bond held to maturity, there will be a capital loss if the bond is purchased for more than its par value. A bond purchased for more than its par value is said to be purchased at a premium. For example, a bond purchased for $102.5 with a par value of $100 will generate a capital loss of $2.5 ($102.5 – $100) if held to maturity. For a callable bond, a capital loss results if the price at which the bond is called is less than the purchase price. For example, if the bond in our previous example is callable and subsequently called at $100.5, a capital loss of $2 ($102.5 – $100.5) will be realized. If the same bond is sold prior to its maturity or before it is called, a capital loss will result if the sale price is less than the purchase price. So, if our hypothetical bond is sold prior to the maturity date for $98.5, the capital loss would be $4 ($102.5 – $98.5).

With the exception of zero-coupon instruments, bonds make periodic payments of interest that can be reinvested until the security is removed from the portfolio. There are also instruments in which there are periodic principal repayments that can be reinvested until the security is removed from the portfolio. Repayment of principal prior to the maturity date occurs for amortizing instruments such as mortgage-backed securities and asset-backed securities. The interest earned from reinvesting the interim cash flows (interest and/or principal payments) until the security is removed from the portfolio is called reinvestment income.

There are several yield measures cited in the bond market. These include current yield, yield to maturity, yield to call, yield to put, yield to worst, and cash flow yield. Below we explain how each measure is calculated and its limitations.

The current yield relates the annual dollar coupon interest to the market price. The formula for the current yield is:

For example, the current yield for a 7% 8-year bond whose price is $94.17 is 7.43% as shown below:

The current yield will be greater than the coupon rate when the bond sells at a discount; the reverse is true for a bond selling at a premium. For a bond selling at par, the current yield will be equal to the coupon rate.

The drawback of the current yield is that it considers only the coupon interest and no other source that will impact an investor's return. No consideration is given to the capital gain that the investor will realize when a bond is purchased at a discount and held to maturity; nor is there any recognition of the capital loss that the investor will realize if a bond purchased at a premium is held to maturity.

The most popular measure of yield in the bond market is the yield to maturity. The yield to maturity is the interest rate that will make the present value of the cash flows from a bond equal to its market price plus accrued interest. To find the yield to maturity, we first determine the cash flows. Then an iterative procedure is used to find the interest rate that will make the present value of the cash flows equal to the market price plus accrued interest. In the illustrations presented below, we assume that the next coupon payment will be 6 months from now so that there is no accrued interest.

To illustrate, consider a 7% 8-year bond selling for $94.17. The cash flows for this bond are (1) 16 payments every 6 months of $3.50 and (2) a payment 16 6-month periods from now of $100. The present value using various discount (interest) rates is:

Interest rate | 3.5% | 3.6% | 3.7% | 3.8% | 3.9% | 4.0% |

Present value | 100.00 | 98.80 | 97.62 | 96.45 | 95.30 | 94.17 |

When a 4.0% interest rate is used, the present value of the cash flows is equal to $94.17, which is the price of the bond. Hence, 4.0% is the semiannual yield to maturity.

The market convention adopted is to double the semiannual yield and call that the yield to maturity. Thus, the yield to maturity for the above bond is 8% (2 times 4.0%). The yield to maturity computed using this convention— doubling the semiannual yield—is called a bond-equivalent yield.

The following relationships between the price of a bond, coupon rate, current yield, and yield to maturity hold:

Bond selling at | Relationship | ||||

|---|---|---|---|---|---|

Par | Coupon rate | = | Current yield | = | YTM |

Discount | Coupon rate | > | Current yield | > | YTM |

Premium | Coupon rate | < | Current yield | < | YTM |

The yield to maturity considers not only the coupon income but also any capital gain or loss that the investor will realize by holding the bond to maturity. The yield to maturity also considers the timing of the cash flows. It does consider reinvestment income; however, it assumes that the coupon payments can be reinvested at an interest rate equal to the yield to maturity. So, if the yield to maturity for a bond is 8%, for example, to earn that yield the coupon payments must be reinvested at an interest rate equal to 8%. The following illustration clearly demonstrates this point.

Suppose an investor has $94.17 and places the funds in a certificate of deposit that pays 4% every 6 months for 8 years or 8% per year (on a bond-equivalent basis). At the end of 8 years, the $94.17 investment will grow to $176.38. Instead, suppose an investor buys the following bond: a 7% 8-year bond selling for $94.17. The yield to maturity for this bond is 8%. The investor would expect that at the end of 8 years, the total dollars from the investment will be $176.38.

Let's look at what the investor will receive. There will be 16 semiannual interest payments of $3.50, which will total $56. When the bond matures, the investor will receive $100. Thus, the total dollars that the investor will receive is $156 by holding the bond to maturity. But this is less than the $176.38 necessary to produce a yield of 8% on a bond-equivalent basis by $20.38 ($176.38 minus $156). How is this deficiency supposed to be made up? If the investor reinvests the coupon payments at a semiannual interest rate of 4% (or 8% annual rate on a bond-equivalent basis), then the interest earned on the coupon payments will be $20.38. Consequently, of the $82.21 total dollar return ($176.38 minus $94.17) necessary to produce a yield of 8%, about 25% ($20.38 divided by $82.21) must be generated by reinvesting the coupon payments.

Clearly, the investor will only realize the yield to maturity that is stated at the time of purchase if (1) the coupon payments can be reinvested at the yield to maturity and (2) the bond is held to maturity. With respect to the first assumption, the risk that an investor faces is that future interest rates will be less than the yield to maturity at the time the bond is purchased. This risk is referred to as reinvestment risk—a risk we explain later in this chapter. If the bond is not held to maturity, it may have to be sold for less than its purchase price, resulting in a return that is less than the yield to maturity. The risk that a bond will have to be sold at a loss is referred to as interest rate risk as explained later in this chapter.

There are two characteristics of a bond that determine the degree of reinvestment risk. First, for a given yield to maturity and a given coupon rate, the longer the maturity the more the bond's total dollar return is dependent on reinvestment income to realize the yield to maturity at the time of purchase (that is, the greater the reinvestment risk). The implication is that the yield to maturity measure for long-term coupon bonds tells little about the potential yield that an investor may realize if the bond is held to maturity. For long-term bonds, in high interest rate environments the reinvestment income component may be as high as 70% of the bond's potential total dollar return.

The second characteristic that determines the degree of reinvestment risk is the coupon rate. For a given maturity and a given yield to maturity, the higher the coupon rate, the more dependent the bond's total dollar return will be on the reinvestment of the coupon payments in order to produce the yield to maturity at the time of purchase. This means that holding maturity and yield to maturity constant, premium bonds will be more dependent on reinvestment income than bonds selling at par. In contrast, discount bonds will be less dependent on reinvestment income than bonds selling at par. For zero-coupon bonds, none of the bond's total dollar return is dependent on reinvestment income. So, a zero-coupon bond has no reinvestment risk if held to maturity.

When a bond is callable, the practice has been to calculate a yield to call as well as a yield to maturity. As explained earlier, a callable bond may have a call schedule. The yield to call assumes that the issuer will call the bond at some assumed call date and the call price is then the call price specified in the call schedule.

Typically, investors calculate a yield to first call or yield to next call, a yield to first par call, and yield to refunding. The yield to first call is computed for an issue that is not currently callable, while the yield to next call is computed for an issue that is currently callable. Yield to refunding is used when bonds are currently callable but have some restrictions on the source of funds used to buy back the debt when a call is exercised. The refunding date is the first date the bond can be called using lower-cost debt.

The procedure for calculating any yield to call measure is the same as for any yield calculation: determine the interest rate that will make the present value of the expected cash flows equal to the price plus accrued interest. In the case of yield to first call, the expected cash flows are the coupon payments to the first call date and the call price. For the yield to first par call, the expected cash flows are the coupon payments to the first date at which the issuer can call the bond at par and the par value. For the yield to refunding, the expected cash flows are the coupon payments to the first refunding date and the call price at the first refunding date.

To illustrate the computation, consider a 7% 8-year bond with a maturity value of $100 selling for $106.36. Suppose that the first call date is 3 years from now and the call price is $103. The cash flows for this bond if it is called in 3 years are (1) six coupon payments of $3.50 and (2) $103 in six 6-month periods from now. The process for finding the yield to first call is the same as for finding the yield to maturity. It can be shown that a semiannual interest rate of 2.8% makes the present value of the cash flows equal to the price is 2.8%. Therefore, the yield to first call on a bond-equivalent basis is 5.6%.

Let's take a closer look at the yield to call as a measure of the potential return of a security. The yield to call does consider all three sources of potential return from owning a bond. However, as in the case of the yield to maturity, it assumes that all cash flows can be reinvested at the yield to call until the assumed call date. As we just demonstrated, this assumption may be inappropriate. Moreover, the yield to call assumes that (1) the investor will hold the bond to the assumed call date and (2) the issuer will call the bond on that date.

These assumptions underlying the yield to call are often unrealistic. They do not take into account how an investor will reinvest the proceeds if the issue is called. For example, consider two bonds, M and N. Suppose that the yield to maturity for bond M, a 5-year noncallable bond, is 7.5%, while for bond N the yield to call assuming the bond will be called in 3 years is 7.8%. Which bond is better for an investor with a 5-year investment horizon? It's not possible to tell for the yields cited. If the investor intends to hold the bond for 5 years and the issuer calls bond N after 3 years, the total dollars that will be available at the end of 5 years will depend on the interest rate that can be earned from investing funds from the call date to the end of the investment horizon.

When a bond is puttable, the yield to the first put date is calculated. The yield to put is the interest rate that will make the present value of the cash flows to the first put date equal to the price plus accrued interest. As with all yield measures (except the current yield), yield to put assumes that any interim coupon payments can be reinvested at the yield calculated. Moreover, the yield to put assumes that the bond will be put on the first put date.

A yield can be calculated for every possible call date and put date. In addition, a yield to maturity can be calculated. The lowest of all these possible yields is called the yield to worst. For example, suppose that there are only four possible call dates for a callable bond and that a yield to call assuming each possible call date is 6%, 6.2%, 5.8%, and 5.7%, and that the yield to maturity is 7.5%. Then the yield to worst is the minimum of these values, 5.7% in our example.

The yield to worst measure holds little meaning as a measure of potential return.

Mortgage-backed securities and asset-backed securities are backed by a pool of loans. The cash flows for these securities include principal repayment as well as interest. The complication that arises is that the individual borrowers whose loans make up the pool typically can prepay their loan in whole or in part prior to the scheduled principal repayment date. Because of prepayments, in order to project the cash flows it is necessary to make an assumption about the rate at which prepayments will occur. This rate is called the prepayment rate or prepayment speed.

Given the cash flows based on the assumed prepayment rate, a yield can be calculated. The yield is the interest rate that will make the present value of the projected cash flows equal to the price plus accrued interest. A yield calculated in this way is called a cashflow yield.

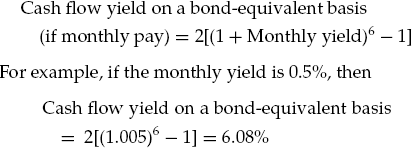

Typically, the cash flows for mortgage-backed and asset-backed securities are monthly. Therefore, the interest rate that will make the present value of the projected principal repayment and interest payments equal to the market price plus accrued interest is a monthly rate. The bond-equivalent yield is found by calculating the effective 6-month interest rate and then doubling it. That is:

As we have noted, the yield to maturity has two shortcomings as a measure of a bond's potential return: (1) it is assumed that the coupon payments can be reinvested at a rate equal to the yield to maturity, and (2) it is assumed that the bond is held to maturity. These shortcomings are equally present in application of the cash flow yield measure: (1) the projected cash flows are assumed to be reinvested at the cash flow yield, and (2) the mortgage-backed or asset-backed security is assumed to be held until the final payoff of all the loans based on some prepayment assumption. The importance of reinvestment risk—the risk that the cash flows will be reinvested at a rate less than the cash flow yield—is particularly important for mortgage-backed and asset-backed securities since payments are typically monthly and include principal repayments (scheduled and prepayments), as well as interest. Moreover, the cash flow yield is dependent on realization of the projected cash flows according to some prepayment rate. If actual prepayments differ significantly from the prepayment rate assumed, the cash flow yield will not be realized.

Bonds expose an investor to one or more of the following risks: (1) interest rate risk; (2) call and prepayment risk; (3) credit risk; (4) liquidity risk; (5) exchange rate or currency risk; and (6) inflation or purchasing power risk.

The price of a typical bond will change in the opposite direction from a change in interest rates. That is, when interest rates rise, a bond's price will fall; when interest rates fall, a bond's price will rise. For example, consider a 6% 20-year bond. If the yield investors require to buy this bond is 6%, the price of this bond would be $100. However, if the required yield increased to 6.5%, the price of this bond would decline to $94.4479. Thus, for a 50-basis-point increase in yield, the bond's price declines by 5.55%. If, instead, the yield declines from 6% to 5.5%, the bond's price will rise by 6.02% to $106.0195.

The reason for this inverse relationship between price and changes in interest rates or changes in market yields is as follows. Suppose investor X purchases our hypothetical 6% coupon 20-year bond at par value ($100). The yield for this bond is 6%. Suppose that immediately after the purchase of this bond two things happen. First, market interest rates rise to 6.50% so that if an investor wants to buy a similar 20-year bond a 6.50% coupon rate would have to be paid by the bond issuer in order to offer the bond at par value. Second, suppose investor X wants to sell the bond. In attempting to sell the bond, investor X would not find an investor who would be willing to pay par value for a bond with a coupon rate of 6%. The reason is that any investor who wanted to purchase this bond could obtain a similar 20-year bond with a coupon rate 50 basis points higher, 6.5%. What can the investor do? The investor cannot force the issuer to change the coupon rate to 6.5%. Nor can the investor force the issuer to shorten the maturity of the bond to a point where a new investor would be willing to accept a 6% coupon rate. The only thing that the investor can do is adjust the price of the bond so that at the new price the buyer would realize a yield of 6.5%. This means that the price would have to be adjusted down to a price below par value. The new price must be $94.4469. While we assumed in our illustration an initial price of par value, the principle holds for any purchase price. Regardless of the price that an investor pays for a bond, an increase in market interest rates will result in a decline in a bond's price.

Suppose instead of a rise in market interest rates to 6.5%, they decline to 5.5%. Investors would be more than happy to purchase the 6% coupon 20-year bond for par value. However, investor X realizes that the market is only offering investors the opportunity to buy a similar bond at par value with a coupon rate of 5.5%. Consequently, investor X will increase the price of the bond until it offers a yield of 5.5%. That price is $106.0195.

Since the price of a bond fluctuates with market interest rates, the risk that an investor faces is that the price of a bond held in a portfolio will decline if market interest rates rise. This risk is referred to as interest rate risk and is a major risk faced by investors in the bond market.

Bond Features that Affect Interest Rate Risk

The degree of sensitivity of a bond's price to changes in market interest rates depends on various characteristics of the issue, such as maturity and coupon rate. Consider first maturity. All other factors constant, the longer the maturity, the greater the bond's price sensitivity to changes in interest rates. For example, we know that for a 6% 20-year bond selling to yield 6%, a rise in the yield required by investors to 6.5% will cause the bond's price to decline from $100 to $94.4479, a 5.55% price decline. For a 6% 5-year bond selling to yield 6%, the price is $100. A rise in the yield required by investors from 6% to 6.5% would decrease the price to $97.8944. The decline in the bond's price is only 2.11%.

Now let's turn to the coupon rate. A property of a bond is that all other factors constant, the lower the coupon rate, the greater the bond's price sensitivity to changes in interest rates. For example, consider a 9% 20-year bond selling to yield 6%. The price of this bond would be $112.7953. If the yield required by investors increases by 50 basis points to 6.5%, the price of this bond would fall by 2.01% to $110.5280. This decline is less than the 5.55% decline for the 6% 20-year bond selling to yield 6%. An implication is that zero-coupon bonds have greater price sensitivity to interest rate changes than same-maturity bonds bearing a coupon rate and trading at the same yield.

Because of default or credit risk (discussed later), different bonds trade at different yields, even if they have the same coupon rate and maturity. How, then, holding other factors constant, does the level of interest rates affect a bond's price sensitivity to changes in interest rates? As it turns out, the higher the level of interest rates that a bond trades at, the lower the price sensitivity.

To see this, we can compare a 6% 20-year bond initially selling at a yield of 6%, and a 6% 20-year bond initially selling at a yield of 10%. The former is initially at a price of $100, and the latter carries a price of $65.68. Now, if the yield on both bonds increases by 100 basis points, the first bond trades down by 10.68 points (10.68%). After the assumed increase in yield, the second bond will trade at a price of $59.88, for a price decline of only 5.80 points (or 8.83%). Thus, we see that the bond that trades at a lower yield is more volatile in both percentage price change and absolute price change, as long as the other bond characteristics are the same. An implication of this is that, for a given change in interest rates, price sensitivity is lower when the level of interest rates in the market is high, and price sensitivity is higher when the level of interest rates is low.

We can summarize these three characteristics that affect the bond's price sensitivity to changes in market interest rates as follows:

- Characteristic 1:

For a given maturity and initial yield, the lower the coupon rate the greater the bond's price sensitivity to changes in market interest rates.

- Characteristic 2:

For a given coupon rate and initial yield, the longer the maturity of a bond the greater the bond's price sensitivity to changes in market interest rates.

- Characteristic 3:

For a given coupon rate and maturity, the lower the level of interest rates the greater the bond's price sensitivity to changes in market interest rates.

A bond's price sensitivity bond will also depend on any options embedded in the issue. This is explained below when we discuss call risk.

Interest Rate Risk for Floating-Rate Securities

The change in the price of a fixed-rate coupon bond when market interest rates change is due to the fact that the bond's coupon rate differs from the prevailing market interest rate. For a floating-rate security, the coupon rate is reset periodically based on the prevailing value for the reference rate plus the contractually specified index spread. The index spread is set for the life of the security. The price of a floating-rate security will fluctuate depending on the following three factors.

First, the longer the time to the next coupon reset date, the greater the potential price fluctuation. For example, consider a floating-rate security whose coupon resets every six months and the coupon formula is 6-month LIBOR plus 20 basis points. Suppose that on the coupon reset date 6-month LIBOR is 5.8%. If the next day after the coupon is reset, 6-month LIBOR rises to 6.1%, this means that this security is offering a 6-month coupon rate that is less than the prevailing 6-month rate for the remaining six months. The price of the security must decline to reflect this. Suppose instead that the coupon resets every month at 1-month LIBOR and that this rate rises right after a coupon rate is reset. Then, while the investor would be realizing a submarket 1-month coupon rate, it is for only a month. The price decline will be less than for the security that resets every six months.

The second reason why a floating-rate security's price will fluctuate is that the index spread that investors want in the market changes. For example, consider once again the security whose coupon reset formula is 6-month LIBOR plus 20 basis point. If market conditions change such that investors want an index spread of 30 basis points rather than 20 basis points, this security would be offering a coupon rate that is 10 basis points below the market rate. As a result, the security's price will decline.

Finally, as noted earlier, a floating-rate security may have a cap. Once the coupon rate as specified by the coupon reset formula rises above the cap rate, the security offers a below market coupon rate and its price will decline. In fact, once the cap is reached, the security's price will react much the same way to changes in market interest rates as that of a fixed-rate coupon security.

Measuring Interest Rate Risk

Investors are interested in estimating the price sensitivity of a bond to changes in market interest rates. The measure commonly used to approximate the percentage price change is duration. Duration gives the approximate percentage price change for a 100 basis point change in interest rates. Chapters 13 and 14 of Volume III explains the concept of duration and its measurement.

The duration for the 6% coupon 5-year bond trading at par to yield 6% is 4.27. Thus, the price of this bond will change by approximately 4.27% if interest rates change by 100 basis points. For a 50 basis point change, this bond's price will change by approximately 2.14% (4.27% divided by 2). As explained above, this bond's price would actually change by 2.11%. Thus, duration does a good job of approximating the percentage price change. It turns out that the approximation is good the smaller the change in interest rates. The approximation is not as good for a large change in interest rates.

As explained earlier, a bond may include a provision that allows the issuer to retire or call all or part of the issue before the maturity date. From the investor's perspective, there are three disadvantages to call provisions. First, the cash flow pattern of a callable bond is not known with certainty. Second, because the issuer will call the bonds when interest rates have dropped, the investor is exposed to reinvestment risk; that is, the investor will have to reinvest the proceeds when the bond is called at relatively lower interest rates. Finally, the capital appreciation potential of a bond will be reduced, because the price of a callable bond may not rise much above the price at which the issuer will call the bond. Because of these disadvantages faced by the investor, a callable bond is said to expose the investor to call risk. The same disadvantages apply to bonds that can prepay. In this case the risk is referred to as prepayment risk.

In general, one thinks of credit risk as the risk that the debtor will fail to satisfy its obligation to the lender (that is, timely payment of principal and/or interest). That is in fact one form of risk referred to as default risk. Default risk is gauged by credit ratings assigned by three nationally recognized statistical rating companies: Moody's Investors Service, Standard & Poor's Corporation, and Fitch Ratings. These organizations are popularly referred to as rating agencies. We discuss these ratings assigned in Chapter 24 of Volume III.

Bonds with default risk trade in the market at a price that is lower than comparable U.S. government securities, which are considered free of default risk. In other words, a non-U.S. government taxable bond will trade in the market at a higher yield than a U.S. government taxable bond that is otherwise comparable in terms of maturity and coupon rate.

Except in the case of the lowest-rated securities, known as "high-yield" or "junk bonds," an investor is normally more concerned with the changes in the perceived default risk than with the actual event of default. Even though the actual default of an issuer may be highly unlikely, an investor is concerned about the impact that a change in perceived default risk can have on a bond's price. If the perceived default risk increases, the market will require a higher yield for the security. As a result, a bond's price will decline. This risk is referred to as credit spread risk. A decline in the price of a bond will also occur if an issue's credit rating is lowered. By a lower credit rating, it is meant the issue is "downgraded." This risk is referred to as downgrade risk. Credit spread risk and downgrade risk are discussed in Chapter 24 of Volume III.

When an investor wants to sell a bond prior to the maturity date, he or she is concerned whether the price that can be obtained from dealers is close to the true value of the issue. For example, if recent trades in the market for a particular issue have been between 97.25 and 97.75 and market conditions have not changed, an investor would expect to sell the bond somewhere in the 97.25 to 97.75 area.

Liquidity risk is the risk that the investor will have to sell a bond below its true value where the true value is indicated by recent transactions. The primary measure of liquidity is the size of the spread between the bid price (the price at which a dealer is willing to buy a security) and the ask price (the price at which a dealer is willing to sell a security). The wider the bid-ask spread, the greater the liquidity risk.

A liquid market can generally be defined by "small bid-ask spreads which do not materially increase for large transactions" (Gerber, 1997, p. 278). Bid-ask spreads, and therefore liquidity risk, change over time.

For investors who plan to hold a bond until maturity and need not mark a position to market, liquidity risk is not a major concern. An institutional investor that plans to hold an issue to maturity but is periodically marked to market is concerned with liquidity risk. By marking a position to market, it is meant that the security is revalued in the portfolio based on its current market price. For example, mutual funds are required to mark to market at the end of each day the holdings in their portfolio in order to compute the net asset value (NAV). While other institutional investors may not mark to market as frequently as mutual funds, they are marked to market when reports are periodically sent to clients or the board of directors or trustees.

For a U.S. investor, non-dollar-denominated bond (that is, a bond whose payments are not in U.S. dollars) has unknown U.S. dollar cash flows. The dollar cash flows are dependent on the exchange rate at the time the payments are received. For example, suppose a U.S. investor purchases a bond whose payments are in euros. If the euro depreciates relative to the U.S. dollar, then fewer dollars will be received. The risk of this occurring is referred to as exchange rate risk or currency risk. Of course, should the euro appreciate relative to the U.S. dollar, the investor will benefit by receiving more dollars.

Inflation risk or purchasing power risk arises because of the variation in the value of cash flows from a security due to inflation, as measured in terms of purchasing power. For example, if an investor purchases a bond with a coupon rate of 7%, but the rate of inflation is 8%, the purchasing power of the cash flow has declined. For all but floating-rate securities, an investor is exposed to inflation risk because the interest rate the issuer promises to make is fixed for the life of the issue. To the extent that interest rates reflect the expected inflation rate, floating-rate securities have a lower level of inflation risk.

Basically, a bond is a financial obligation of an entity (the issuer) who promises to pay a specified sum of money at specified future dates. In this chapter we have described the basic features of bonds and their investment characteristics.

Bond prices are quoted as a percentage of par value, with par value equal to 100. The coupon rate is the interest rate that the issuer agrees to pay each year; the coupon is the annual amount of the interest payment and is found by multiplying the par value by the coupon rate. Zero-coupon bonds do not make periodic coupon payments; the bondholder realizes interest at the maturity date equal to the difference between the maturity value and the price paid for the bond. A step-up note is a security whose coupon rate increases over time.

A floating-rate security is an issue whose coupon rate resets periodically based on some formula; the typical coupon reset formula is some reference rate plus an index spread. A floating-rate security may have a cap which sets the maximum coupon rate that will be paid at a reset date; a cap is a disadvantage to the bondholder while a floor is an advantage to the bondholder. An inverse floater is an issue whose coupon rate moves in the opposite direction from the change in the reference rate.

Accrued interest is the amount of interest accrued since the last coupon payment and in the United States (as well as in many countries), the bond buyer must pay the bond seller the accrued interest. The full price of a security is the agreed-upon price plus accrued interest; the clean price is the agreed-upon price without accrued interest. Interest accrues on a bond from and including the date of the previous coupon up to but excluding the value date; the value date is usually, but not always, the same as the settlement date.

A bond issue may have a call provision granting the issuer an option to retire all or part of the issue prior to the stated maturity date. A call provision is an advantage to the issuer and a disadvantage to the bondholder. When a callable bond is issued, typically the issuer may not call the bond for a number of years; that is, there is a deferred call. Most new bond issues, even if currently callable, usually have some restrictions against refunding. For an amortizing security backed by a pool of loans, the borrowers typically have the right to prepay in whole or in part prior to the scheduled principal repayment date; this provision is called a prepayment option.

A puttable bond is one in which the bondholder has the right to sell the issue back to the issuer at a specified price on designated dates. A convertible bond is an issue giving the bondholder the right to exchange the bond for a specified number of shares of common stock.

The sources of return from holding a bond to maturity are the coupon interest payments, any capital gain or loss, and reinvestment income. Reinvestment income is the interest income generated by reinvesting coupon interest payments and any principal repayments from the time of receipt to the bond's maturity. The current yield relates the annual dollar coupon interest to the market price and fails to recognize any capital gain or loss and reinvestment income. The yield to maturity is the interest rate that will make the present value of the cash flows from a bond equal to the price plus accrued interest. This yield measure will only be realized if the interim cash flows can be reinvested at the yield to maturity and the bond is held to maturity. The yield to call is the interest rate that will make the present value of the expected cash flows to the assumed call date equal to the price plus accrued interest. Yield measures for callable bonds include yield to first call, yield to next call, yield to first par call, and yield to refunding. The yield to worst is the lowest yield from among all possible yield to calls, yield to puts, and the yield to maturity. For mortgage-backed and asset-backed securities, the cash flow yield based on some prepayment rate is the interest rate that equates the present value of the projected principal and interest payments to the price plus accrued interest. The cash flow yield assumes that all cash flows (principal payments and interest payments) can be reinvested at the calculated yield and that the prepayment rate will be realized over the security's life.

Bonds expose an investor to various risks. The price of a bond changes inversely with a change in market interest rates. Interest rate risk refers to the adverse price movement of a bond as a result of a change in market interest rates; for the owner of a bond it is the risk that interest rates will rise. The coupon rate and maturity of a bond affect its price sensitivity to changes in market interest rate. The duration of a bond measures the approximate percentage price change for a 100-basis-point change in interest rates.

Call risk and prepayment risk refer to the risk that a security will be paid off before the scheduled principal repayment date. From an investor's perspective, the disadvantages to call and prepayment provisions are (1) the cash flow pattern is uncertain, (2) reinvestment risk because proceeds received will have to be reinvested at a relatively lower interest rate, and (3) the capital appreciation potential of a bond will be reduced.

Credit risk consists of three types of risk: default risk, credit spread risk, and downgrade risk. Default risk is gauged by the ratings assigned by the nationally recognized statistical rating organizations (rating agencies).

Liquidity risk depends on the ease with which an issue can be sold at or near its true value and is primarily gauged by the bid-ask spread quoted by a dealer. From the perspective of a U.S. investor, exchange rate risk is the risk that a currency in which a security is denominated will depreciate relative to the U.S. dollar. Inflation risk or purchasing power risk arises because of the variation in the value of cash flows from a security due to inflation.

Choudhry, M., and Fabozzi, F. J. (eds.) (2004). Handbook of European Fixed Income Securities. Hoboken, NJ: John Wiley & Sons.

Fabozzi, F. J. (1999). Duration, Convexity, and Other Bond Risk Measures. Hoboken, NJ: John Wiley & Sons.

Fabozzi, F. J. (ed.) (2000). Investing in Asset-Backed Securities. Hoboken, NJ: John Wiley & Sons.

Fabozzi, F. J. (2002). Fixed Income Securities. Hoboken, NJ: John Wiley & Sons.

Fabozzi, F. J. (ed.) (2005). Handbook of Fixed Income Securities, 7th edition. New York: McGraw-Hill.

Fabozzi, F. J. (2006). Bond Markets, Analysis, and Strategies, 6th edition. Upper Saddle River, NJ: Prentice Hall.

Fabozzi, F. J., Bhattacharya, A. K., and Berliner W S. (2007). Mortgage-Backed Securities: Products, Structuring, and Analytical Techniques. Hoboken, NJ: John Wiley & Sons.

Fabozzi, F. J., and Mann, S.V. (2001). Floating Rate Securities. Hoboken, NJ: John Wiley & Sons.

Fabozzi, F. J., Mann, S. V., and Choudhry, M. (2002). Global Money Markets. Hoboken, NJ: John Wiley & Sons.

Gerber, R. I. (1997). A user's guide to buy-side bond trading. In F. J. Fabozzi (ed.), Managing Fixed Income Portfolios (pp. 277-290). Hoboken, NJ: John Wiley & Sons.

Wilson, R. W, and Fabozzi, F. J. (1996). Corporate Bonds: Structures and Analysis. Hoboken, NJ: John Wiley & Sons.