Objective 16-1 Investment Fundamentals

-

Describe how risk-return relationships, risk tolerance, and asset diversification and allocation relate to the fundamentals of investments.

The Risks and Rewards of Saving and Investing

Why is it important to put money into a savings account? As a young adult, you have time on your side. If you continue to save regularly, your savings will accumulate. How much you end up with depends on three factors: how long you save, how often you add to your savings, and the interest rate your savings earn. The sooner you begin to save and the more frequently you put money into savings makes a big difference in terms of the amount you will accumulate during your lifetime. This is because of the concept of compound interest: The interest you earn on your initial savings periodically gets adding to the total amount you have saved and begins earning interest as well. Over time, the process continues, and you accumulate more and more money, as a result of compound interest.

To illustrate the power of compound interest and having your savings work for you, consider the following situation. Suppose that your grandparents had started a savings account for you the day you were born. Every month, they deposited $100 until you turn 16. By your sixteenth birthday, your grandparents have put aside $19,200. Because they put the money in a savings account that earned a 2.5 percent average interest rate the account balance after 16 years would be $23,578. In other words, you have earned $4,378 by doing nothing more than letting your money sit in a savings account. (Note that interest rates on savings accounts since 2008 have been closer to 0 to 0.25 percent.)

Now suppose you have the choice of using the money to buy a car or continuing to keep it in the savings account. Either way, your grandparents will stop contributing to your savings account. As tempting as it is to buy a new car, your father explains that if you save your money instead, and your money continues to earn 2.5 percent interest each year, when you are 65 it will have grown to $115,192. So, again, by doing nothing but earning interest, you have grown your money to a substantial amount. But is this all you can do? There are other alternatives to savings that may make your money grow to even greater amounts.

Why isn’t saving enough? Although saving is important, it isn’t the only way to make money. The Federal Deposit Insurance Corporation (FDIC) insures most savings accounts up to $250,000, so you may be convinced this is a good low-risk strategy because you are guaranteed to receive your money at any time, plus the interest it has earned. However, depending on the amount and timing of your long-term needs, the amount your money will earn in a savings account might not be enough to reach your goals. The interest rates for savings accounts and other short-term, low-risk investments have been at historically low levels over the past decade. In addition, your savings are further compromised by taxes and inflation (see the BizChat box). To reach your long-term financial goals, you’ll most likely need to have your money work harder by investing in securities, such as stocks, bonds, or mutual funds.

Continuing the scenario from earlier, now consider that instead of keeping your grandparents’ gift in a savings account, you decide to invest the funds in a group of conservative stocks that would earn 8 percent per year on average. In this case, when you reach 65, you would have more than $1 million—$1,172,973!

Investment Risk

Isn’t investing too risky? As our example illustrates, when you invest money rather than saving it in a bank, your money will have the potential to grow even more. Investing is buying or otherwise obtaining an asset with the expectation of achieving a future profit. Investing and saving are fundamentally different because of the different risks related to each of these types of activities. Savings is associated with little, if any, risk. In contrast, investing has some inherent risk because there is a chance you could lose part or all of your investment.

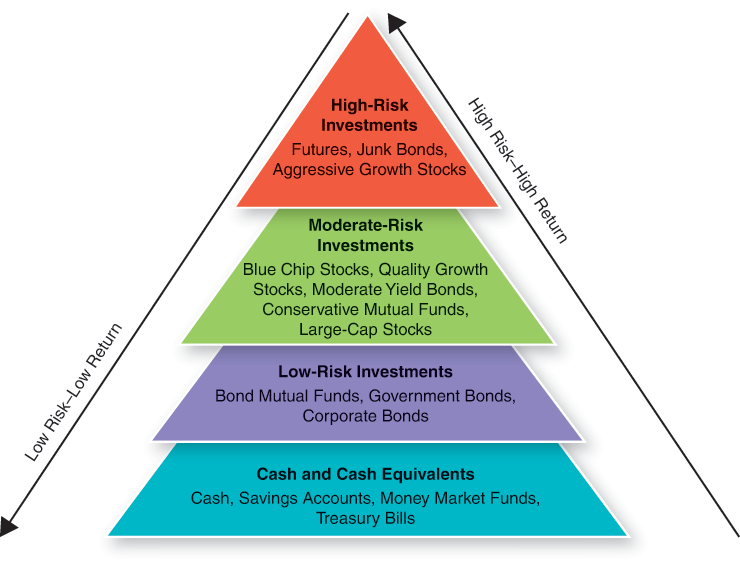

There is a direct relationship between risk and return for all securities, with the least risky investments offering the lowest amount of return and vice versa. This relationship is known as a risk–return relationship. Figure 16.1 shows the risk–return relationships of various types of savings and investment options. As you can see, the least risky investments offer the least amount of return. If reducing your risk is a necessity, then to acquire the same amount of money you would with a riskier investment, you will need to increase the amount you save or the length of time it is saved or invested. Or you could lower your expectations about the amount of money you will ultimately accumulate.

Figure 16.1

Risk-Return Relationships

© Mary Anne Poatsy

In addition to the specific risk associated with each investment, there is also a more general risk associated with the overall market, known as market risk. Events such as wars and other political turmoil, changes in interest rates, terrorist attacks, recessions, and natural disasters will cause a decline in the market as a whole. For example, after the September 11 terrorist attack in New York City, the financial markets reopened one week later. The Dow Jones Industrial Average lost 7.1 percent of its value by dropping 684 points that day. By the end of the week, the Dow had fallen 1,370 points (14 percent). Its largest one-week drop in history. The Dow dropped significantly again, losing 777 points (7.0 percent) on September 29, 2008, at the beginning of the financial crisis of 2007–2008.

How do I know my risk tolerance? To determine whether investing is worth the risk, you must know how much risk you can tolerate. The less tolerant you are of risk, the fewer investment chances you can and should take. Most of us have a good idea of how tolerant we are toward risk. Your current behavior with money and other situations are indications of whether you should invest conservatively, moderately, aggressively, or somewhere in between. There are also several tests that you can take online to help quantify your tolerance level. Another way to figure out your risk tolerance is by asking yourself this question: “Are my investments going to keep me awake at night with worry?” If the answer is yes, then you need to reduce the risk level of your investments and perhaps lower your expectations accordingly. Over time, your tolerance to risk can change depending on your knowledge level and financial situation. As you become more secure financially, you might be willing to risk losing some money for the possibility of earning more. As you begin to learn more about investing, you may be more comfortable with evaluating some of the risks you will take, thus increasing your risk tolerance.

How do I start investing? Depending on how much money you have to invest, you might start investing by purchasing stock in one or two companies or by investing in a mutual fund. We’ll discuss these investment alternatives as well as some others in more detail later in the chapter. As you invest, you should keep in mind two strategies that will help to minimize your risk: diversification and asset allocation. Both strategies center on the notion of not putting all your eggs in one basket to avoid the possibility of losing everything because of one bad investment.

How do I make money by investing? There are two ways to earn money by investing. Most investors hope to make money through capital appreciation, that is, “buying low and selling high,” or buying a security at one price and then later selling the security at a higher price. When this happens, the investor incurs a capital gain. If there is a decrease in value between the purchase price and the selling price, the investor incurs a capital loss. Investors can also receive periodic payments of dividends or interest, if they invest in securities that distribute dividends or interest.

What is diversification? Diversification is having a variety of investments in your portfolio, such as different types of companies in different industries. For example, assume you have $6,000 to invest. You have the option of putting all your money into one company that is strong and has great potential for long-term growth and profits. You also have the option to put $1,500 into four different companies, each in a different industry. Each of these companies is also thought to be a great investment.

The first option may be great if the one company has unlimited success, but economic factors, consumer demand, competition, and other issues can hamper a company’s ability to make money constantly. If you instead diversify and invest in several companies that are in different industries, you can better insulate yourself from the negative effects that could affect a company or industry. If a negative event happens, the chances are that one or more of the other companies in your investment portfolio will be performing well and will offset the losses of the company that is not. Even if you experience a loss, it is not likely to be as large as it would be if you were invested in only one company.

Keep in mind, however, that diversification does not protect against market risks that affect the overall market, as discussed previously. And, if your portfolio is diversified but still heavily invested in a particular industry or market segment, your portfolio could still be significantly affected by events that affect that industry. Such was the case for many investors who were caught in the dot-com crash. In the late 1990s, greater universal access to the Internet created an opportunity for a new untapped market and unlimited business opportunities. Many investors threw caution to the wind and heavily invested in novel Internet-based businesses referred to as dot-com businesses. Investors were buying stocks of companies without regard to the specific business strategy and financial forecasts. In 1999, for example, more than 450 new businesses, mostly Internet- and technology-related, entered the stock market. Of those, almost a quarter doubled in price on the first day of trading.1 But soon afterward, many of those same companies filed for bankruptcy. Pets.com, famous for its sock-puppet commercials, traded on the market for the first time in February 2000 and then filed for bankruptcy nearly nine months later. The burst of the dot-com bubble contributed to a mild economic downturn in the early 2000s.

What is asset allocation? Asset allocation refers to how you structure your portfolio with different types of assets (stocks, bonds, mutual funds, real estate, and so on) to reduce the risks associated with these different types of investments. Studies have shown that most of an investment portfolio’s performance is determined by the allocation of its assets, not by the selection of individual investments or how well a person has timed his or her buying and selling of the investments.2,3

Properly allocating your assets is particularly important if you want to minimize your investment risk in the highly volatile markets that have been common since the new millennium. The allocation of assets in a portfolio depends on your risk tolerance and can change as an investor reaches certain milestones, such as getting married, paying for college tuition, or retiring. Figure 16.2 shows how a person’s risk tolerance affects the asset allocation mix in a portfolio.

Figure 16.2

Asset Allocation Risk Based on Risk Tolerance

© Mary Anne Poatsy

Are there rules and regulations that govern investing? The Securities and Exchange Commission (SEC) is a U.S. federal agency created to protect investors and maintain fair and orderly securities markets. It governs the securities exchanges; the people who issue, trade, and deal securities; and those who offer investment advice. The SEC also establishes regulations that govern how companies disclose information to the investing public, and regulations for the investment banks creating the investment products the public buys. In doing so, the SEC controls what should be put in the documentation (the prospectus) of an initial bond or stock issue.

In addition, the SEC prohibits fraudulent activity with regard to the offer, sale, and purchase of securities, such as insider trading. Insider trading is the buying and selling of securities based on information that has not been disclosed to the public. For example, suppose you own 1,000 shares of XYZ Corp. stock and you are on friendly terms with the company’s chief financial officer (CFO). The CFO tells you the company is going to claim bankruptcy next week, so you sell all your shares before the information is publicly released. If you do this, you have taken part in illegal insider trading.

The government has made a pointed effort to stop insider trading on Wall Street. One of the most high-profile insider trading cases involved the domestic celebrity Martha Stewart. In 2001, Martha Stewart sold almost 4,000 shares of ImClone stock after receiving pertinent information about the company from her friend, ImClone’s CEO. Stewart was convicted of insider trading and spent five months in prison and an additional five months under house arrest. More than a decade later, Rajat Gupta, a former board member for Goldman Sachs Group Inc. and head of McKinsey & Co., was convicted of insider trading when he leaked important investment information discussed at a Goldman Sachs board meeting to Raj Rajaratnam, a hedge fund founder and friend of Gupta. The conviction was upheld in March 2014.

Although there are inherent risks when investing your money in stocks, bonds, or mutual funds, if the investments are within your risk tolerance level and your portfolio is well diversified with good asset allocation, you can mitigate the risks and allow your money to work harder for you.