Objective 2-5 Government and the Economy

-

Describe the four stages of the business cycle, and explain how the government uses both fiscal policy and monetary policy to control swings in the business cycle.

Economic Policies

Why does the state of the economy change? In 1980, the rate of inflation was at its highest level—nearly 15 percent.9 Only eight years before and six years after that high inflationary period (1972 and 1986), inflation was hovering around 2 percent.10 Over time, the economy naturally goes through periodic increases and decreases in inflation. Economists refer to these increases and decreases as the business cycle.

There are four stages of the business cycle, as illustrated in Figure 2.9:

Figure 2.9

The Business Cycle

Peak. The peak occurs when an economic expansion is at its most robust point.

Recession. By definition, a recession is a decline in the GDP for two or more successive quarters of a year. In recessionary times, corporate profits decline, unemployment increases, and the stock market reacts with large selling sessions that result in decreasing stock prices. The U.S. economy has experienced seven recessions over the past 40 years; the most recent recession began in late 2007 and ended in the fall of 2009. This was the country’s worst and longest recession since the Great Depression. A very severe or long recession is a depression. Depressions are usually associated with falling prices (deflation). After the onset of the Great Depression in 1929, the government used policies to control the economy to avoid another such depression.

Trough. A trough occurs when the recession hits bottom and the economy begins to expand again.

Expansion or recovery. After a recession or a depression, the economy hits a trough and begins to grow again and therefore enters into an expansionary or recovery phase. Eventually, the recovery will hit a peak, and the cycle begins again.

How does the government control swings in the business cycle? Ideally, the economy should stay near its peak all the time. But left to its own forces and in reaction to external actions on the economic system, such as wars and variations in the weather, it is inevitable that the economy cycles through recessions and recoveries. To smooth out the swings in the business cycle, lawmakers use fiscal policy to determine the appropriate level of taxes and government spending.

Fiscal Policy

Why does the government increase taxes to influence the economy? Threats of increasing taxes are a concern to Nick and Jacinta. They feel they pay too much already and need as much of their paychecks as possible to make their anticipated mortgage payments. However, they are told that an increase in taxes is necessary to offset rising inflation. Higher taxes translate into consumers spending less money, which in turn slows the growth of businesses and consequently slows down the economy by reducing the amount of money in the system. This, in turn, lowers inflation.

Decreasing taxes does not have quite the opposite effect on the economy as increasing taxes. It would seem that if increasing taxes would slow down an economy, a tax cut would help stimulate the economy. Although that is partially true, the amount of money entering into the system depends on how much of the reduction in taxes consumers spend and how much of it they save. Money put into savings does not help stimulate the economy immediately. To stimulate the economy more quickly, the government uses another form of fiscal policy: government spending.

How does government spending help stimulate the economy? The government spends money on a wide variety of projects, such as infrastructure improvements and projects that benefit the military, education, and health care. Because the money gets spent immediately and not saved, government spending increases the cash flow in the economy faster than decreasing taxes does. Often, government spending creates additional jobs, which also helps stimulate the economy. The American Recovery and Reinvestment Act was a huge stimulus plan introduced in 2009 to help jump-start the failing economy. It included government spending for infrastructure, education, and health care improvements. During periods of high economic growth, the government may decrease its spending. But reducing government spending is more easily said than done. There always seem to be government programs that are essential and cannot be cut regardless of the state of the economy. This is always a debate around election time, and there really isn’t one right answer to this issue. Overall, fiscal policy has its critics. Some economists think government spending has a mixed record when it comes to jump-starting the economy. That was the case with the last stimulus. Other economists believe the impact of the spending would have been greater if the stimulus had been larger. This issue is still being debated.

Monetary Policy

What else can be done to control the economy? The second tool used to manage the economy is monetary policy. Monetary policy is not exercised by the government. Instead, it is exercised by the Federal Reserve System (the Fed). The Fed is the central banking system of the United States. Created by Congress as an independent governmental entity, it includes 12 regional Federal Reserve Banks (see Figure 2.10) and a Board of Governors based in Washington, D.C. The Federal Reserve Banks carry out most of the activities of the Fed. The Fed also includes the Federal Open Market Committee, which sets the policies of the Fed, including its monetary policies. Through its monetary policy, the Federal Reserve affects the nation’s money supply and helps shape the direction of the economy.

Figure 2.10

The 12 Federal Reserve Districts

Source: The Twelve Federal Reserve Districts, retrieved from: www.federalreserve.gov/

What is the money supply? It is natural to think that just all the coins and bills held by people, businesses, and banks make up the country’s money supply. However, that would represent only a portion of the country’s money. The money supply is the combined amount of money available within an economy, and it includes not only currency (coins and bills) but also personal savings and checking accounts as well as the deposit accounts from large institutions. In particular, the money supply consists of the following different “layers” of funds (see Figure 2.11):

Figure 2.11

Money Supply Measures for M-1 and M-2

Surprisingly, currency is not the biggest component of the U.S. money supply. Savings and other deposits represent the largest component of the money supply.

© Mary Anne Poatsy

M-1. Coins and bills (currency), traveler’s checks, and checking accounts constitute the narrowest measure of our money supply, which is referred to as M-1. M-1 assets are the most liquid in that they are already in the form of cash or are the easiest to convert to cash.

M-2. Another part of the money supply is that which is available for banks to lend out, such as savings deposits, money market accounts, and certificates of deposit (CDs) less than $100,000. This layer of the money supply, in addition to the M-1 layer, constitutes M-2.

M-3. The third layer of the money supply is M-3. M-1 and M-2, plus less liquid funds, such as larger CDs (greater than $100,000), money market accounts held by large banks and corporations, and deposits of Eurodollars (U.S. dollars deposited in banks outside the United States), make up M-3. The Federal Reserve Board of Governors has stopped publishing M-3 data.

Why is the money supply important? Money has a direct effect on the economy: The more money we have, the more we tend to spend. When we as consumers spend more, businesses do better. The demand increases for resources, labor, and capital because of the stimulated business activity, and, in general, the economy improves. However, too much money in the economy can be too much of a good thing. When the money supply continues to expand, eventually there may not be enough goods and services to satisfy demand, and, as was previously discussed, when demand is high, prices will rise, resulting in inflation. (Remember the demand curve? It shifts to the right.) Economists carefully watch the CPI to monitor inflation, because they don’t want inflation to go too high.

An opposite effect can happen when the supply of money becomes limited following a decrease in economic activity. When the economy begins to slow down as a result of decreased spending, either disinflation (reduced inflation) or deflation (falling prices) results. To help manage the economy from being in the extreme economic states of inflation or deflation, the Fed uses three tools to affect money supply (see Table 2.6):

Table 2.6

Federal Reserve Bank Monetary Policy

Source: Based on Federal Reserve Bank of New York, “Historical Changes of the Target Federal Funds and Discount Rates 1971–Present,” www.ny.frb.org. © Michael R. Solomon.

Reserve requirements

Short-term interest rates

Open market operations

Reserve Requirements

What are reserve requirements? The reserve requirement, determined by the Federal Reserve Bank, is the minimum amount of money banks must hold in reserve to give to their depositors who want to withdraw it. When you deposit money in a bank, the money does not sit in a vault waiting for you to withdraw it later. Instead, banks use deposits to make loans to others: people, small businesses, corporations, and other banks. Banks make money by the interest charged on those loans; however, a bank must be able to give you back your money when you demand it. If a bank doesn’t have enough money to cover what its customers want to withdraw on a given day, they might get nervous and try to withdraw all of their funds. This is referred to as a bank run. Bank runs that occurred in 1929 helped spark the Great Depression. At that time, people were so nervous about banks not being able to cover their deposits that the massive withdrawals forced many banks to close.

Banks do not lend out the entire balance of their deposits. The Fed mandates banks retain a certain reserve requirement sufficient to cover the demands of their customers for on any given day. This includes trips to automatic teller machines, the use of debit cards, requests for loans, and the payment of checks that you write. The Fed can ease or tighten the money supply by increasing or decreasing the reserve requirement. For example, if the Fed increases the reserve requirement, it forces banks to hold on to more money rather than lending it out. This slows down economic activity. However, the Fed rarely uses the reserve requirement as a means of monetary policy because these actions would be very disruptive to the banking industry.

Short-Term Interest Rates

What is the discount rate? The Federal Reserve Bank serves as the bank to other banks. Occasionally, commercial banks have unexpected draws on their funds that might put them near their reserve requirements. In those instances, banks may turn to the Federal Reserve Bank for short-term loans. For this reason, the Fed is sometimes referred to as the “lender of last resort.”

When banks borrow emergency funds from the Fed, they are charged an interest rate, called the discount rate. The Federal Reserve has the power to increase or decrease the discount rate in its efforts to control monetary supply. When the Fed lowers the discount rate, commercial banks are encouraged to obtain additional reserves by borrowing funds from the Fed. Commercial banks then lend out the reserves to businesses, thereby stimulating the economy by injecting funds into the economic system. However, if the economy is too robust, the Fed can increase the discount rate, which discourages banks from borrowing additional reserves. Businesses are then discouraged from borrowing because of the higher interest rates that the banks charge on their loans.

Is the discount rate the same as the federal funds rate? The federal funds rate is not the same as the discount rate. It is often reported in the news that the Fed intends to change the federal funds rate in its efforts to stabilize the economy. The federal funds rate is the interest rate banks charge other banks when they borrow funds overnight from one another. (As mentioned previously, the Fed requires banks to have so much money on reserve, depending on the deposits in the bank and the other assets and liabilities held by each bank. Banks avoid dipping below their required reserves by borrowing from each other before they have to borrow from the Fed at the discount rate.) Despite news reports, the Fed does not control the federal funds rate directly. Instead, the federal funds rate is the equilibrium price created through the Fed’s open market operations and the exchange of securities.

The excess reserves that are available to lend between banks come from securities that the Fed buys and sells through its open market operations. If there are excess reserves on hand, banks have adequate funds to lend to other banks. On the other hand, if excess reserves are not as plentiful, banks lend funds to one another more sparingly. To increase the federal funds rate, the Fed sells bonds in the open market. Banks buy the securities, thus reducing their excess reserves available for loans. The decrease in excess reserves increases the federal funds rate.

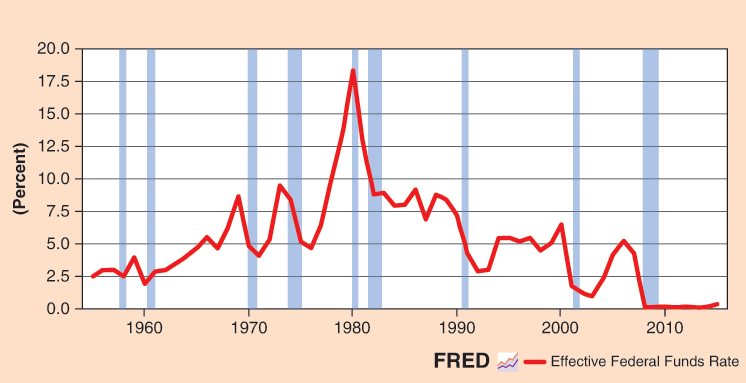

The opposite holds true as well. To decrease the federal funds rate, the Fed will buy bonds in the open market. Buying securities from banks increases the banks’ excess reserves, making money more available, which decreases the federal funds rate and helps stimulate the economy. Figure 2.12 shows the trend of federal funds rates over the past several decades. As you can see, the federal funds rate has been at a historically low of .25 percent for many years.

Figure 2.12

Trend of Effective Federal Funds Rate 1954–2016

Source: “Historical Changes of the Target Federal Funds and Discount Rates 1971– Present,” Federal Reserve Bank of New York, http:/

Open Market Operations

What are open market operations? The primary tool the Fed uses in its monetary policy is open market operations, buying and selling U.S. Treasury and federal agency bonds on the “open market.” The Fed does not place transactions with any particular security dealer; rather, securities dealers compete for federal transactions in an open market. When the Fed buys or sells U.S. securities, it is changing the level of monetary reserves in the banking system by adding or taking away money from the system. When the Fed sells securities, reserves are reduced to pay for the securities (money is said to be “tight”), and interest rates rise. However, when the Fed buys securities, it adds reserves to the system (money is said to be “easy”), and interest rates drop. Lower interest rates help stimulate the economy by decreasing people’s desire to save and increasing their demand for loans, such as home mortgages. Using open market operations is probably the most influential tool the Fed has to alter money supply.

To make their decision about whether to buy a home, Nick and Jacinta would benefit by paying attention to the Fed’s monetary policies. If the Fed buys securities, it’s likely that interest rates for mortgage loans will fall. Additionally, Nick and Jacinta can look to the discount rate and the federal funds rate. News about the lowering of the discount rate will signal that banks might have funds available to lend out at potentially lower rates. Although the federal funds rate does not have a direct impact on mortgage rates, it does have an indirect effect because interest rates respond to economic growth and inflation. Reports on the news that the Fed is striving to change the federal funds rate will indicate to Nick and Jacinta whether it’s likely that interest rates will increase or decrease in the near future. This in turn can help them determine the best time to buy a home.