Objective 6-3 Corporations

-

Explain how a corporation is formed, and compare a corporation to other forms of business.

Advantages of Incorporation

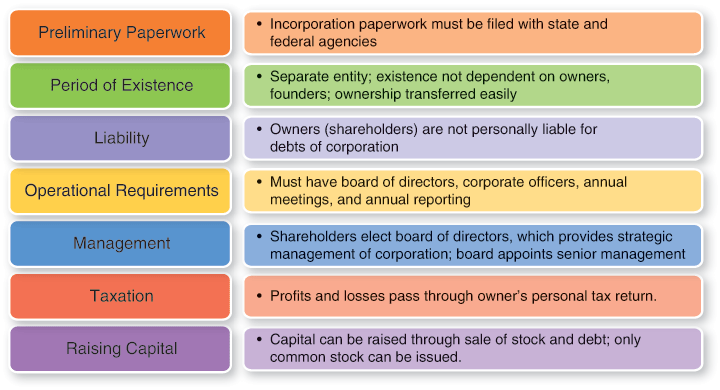

What is a corporation? A corporation is a specific form of business organization that is legally formed under state laws. A corporation is considered a separate entity apart from its owners; therefore, a corporation has legal rights like an individual. Consequently, a corporation can own property, assume liability, pay taxes, enter into contracts, and sue and be sued—just like any other individual. Most of the time, a corporation is structured as a C corporation, which refers to Subchapter C of the Internal Revenue Code by which it is governed. Sometimes a corporation can be structured as an S corporation (which we discuss next). Some characteristics of a C corporation are listed in Figure 6.5.

Figure 6.5

Characteristics of a C Corporation

When does it make sense to form a corporation? Some business owners incorporate just to be able to end a business’s name with “Company,” “Co.,” “Incorporated,” or “Inc.” Having such corporate nomenclature can give a start-up business an air of legitimacy, which can be a perceived benefit to prospective clients and lenders and potentially a greater threat to the competition. More important, forming under a corporate structure provides many advantages not available with other business structures such as protecting against personal liability, perpetual existence, and raising capital.

How can a business owner protect his or her personal assets? Corporations are not just for big businesses. A C corporation can be the right choice for many small entities because it is a separate legal entity and is responsible for its own debts, obligations, and liabilities. It also can sue and be sued. This is one of the main reasons owners incorporate their business. When a corporation runs into problems, only the corporation’s assets can be used to remedy the situation; the owners are not personally liable for the business’s debts.

What happens to a corporation when an owner leaves? Sole proprietorships and partnerships, by their nature, are dependent on their founding owners. When an owner dies or otherwise leaves the business, a partnership or sole proprietorship is usually terminated. On the other hand, corporations can theoretically live forever because their ownership can be transferred to different shareholders. Shares of ownership are easily exchanged, so the corporation will continue to exist should an owner die or wish to sell his or her interest in the business. As long as it is financially viable, a corporation is capable of continuing forever.

Is it easier for corporations to get funding and to raise capital? Corporations can raise money by selling shares of ownership to a specified group of individuals. Or, when a corporation has reached a significant size, it can extend its ownership by “going public”—selling shares of ownership in the corporation to the general public. A stock certificate is the tangible evidence of investment and ownership. And, as we noted previously, lenders are more likely to loan money to an incorporated business because they are not limited to the credit profile of a sole proprietor or general partners.

Are corporations taxed the same as other types of businesses? Because sole proprietors and partners run their business income through their personal income tax statements, these two types of business structures pay taxes at the owner’s or partners’ tax rates. Corporations have separate tax rates. The corporate tax rate is 15 percent for the first $50,000 of net income a business earns, whereas the same amount of profits from a sole proprietorship or partnership would be taxed at a rate of 25 percent. However, most corporations will generate more than $50,000 in net income. Businesses generating more than $50,000 in taxable income will pay taxes at an equal or higher tax rate than individuals.

Does it matter where a business is incorporated? The answer to this questions is more complex than it seems, but there are some general considerations that should be evaluated. If you have a corporation with fewer than five shareholders or members, it is usually much easier and often less expensive to incorporate in the state where your business has a physical presence. For some larger businesses, however, it may be more advantageous to incorporate in a state that is historically more favorable to businesses, such as Delaware, Nevada, and Wyoming. Delaware offers some of the most flexible and business-friendly statutes in the country. Nevada offers low filing fees and has no state corporate income, franchise, and personal income taxes. For similar reasons, Wyoming is also becoming a popular state in which to incorporate.

Structure of a Corporation

How is a corporation structured? In its simplest configuration, a corporation’s organizational structure is comprised of shareholders, a board of directors, corporate officers, first-line managers, and employees, as Figure 6.6 shows. Each group has different responsibilities.

Figure 6.6

Organizational Structure of a C Corporation

Shareholders have the power to elect the board of directors of a C corporation. The board, in turn, has the ability to hire (or fire) the company’s corporate officers.

Shareholders

Whether or not a corporation is privately owned or publicly owned, it has shareholders. Shareholders (or stockholders) have an ownership interest in the company. For their investment, the corporation provides them with stock certificates identifying the number of shares (called apportioned ownership interest) they own. A publicly owned corporation is a corporation regulated by the U.S. Securities and Exchange Commission (SEC) because the shares of ownership can be traded on public stock exchanges. Although shareholders of a publicly owned corporation serve as the owners of the corporation, they have no involvement in the direct management of the corporation. Instead, they can influence corporate decisions by electing directors, overseeing the laws and rules that govern the organization, and voting on major corporate issues.

In privately held (or closed) corporations, in most cases, the company’s founders, a management team, or a group of private investors own the company. These owners are generally involved in the management and daily operations of the business and have more decision-making responsibilities than do shareholders of publicly owned corporations. The owners of privately held corporations are generally the sole shareholders. Any shares of privately held corporations are not traded on public stock exchanges.

Directors

The shareholders of a corporation elect its board of directors, and the members of the board select and hire the business’s management team of corporate officers. Major financing and business decisions for the corporation are also made by the board of directors. For example, in addition to setting the corporation’s policies, the board authorizes the issuance of stock, approves loans to or from the corporation, and decides on major real estate transactions. Consequently, because they vote for the board members, the firm’s shareholders can influence the nature of a corporation and how it is run.

Not only is a business’s board of directors responsible for hiring the corporation’s major executives, it is also responsible for ensuring they do their jobs. Not all boards are effective in doing so. Following a rash of corporate scandals, in 2002, the Sarbanes-Oxley Act was enacted. The act provides a new set of regulations designed to make boards of directors more accountable. If the members of a board of directors ignore their responsibility to manage the internal controls of a company, they risk going to prison and face huge fines.

Officers and Line Managers

The primary lineup of officers elected by a corporation’s board of directors include the firm’s CEO, CFO, and COO. The chief executive officer (CEO) is typically responsible for the entire operations of the corporation and reports directly to the board of directors. Sometimes the CEO is a member of the board of directors as well. The chief financial officer (CFO) reports directly to the CEO and is responsible for analyzing and reviewing the business’s financial data, reporting its financial performance, preparing budgets, and monitoring the firm’s expenditures and costs. The chief operating officer (COO) is responsible for the day-to-day operations of the organization and reports directly to the CEO. Often, there is a chief legal officer or general council, and depending on the needs of the company, there might also be a chief information officer (CIO). In actuality, any “officer” position can be formed if it makes sense for the company. In smaller companies, only one or two people might play the roles of several different officers. For example, the CEO might also serve as the CFO. In large companies, the responsibilities of each officer are demanding enough that first-line managers, people who directly supervise lower-level employees, help run the business.

Disadvantages of Incorporation

Are there any disadvantages of structuring a business as a corporation? Forming a corporation is a much more cumbersome process than forming a sole proprietorship or a partnership. Figure 6.7 shows the steps involved in forming a corporation.

Figure 6.7

Steps in Forming a Corporation

Corporations provide owners with more protection than other business structures, although forming a corporation is a more complex process.

Because a corporation is a separate legal entity, there are many more filing and process requirements that must be fulfilled to maintain corporate status. All public companies must file an annual report, and all corporations, both private and public, must maintain written minutes of annual and other periodic board of director and shareholder meetings. Major decisions must be recorded, including decisions about whether to issue stock, purchase real estate, approve leases, loans, or lines of credit and make changes to the stock options and retirement plans employees receive. A corporation must also record financial transactions in a double-entry bookkeeping system and file taxes on a regular basis (quarterly or annually).

Because it is considered its own legal entity, a corporation files its own tax return. This results in the disadvantage of double taxation. Double taxation occurs when taxes are paid on the same income twice. The classic business example of double taxation is the distribution of dividends. A corporation is first taxed on its net income, or profit, and then distributes that net income to its shareholders in the form of dividends. The individual shareholder must then pay taxes on the dividends (which have already been taxed at the corporate level). Therefore, the same pool of money—corporate profits—has been taxed twice: once in the form of corporate profits and again as dividends received by the shareholders. Although this is a commonly mentioned disadvantage of corporations, it affects only those corporations that pay dividends to their shareholders.

Can a business have the protection of a corporation but not pay corporate taxes? When choosing a legal structure for their businesses, most entrepreneurs want to achieve two goals: protect themselves from personal liability and have the tax advantages of their business income flow through to their individual tax returns. A corporate structure protects an owner’s personal assets from being touched if the corporation is in financial difficulty, but the corporation is taxed as a separate entity without flow-through to the owner’s returns. Fortunately, there are other forms of business structures in which both goals can be met: the S corporation and the limited liability company.

S Corporations

What is an S corporation? An S corporation is a regular corporation (a C corporation) that has elected to be taxed under a special section of the Internal Revenue Code called Subchapter S. Like C corporations, S corporations have shareholders, and they must comply with all the other regulations involving traditional C corporations.

How is an S corporation different from a C corporation? Unlike C corporations, S corporations do not pay corporate income taxes. Instead, as with a partnership or a sole proprietorship, shareholders in an S corporation owe income taxes based on their proportionate share of the business profits they receive and pay taxes through their own individual tax returns. Passing taxes through personal tax returns is one of the primary advantages of forming a business as an S corporation. However, even though S corporations do not pay corporate taxes like C corporations, they still must file a corporate tax return every year. In addition, S corporations must comply with the meeting and reporting requirements established for C corporations. Other characteristics of an S corporation are shown in Figure 6.8.

Figure 6.8

Characteristics of an S Corporation

How does an S corporation handle personal liability? The beauty of an S corporation is that it offers the best of both worlds: Profits and losses pass through to the shareholders, and the corporate structure provides some limitations on the personal liability of the owners. Although an owner’s personal assets will be protected in case of a large claim against the corporation, the S corporation does not assume liability for an owner’s personal wrongdoings. This is true for any corporate structure—whether it is a C corporation, an S corporation, or a limited liability company (discussed later). So, if an owner directly injures someone or intentionally does something fraudulent, illegal, or reckless that causes harm to the company or someone else, he or she will be held personally responsible and is not protected under the corporate umbrella.

For example, suppose William is the owner of a boating business that offers day cruises in the San Francisco Bay. Unfortunately, one foggy day, William’s boat collides with another boat, causing his boat to capsize. Before leaving the dock, William knew there were not enough life jackets for each passenger. If any of his passengers were harmed because there were not enough life preservers, William most likely would be held personally liable for his negligent actions, even though he had structured his company as an S corporation. William not only would be in danger of losing the business but also may be forced into personal bankruptcy if his personal assets were needed to help satisfy the claims on the company.

Can any business elect to be an S corporation? There are certain qualification requirements a business must meet to elect an S corporation status. According to the Internal Revenue Code, an S corporation must have the following characteristics:

The company must not have more than 100 shareholders.

Shareholders must be U.S. citizens or residents.

The company must issue only one class of stock.

S corporations are an appropriate business structure for small business owners who want the legal protection of a corporation but also want to flow business income and losses on their personal tax returns. However, if a business does not meet the IRS requirements for an S corporation but the owner stills wants personal liability protection along with pass-through tax benefits, a limited liability company might be a suitable alternative corporate structure.

Limited Liability Companies

What is a limited liability company? A limited liability company (LLC) combines the corporate advantages of limited liability with the tax advantages inherent in sole proprietorships and partnerships. Similar to creating an S or a C corporation, an LLC requires articles of organization, so it is a separate legal entity (thus providing limited liability). But an LLC is free of many of the annual meetings and reporting requirements imposed on C and S corporations, so it is simpler to maintain.

LLCs do not issue stock. Rather, each member’s ownership is determined by the value of his or her capital account. A capital account tracks the member’s capital contributions to the LLC. Profit and loss distributions also flow through the capital accounts in proportion to the ownership percentage each member has. Because there are fewer corporate formalities, limited liability provisions, and the reporting of taxes at the individual level, an LLC is a popular business structure choice for many new businesses. Some states restrict the types of businesses that can form as LLCs. Other characteristics of an LLC are outlined in Figure 6.9.

Figure 6.9

Characteristics of an LLC

What’s the difference between an LLC and an S corporation? Although LLCs and S corporations share certain similarities, there are several differences between the two:

Ownership. S corporations are restricted as to the number of owners the company can have, but LLCs can have an unlimited number of owners (called members). In addition, LLC members are not limited to just U.S. residents and are not subject to other ownership restrictions imposed on S corporations.

Perpetual life. When a member leaves an LLC, the LLC must dissolve, unless all remaining members agree to continue the business. Some states require a dissolution date be listed in an LLC’s articles of organization. Consequently, an LLC has a limited life span.

Stock transfer. Stock in an S corporation, like a C corporation, is freely transferable, whereas the ownership interest in an LLC is not, and the transfer generally requires the approval of other members.

Profit and loss distributions. An LLC can allocate its profits in whatever way its owners agree on, but the profits of an S corporation are allocated in proportion to a shareholder’s interest. So, if two members own a business and one contributes 75 percent of the capital but does only 25 percent of the work whereas the other member contributes 25 percent of the capital but does 75 percent of the work, the two members can decide that a fair allocation of profits is 50/50. This arrangement would be possible with an LLC, but with an S corporation, the profits would need to be distributed based on the 75/25 ownership interest in the business.

Owner and employee benefits. An S corporation can offer fringe benefits to its owners, such as qualified retirement plans, employee-provided vehicles, and educational expenses related to the job. Because S corporations have stock, they can also offer their employees stock options and other stock bonus incentives. LLCs are limited in the benefits their members can be offered, and because LLCs do not issue stock, they cannot offer stock benefits to their employees.

What kinds of businesses are best suited as an LLC? There are many types of businesses in which an LLC structure is appropriate. LLCs may be a good choice for start-up businesses, not only for the tax benefits but also because it is easier to obtain financing because the number of investors (owners) is not restricted.

Comparing Forms of Ownership

Which form of ownership is best? There is no one entity that works for everyone. A certified public accountant or a tax attorney should be able to help you choose the right structure for your business. The important considerations are the operational, legal, and tax aspects of each structure as they apply to your unique situation. Figure 6.10 shows how the most common forms of ownership stack up to one another.

Figure 6.10

Comparing the Forms of Business Ownership